Despite the worries over the regional bank credit situation this week, it didn’t seem to impact the forward estimates for the financial sector or the SP 500 in general, although the small bank and the small bank/financial index doesn’t really have an impact on the SP 500 in terms of earnings weight.

- The forward 4-quarter estimate for the SP 500 increased this week to $294.32 from last week’s $293.87.

- The PE on the forward estimate is now 22.6x versus the 22.4x from last week, and the 21.8x to start the year.

- The 10-year Treasury yield has now dropped for weeks in row from 4.19% to 4.02%.

- The SP 500 earnings yield at week’s end was 4.42% versus last week’s 4.48%.

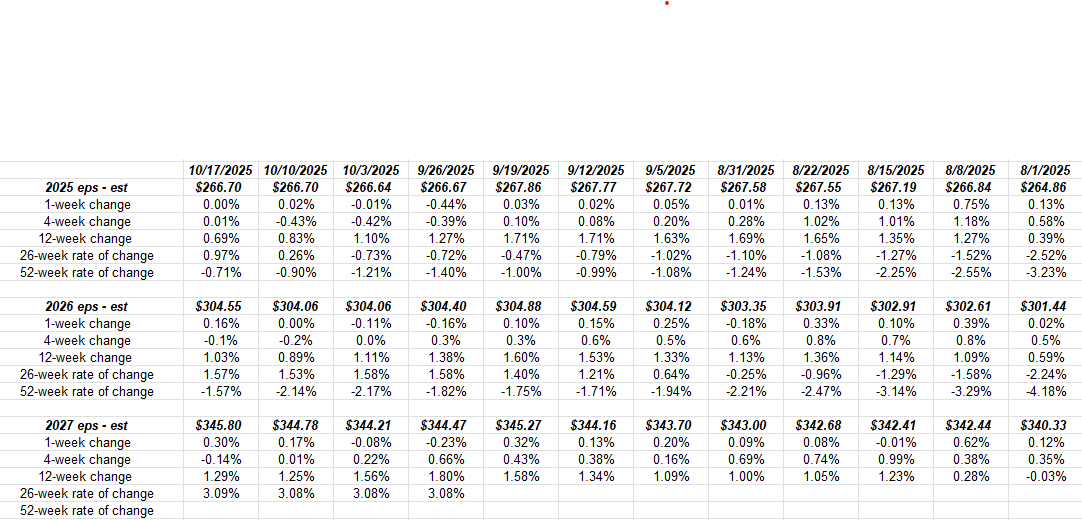

This table from an internal spreadsheet shows the rate-of-change for the 2025, 2026, and 2027 annual SP 500 EPS estimates.

What’s interesting to me is the continued steady rise in the 2026 and 2027 estimates.

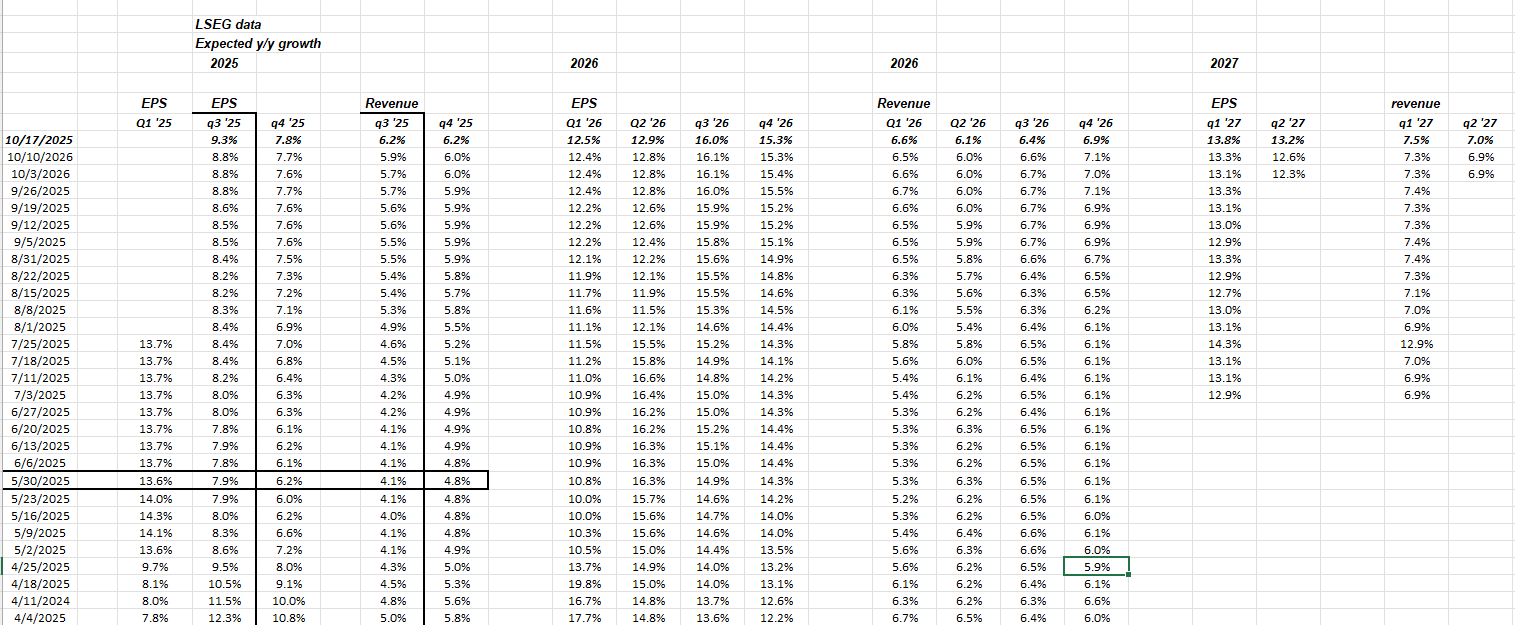

Another look at quarterly SP 500 EPS and revenue growth rates:

In Q2 ’25, SP 500 EPS grew 13.8% y-o-y, by the time the 3rd quarter ended September 30, ’25.

The tech companies will influence the expected 3rd quarter SP 500 EPS growth rate over the next two weeks, but Q3 ’25’s expected growth is already +9.3%, so another 450 bp’s and the 2nd quarter’s EPS growth is beaten.

Nothing seems to have slowed SP 500 earnings growth, not tariffs, not the gov’t shutdown, not worries over the overseas conflict in the Middle East: it’s been a bulletproof market this year.

Crude oil looks ready to breakdown and that should help the 10-year Treasury yield trade through 4% and allow the Fed some breathing room on inflation. It was talked about in last week’s post here.

This chart from technician Gary Morrow shows that – perhaps – the USO is nearing support at a gap fill (blue line) and maybe crude oil won’t break lower much further.

Summary / conclusion: The SPDR Regional Bank Index (KRE) held support Thursday and Friday, 10/16 and /17, after worries about private credit at some of the regional banks. The 200-week average for KRE is $56.83 per the Worden charts, which is this blog’s line-in-the-sand on what to do with KRE.

The SP 500 actually finished higher this week by 1.70% despite worries over credit and the spike in the VIX.

The strong upside surprises this week in the larger banks and brokerages like JPMorgan, Goldman Sachs, etc. no doubt helped sell-side analysts boost forward estimates again for the SP 500.

Two growth stocks reporting this week are Netflix (NFLX) and Tesla (TSLA), while two older tech giants – IBM (IBM) and Intel (INTC) – also report later in the week.

Amazon, Alphabet, Microsoft and Apple all report the last week of October.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. LSEG is the source of all revenue and EPS estimates used in the weekly earnings update. None of this information may be updated and if updated may not be done in a timely fashion.

Thanks for reading.