Cisco (CSCO) reports their fiscal Q3 ’25 after the closing bell on Wednesday, May 14th, 2025, with sell-side consensus expecting (per Briefing.com) $0.92 in earnings per share on $14.05 billion in revenue, for expected year-over-year (y-o-y) growth of 5% and 11% respectively.

LSEG data shows expectations of $0.92 in EPS, $14.08 billion in revenue growth and $4.7 billion in operating income, for y-o-y growth of 5%, 11% and 9% respectively.

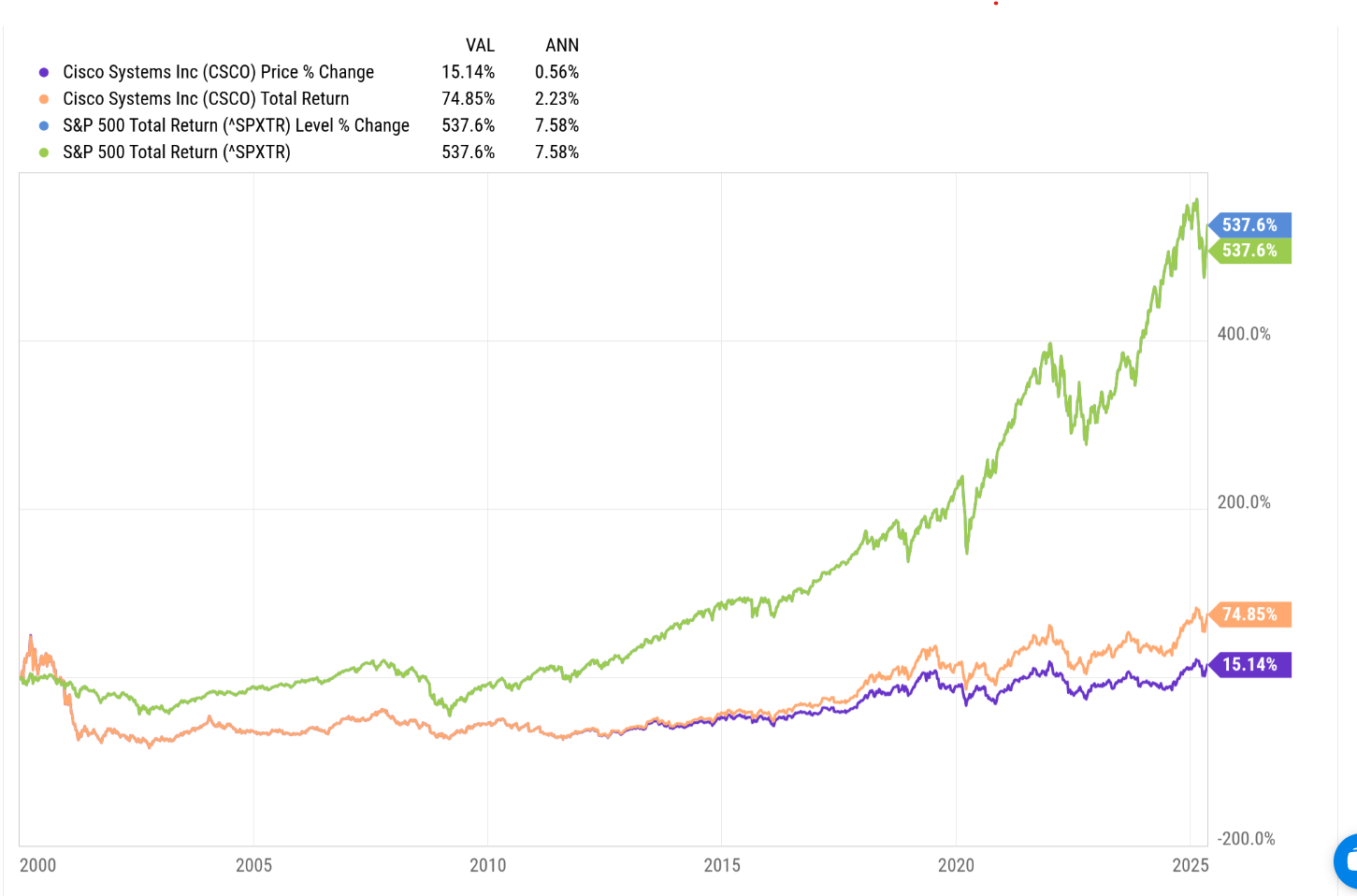

If you want one chart that detail’s Cisco’s progress over the years, here it is:

If you click on and expand the chart, Cisco’s total return has given up about 500 bp’s a year for the last 25 years relative to the SP 500 total return.

What’s changed ?

Well nothing yet: Cisco paid $28 billion for Splunk, closing the deal in March, 2024, and since Splunk is Cisco’s entry into the security market, and security or cyber-security remains one of the fastest growing segments within tech, maybe there’s a chance to finally generate some revenue and cash-flow growth for the networking giant.

For some portfolio’s Cisco could be a value way to play the cyber-security sector.

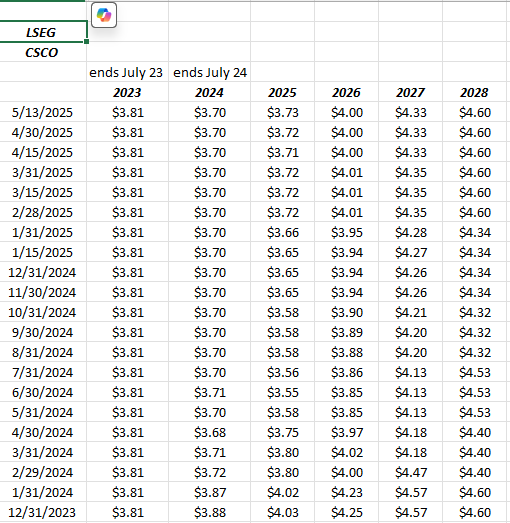

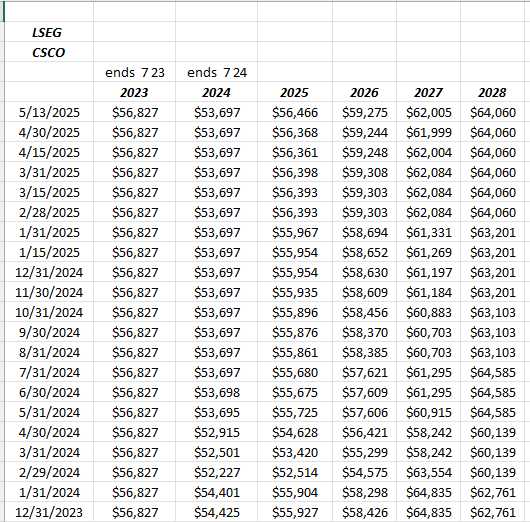

EPS and revenue estimate revisions:

Cisco has seen some positive EPS estimate revisions since the summer of ’24 (post Splunk) for the fiscal ’25 and ’26 years.

Cisco revenue estimate revisions for 2025 and 2026 have also been steadily positive since the summer of 2024.

Summary / conclusion: Cisco’s all-time-high was $82 in April of 2000, and the stock hasn’t gotten close since after doing numerous (maybe hundreds) smaller dilutive acquisitions, which destroyed shareholder value and really didn’t leave the company or shareholders any more “enriched”. In July, 2025, Chuck Peters will be at the helm of Cisco for a full 10 years, and while the stock has performed better over that period – up +10% from July 1 ’15 to May ’12, 2025 – it’s still trailing the SP 500, but only by 105 basis points, which is a mild positive for Chuck.

The big question seems to be whether Splunk can amount to anything meaningful at Cisco.

Networking is still 50% of Cisco’s annual revenue, and at best grows at a mid-single-digit revenue rate, with some periods far less than that. While “security” at Cisco stagnated at 6% – 7% of revenue for years, by adding Splunk, security revenue is now 15% of total Cisco revenue. The integration is expected to take at least 8 quarters or two full years since the Splunk deal closed in March ’24, so we will know more a year from now how Splunk is adding to Cisco’s organic growth.

Morningstar has noted Cisco is not an AI player, and with Splunk, security will likely be a far bigger segment than AI.

With security is Chuck Peters trying to convert Cisco from a hardware to software company ? Yes and no. IBM under Arvind Krishna is trying to do just that, and has met with some success, but Chuck Peters has been a Cisco-lifer, and to my knowledge hasn’t worked at anywhere in a leadership role, and so only knows Cisco as a hardware company.

Since 2010, and using the official revenue estimates for fiscal ’25 through ’28, Cisco has averaged just 3% revenue growth per year.

Since 2010, with the same constraints as revenue, Cisco EPS growth has averaged 7% per year.

Until the networking giant can break the bounds of these constraints, and generate some revenue growth, the only real benefit to owning the stock is to own an “uncorrelated” or “non-correlated” tech name that the market has completely forgotten. The stock has completely sat out this 15-year secular bull market, which – if you think about – presents an opportunity in and of itself.

Clients own a very small position – just waiting for some ray of light to commit more to the stock.

Trading at $62 today, or 17x forward earnings with 0% expected EPS growth for fiscal 2025 (ends July ’25), on 1% revenue growth, guidance will be a key component of Wednesday night’s earnings call.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results.

(Previous Cisco articles: here, here, and an article on Splunk here )