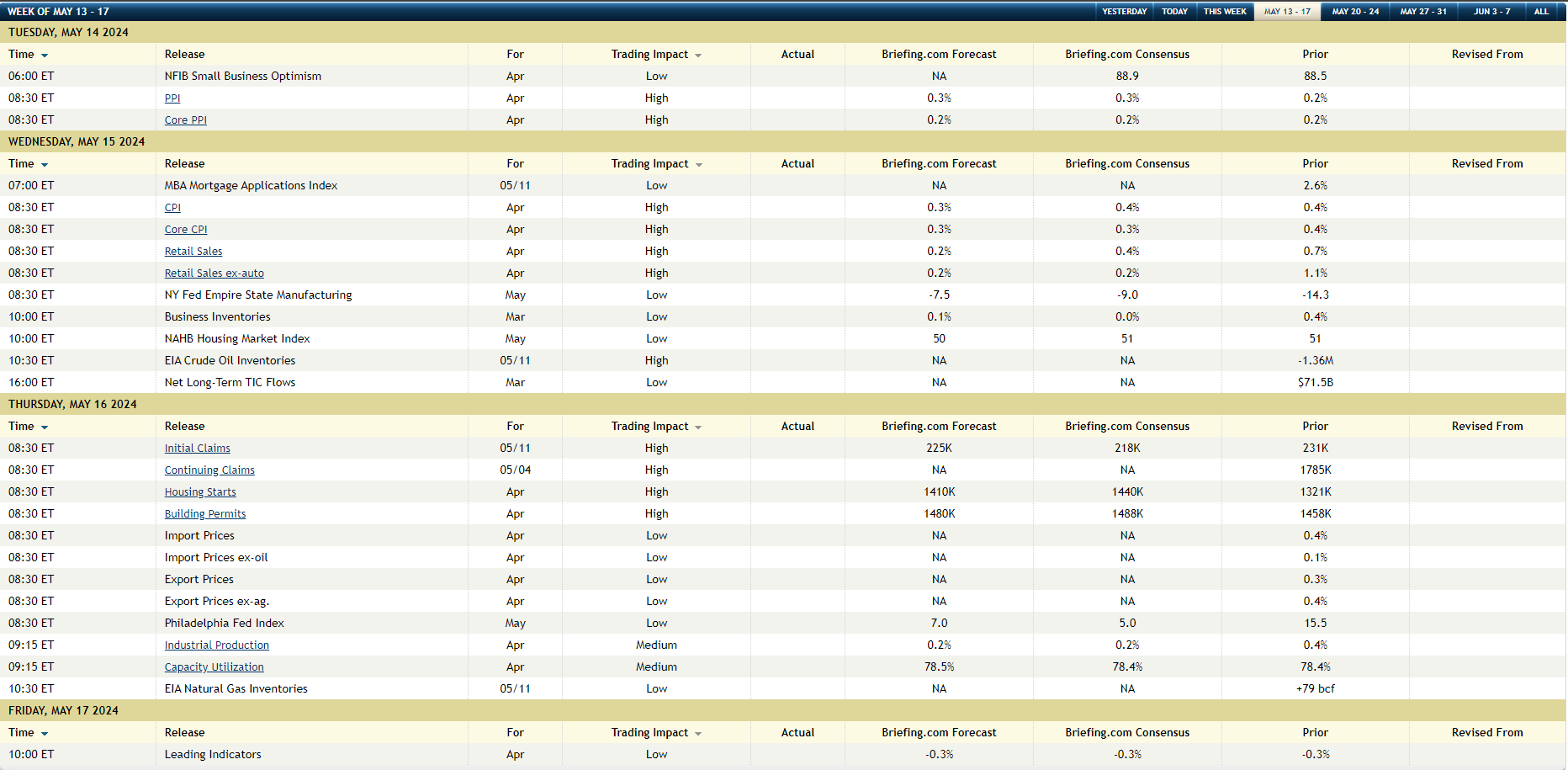

The above is Briefing.com’s weekly economic data table. April ’24 PPI and April ’24 CPI are due out Tuesday, May 14th, and Wednesday, May 15th, respectively.

Shelter or OER (owners equivalent rent) has a significant influence on the CPI given it’s weight (roughly 30% of the inflation gauge) and then add in auto insurance premiums, and the other troublesome areas, and it’s understandable why inflation remains stubborn.

With Friday May 10th’s, University of Michigan consumer sentiment data, “inflation expectations” ticked higher. That’s not a good thing. While the mainstream financial media remains obsessed with the inflation story, “inflation expectations” matters far more, and yet the mainstream financial media gives it little play, because expectations doesn’t get the visceral reaction that actual inflation gets.

Seriously, we want to see inflation expectations eventually move lower.

Here’s Briefing.com’s summary of the U of Michigan sentiment data (above graph) and the rise in inflation expectations data.

While the capital markets and the media react far more to the actual inflation data, ultimately it’s inflation expectations that matter more.

Crude Oil Still Matters:

While the mainstream financial media talks about the various inflation components, investors sometimes forget that crude oil still matters too.

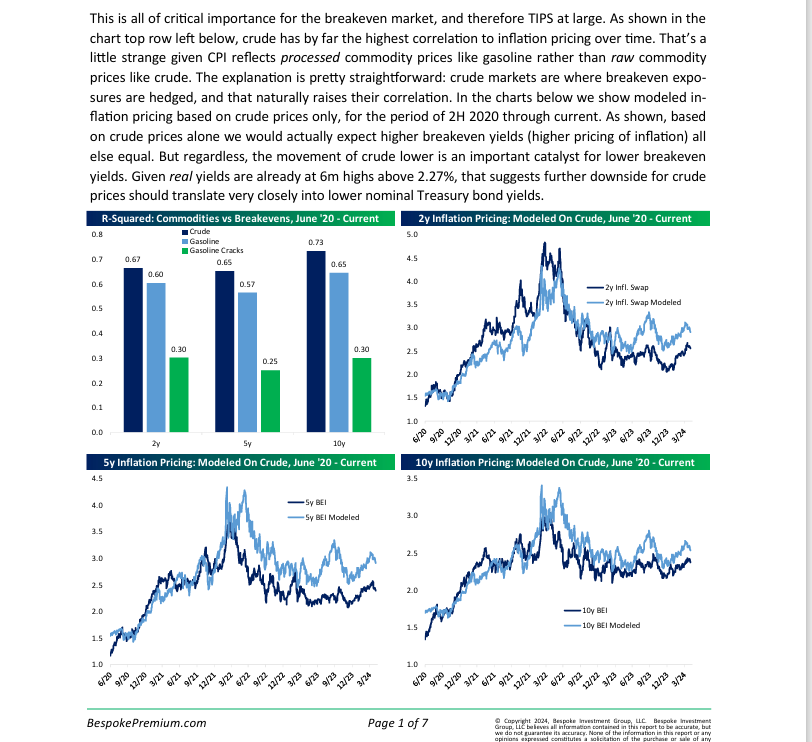

While these graphs are helpful from Bespoke’s Fixed Income Weekly of May 1 ’24, note Bespoke’s breakeven commentary above the graphs:

Without getting too wonky, since I’m not completely comfortable with some of the definitions myself, the “breakeven” is the rate or yield that supposedly solves for the rate increase needed (yield increase) for the 10-year Treasury’s return to equate to equate or be equal to the return of the 1-year Treasury bill.

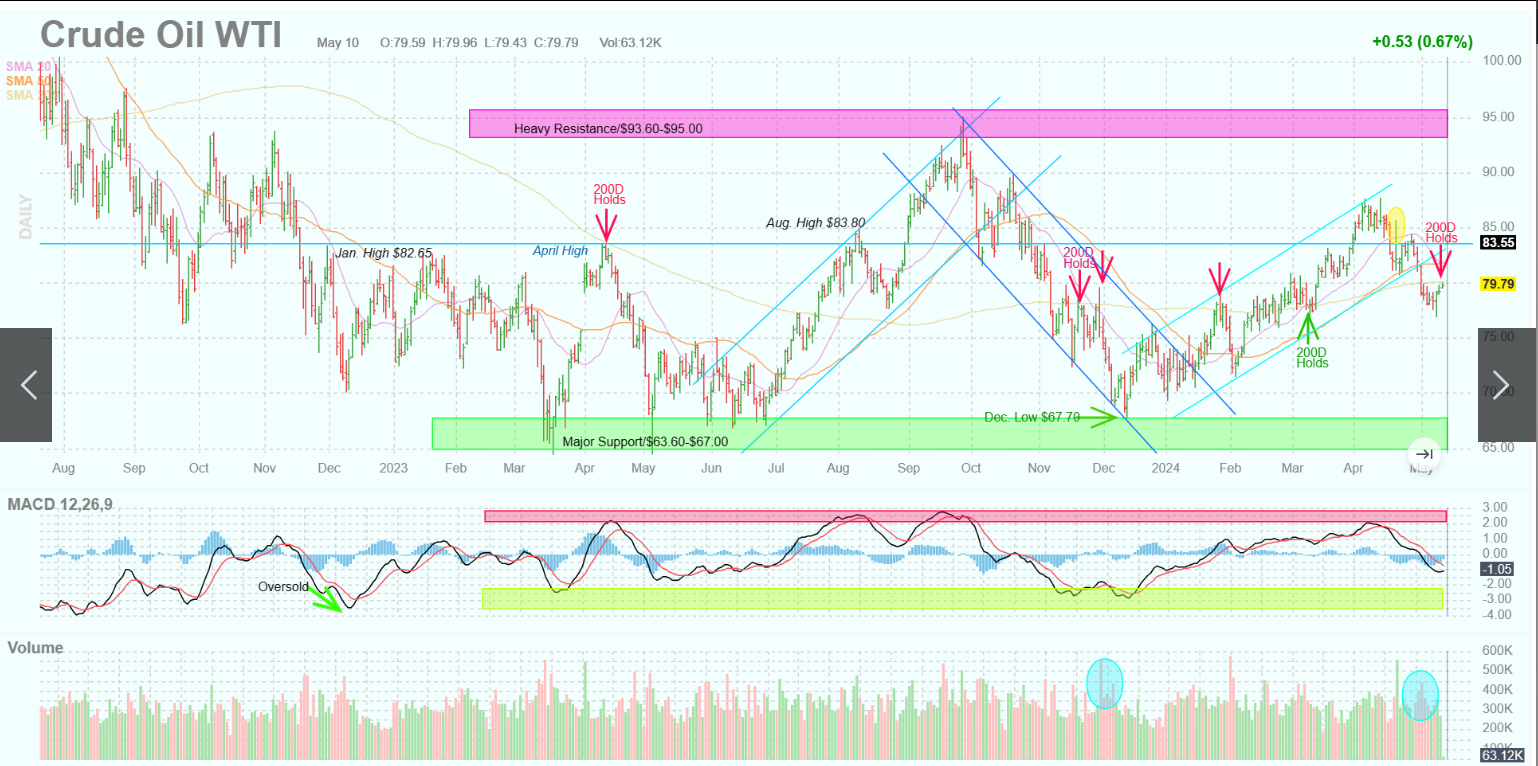

Crude oil chart:

This chart from this blog’s technician (X – @GarySMorrow) shows crude oil holding the 200-day last week. Reasonable investors who have been around the stock and bond markets for years have to know that any time there are Middle East tensions, crude oil gets bid up on the news narrative.

The point being that if a truce emerges in Rafah and the Middle East, and oil cracks, then Treasury yields should follow it lower.

The point being to all this is that even if the April CPI / PPI runs hot again this week, and the headlines look grim, watch the headlines out of Gaza and Israel. It’s an election year. A move in crude from the $80’s to the low $70’s, would help keep a bid in the Treasury market, and would help lower inflation expectations.

As Bespoke explained, crude oil still matters.

Corporate High yield credit spreads:

There is a growing awareness of the “tightness” of corporate high yield credit, which is eliciting more commentary in the mainstream media. Tighter high yield and investment-grade (often called high-grade) credit spreads usually occur with sustained periods of strong economic growth, as the US economy has seen since the pandemic ended.

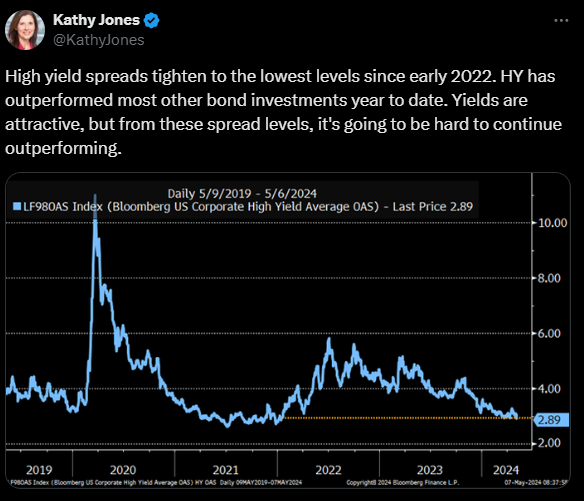

Here’s a good graph from Kathy Jones, Schwab’s Bond Market Strategist, on the relative performance of high-yield credit spreads over time. Lower spreads and lower yields on high-yield bonds, means better high-yield and high-grade bond returns, although for high-grade or investment-grade bonds, the interest rate risk is still a bigger driver of the bond or ETF’s return than the credit risk.

Kathy Jones and her Schwab team did a Fixed-Income update on May 2nd, 2024, and one of the pages on high yield (i.e. junk) credit spreads was worth noting:

Note the right side of the Schwab junk spread chart: at these OAS (option-adjusted spread) levels, the prospects for 12-month “excess returns” for the high yield asset class are diminishing.

Treasury vs credit – annual returns:

Finally, one last reference: this blog’s bond market annual return data from May 2nd, showed how the annual return for the TLT or the 20-year Treasury ETF, showed a barely positive 12 basis point return for the 10-year “annual” TLT return as of 4/30/24.

Almost all the 3-year annual returns for the various fixed-income asset classes are negative. Only a high-yield ETF (HYG) and a JPMorgan and BlackRock bond fund are slightly positive – in terms of annual return – for the 3-year time period.

Summary / conclusion: There is no question in the standard 60% / 40% balanced portfolio, the 60% is carrying the water in terms of total return this decade, while the 40% or the bonds / fixed-income / cash part of the portfolio is trying to “lose less” in a difficult monetary policy environment.

It’s clear “credit” is winning over what’s known as “duration” or interest rate risk. The more interest rate risk investors have taken, the likelihood that your 1 and 3 year bond allocation returns are negative, while if you have overweighted credit in its various forms (corporate investment-grade, corporate high yield, short-term muni high-yield, etc.) you fared pretty well relatively speaking to the benchmark.

So where does that leave us in mid-May ’24 ? This blog is not here to offer advice or recommendations, but only tell you how client accounts are invested, and this blog has client accounts mainly split down the middle with each risk, but when Treasuries get oversold, like they did recently in late April ’24, then smaller positions are added to the TLT, the TIPS (Morningstar posted an article recently noting that TIPS are undervalued) and the AGG. As the various charts and graphs above indicate, the corporate high yield market is reaching credit spread extremes in terms of spread tightening, so readers should evaluate their high yield credit exposure and make sure they know just how much high yield they own.

The last time the Federal Reserve eased (i.e. lowered the fed funds rate) was in 2019, and the TLT returned +14%. Duration will work, but it might be for briefer periods.

Understand this though – because of zero interest rates from 2008 to 2016 – there is no guarantee that the extreme annual returns seen for the last 3 years and – for the TLT specifically – the last 10 years, won’t last considerably longer. It’s all about the cycle. It could remain a tough decade for interest-rate sensitive bonds, and high-yield and investment-grade credit could remain well bid for years.

JPMorgan’s David Kelly still has the key “macro” summary of the US economy when he noted in the last month or so, that the US economy remains free of the “excesses” that plagued the domestic economic landscape the last 20 – 25 years. Even thinking of China, which grew at 15% per year from the early 2000’s through 2012 or so, has returned to about as close to normal state as you can expect a Communist economy to grow.

This blog post was much wonkier and far longer than the original intent. None of this is advice or a recommendation. Past performance is no guarantee of future results. Investing can involve the loss of principal even for short periods of time.

Thanks for reading.