This will be a shorter earnings preview sine the stock is a very small position within client accounts, but Cisco is scheduled to report their fiscal Q3 ’24 financial results after the market closes on Wednesday, May 15th, 2024, after the closing bell.

Consensus is now expecting Cisco to report $0.82 in earnings per share on $12.5 billion in revenue and roughly $5 billion in operating income, for expected yoy declines of -18%, -14% in revenue and +2% growth in operating income.

Cisco has warned the last two quarters on inventory issues. Last quarter was particularly gruesome as Cisco guided this quarter revenue at the time to $12.1 – $12.2 billion versus the then estimate of $13 billion.

Here’s the progression (for readers) that shows the decline in inventory turnover at Cisco and the decline in revenue relative to inventory at Cisco over the last 3 – 4 years.

![]()

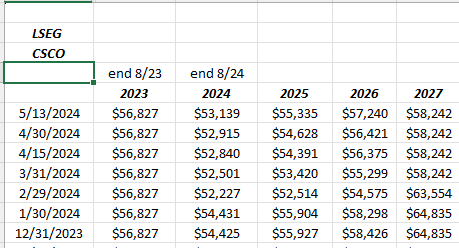

However, Cisco’s revenue estimate revisions have improved from mid-February ’24 (or about the point when they last reported earnings) as this table shows:

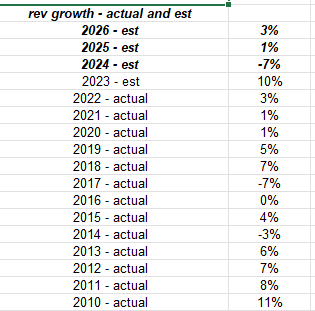

This blog has modeled the networking giant since the late 1990’s, and here is the recent history of revenue growth. 2023 was the first year of double-digit revenue growth since 2011. It looked like Cisco might be turning around, but 2024 has not been kind.

Cisco revenue growth peaked at 55% yoy in 1999 and has been pretty grim since.

Valuation: Cisco’s expected EPS growth over the next 3 years is expected to average 1% on expected -1% revenue growth (3-year average) assuming this year meets the -7% revenue decline expectation.

Trading at 13x expected EPS in ’24 of $3.67, the expected growth rate for the next 3 years isn’t appealing, although the 12x and 14x cash-flow and free-cash-flow looks a little better relatively speaking.

Can Splunk change Cisco’s prospects for growth ?

While a big acquisition always drives financial media interest, since it allows the networks to burn air time, technology acquisitions can be very hit-or-miss. IBM’s acquisition of RedHat was a mild bust, and the former RedHat CEO James Whitehurst left IBM after just a few years, while META’s acquisition of Instagram was a big success. Mergers and acquisitions seem to be particularly tricky within the technology business.

Splunk came public in 2012, while Cisco had come public 2 decades earlier. Same with Redhat and IBM. Younger companies with energetic management teams come face-to-face with firms that are the entrepreneurial equivalent of AT&T, and often times it can be a bad combo.

Since the technical aspects of combining the respective firms technology strengths are well beyond my grasp, two articles found on the merger, here and here, lay out some of the bigger picture analysis of the combination.

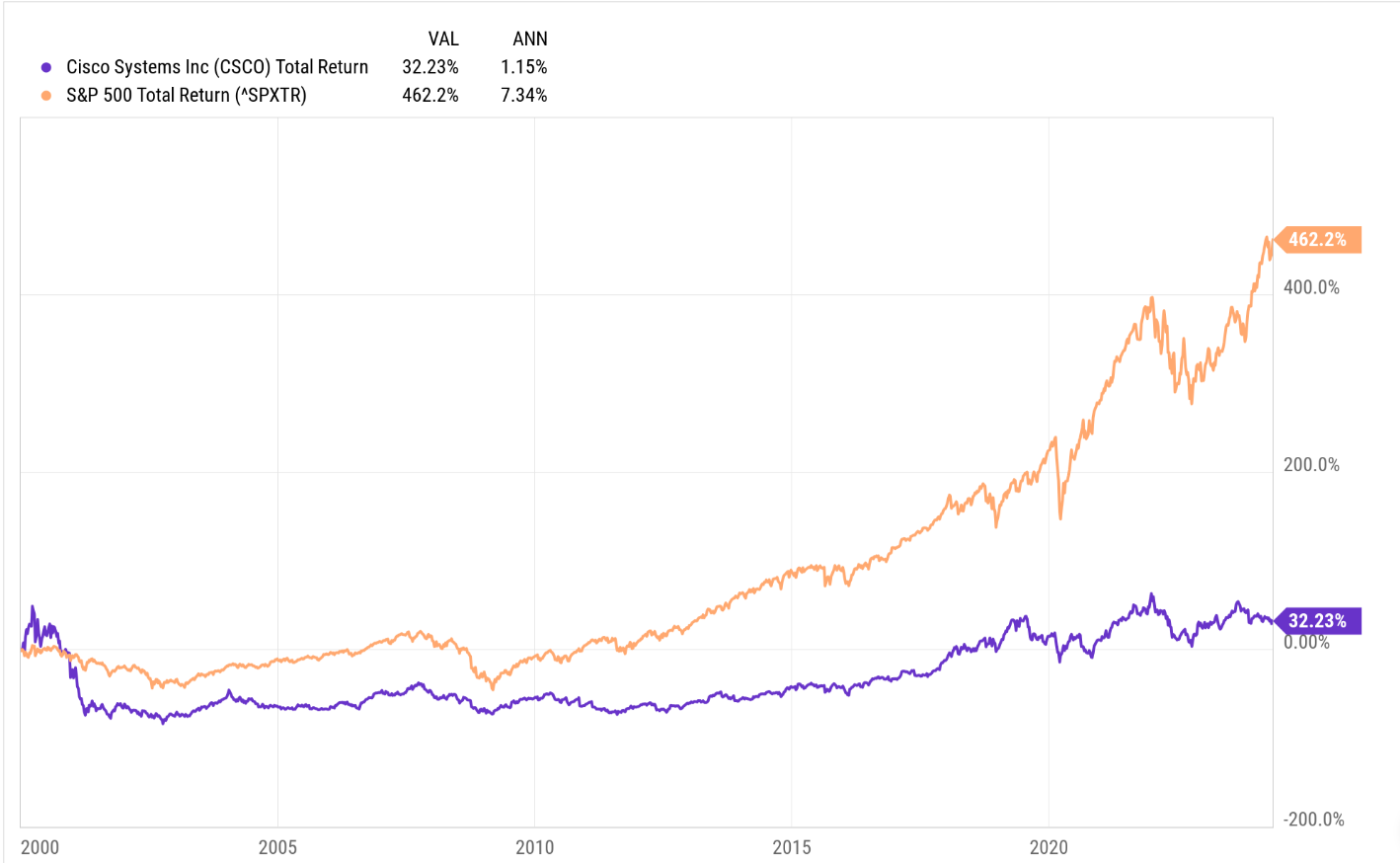

Cisco’s performance vs the SP 500:

This is a chart from Ycharts showing the relative performance of Cisco vs the SP 500 (total return) from 1/1/2000, to 5/10/24.

Cisco peaked at $82 per share in March, 2000. The highest it’s been since is $64 per share in January, 2022.

Basically the last two and half decades have been wildly different than Cisco’s 1992 to 2000 period, when it traded up to a $500 billion market cap.

From a portfolio construction standpoint, it can make sense to own stocks like Cisco since they can represent “uncorrelated” or quasi-value stocks (call it a non-momentum, or out-of-favor, or a dead money stock ) versus whatever is or are the popular tech and growth names of today. The problem with Cisco is you can find that kind of quasi-value and lower valuation equation in other sectors, without having to own a name like Cisco.

Summary / conclusion: Larger companies like Cisco do have the ability to re-engineer their business models and figure out ways to drive new growth, and in fact in tech it might be easier than other industries since winners and losers are created and then destroyed with so much greater frequency than in other industries.

One aspect that’s always bothered me about Cisco in the post 2000 world was they tried re-engineering the business, creating a Security unit and even pushing hard into software at one point, but nothing ever worked.

Is Splunk the magic acquisition ? What if the legacy networking business continues to shrink as it’s now 24 years after it’s revenue peak ?

Cisco has been “stuck-in-the-middle” (to use a Porter Competitive Strategy term) for 24 years.

It will be interesting to track the progress of Splunk’s integration into Cisco and what that will mean for the networking giant.

None of this is advice or a recommendation. Past performance is no guarantee of futures results. Investing can involve the loss of principal even over short periods of time. Any EPS, revenue or operating income data is sourced from LSEG.com.

Thanks for reading.