Watching the annual EPS estimate revisions for the SP 500, the expected, full-year, EPS growth for 2025, is now looking for 9% growth, versus the 14% growth rate as of October ’24.

Since it’s tough to find a comparable earnings period for tariffs, the goal with today’s earnings post was to find some period that that would be considered to be “anomalous” for earnings and see how the revisions progressed, which unfortunately, only leaves us with the COVID period.

Looking at the 3rd quarter ’20 earnings results, which was the quarter following the extreme impact of the Covid shutdown from March ’20 to June ’20, Q3 ’20’s estimated EPS growth for the SP 500, on July 1 ’20 was an expected decline in EPS of -25%, which improved to -21.7% by Sept 30 ’20, and then after the actual Q3 20 SP 500 were reported, the actual EPS decline for Q3 ’20 was -6.5%.

It’s certainly not an apples-to-apples compare, but if you look at 2020 SP 500 EPS estimates during that economically-wild period, the analysts way overshot to the downside in terms of the EPS revisions, (for good reason) and my educated guess here in the middle of Q2 ’25 facing tariff headlines every day, is that the Q2 ’25 SP 500 EPS estimate revisions will do the same again.

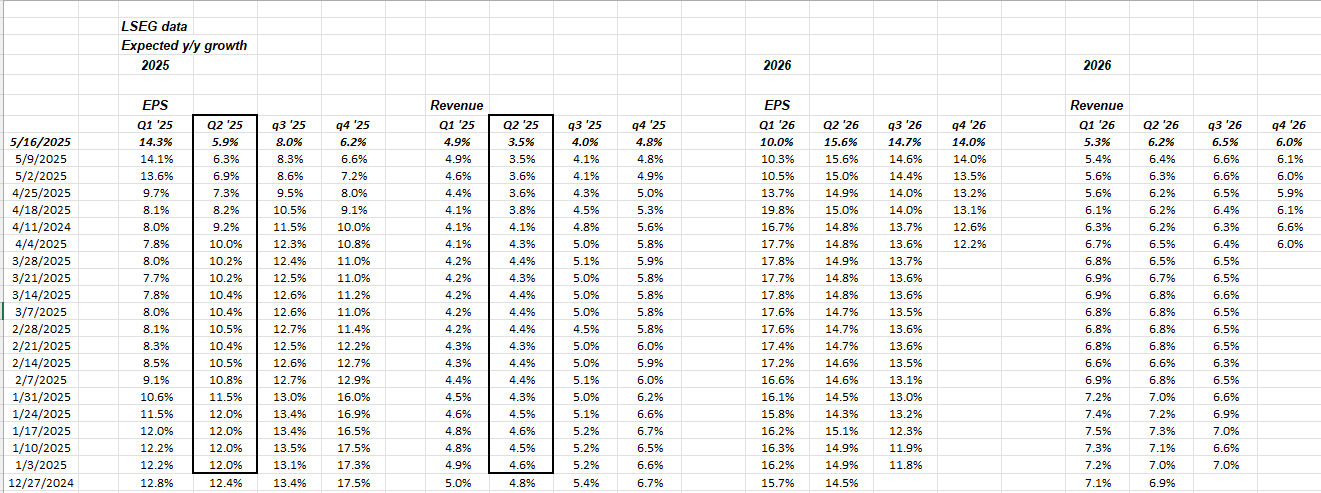

Q2 ’25 SP 500 EPS and revenue revisions

Clicking on the above spreadsheet, the dark-bordered columns are the EPS and revenue revisions (expected growth) for the SP 500.

Note for SP 500 EPS revisions for Q2 ’25, the year started out expecting 12% EPS growth in Q2 ’25, then started the April – June ’25 period at 10% expected growth, declining to 5.9% as of Friday’s close. From 10% to 5.9% over the last 6 weeks is a pretty steep revision, even though – at least the way I understood the headline, in early April the President tweeted that there was a 90-day pause on tariffs, which should carry investors through to July 8 ’25, thus eliminating tariff worries in Q2 ’25.

It’s nothing more than an educated guess, but when Q2 ’25 financial results start getting reported in July ’25, we could see a bigger “upside surprise” than we are seeing in Q1 ’25 results, which is +6.8% currently.

If investors have seen a decline in expected EPS growth from 10% to 5.9% after 6 weeks of the quarter, with another 6 weeks still remaining,

The expected Q2 ’25 EPS growth rate could get reduced to 2% – 3% by June 30 ’25.

SP 500 data:

- The forward 4-quarter estimate (FFQE) fell again this week to $269.93 versus last week’s $270.96, and the quarter’s starting FFQE of $278.96;

- The forward PE ratio this week was 22.07x, versus last week’s 20.9x and quarter’s start of 18x. No doubt the 5% jump in the SP 500 this week, helped the PE expansion;

- The SP 500 earnings yield fell back down to 4.53%, after peaking in early April ’25 at 5.50%;

- High yield credit spreads have tightened nicely, the last two weeks, tightening 84 bp’s from 5/2/25 and 127 bp’s from April 11th ’25;

Summary / conclusion: When looking back at the period during Covid (2020) and then the Fed rate hikes in 2022, what struck me, at least during Covid and the healthy stock market in 2021, was how far off the analysts were in predicting quarterly EPS growth rates. In Q2 ’21, which was the biggest y-o-y compare versus the horrid Q2 ’20, which bore the full brunt of the 2020 lockdown, and work-from-home, the sell-side consensus expected 65% SP 500 EPS growth on June 30 ’21 for Q2 ’21, only to have the actual growth be 96.1%.

Where the real issue with SP 500 quarterly earnings might lie this year is in Q3 ’25, when the real tariff impact starts to be felt (assuming the 90-day moratorium ends and the tariffs start to be felt, along with what seems to be gradually weakening economic data, (or at least economic data that wasn’t as robust as Q4 ’24).

Financial media is finally talking about how strong Q1 ’25 earnings turned out to be, (even with the SP 500 action in March ’25), which this blog noted for readers several weeks ago, here and here.

SP 500 earnings have always been a bit of a crapshoot, since sell-side analysts are people too, and seem to be influenced by headlines and media as much as anyone else. Also, the “risk / reward” of estimating EPS and revenue is that it’s always better to have the company generate upside surprises for EPS and revenue, rather than miss the consensus to the downside.

The biggest red flag for investors is to see prominent companies that weren’t expect to miss, suddenly start pre-announcing negative earnings surprises, from economically-related shortfalls.

None of this is advice or a recommendation, but only an opinion. Pat performance is no guarantee of future results. All earnings data is sourced from LSEG. None of this information may be updated, and if updated may not be done in a timely fashion.

Thanks for reading.

Well done, thank you.

thanks.