Running the estimates and updating the spreadsheet last night after last week’s Q3 ’25 financial results for Charles Schwab (SCHW), it’s surprising that the stock didn’t get a better boost from last week’s results, but looking at the new EPS and revenue estimates for Chuck – post earnings – it’s a reasonable estimate that the stock is at least 25% undervalued, and possibly 50% depending on how the next few quarters unfold.

EPS revisions:

After Schwab reported a fairly good Q3 ’25 quarter, with net revenue growing 16% y-o-y, pre-tax income growing 25%, and EPS growing 31%, here’s how the forward EPS estimates were revised after the release was fully-digested:

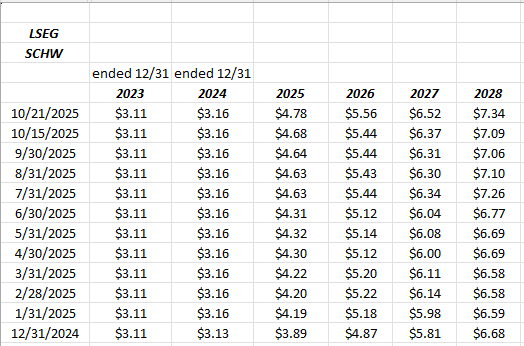

- 2025 EPS estimate increased to $4.78 from $4.58

- 2026 EPS estimate increased to $5.56 from $5.39

- 2027 EPS estimate increased to $6.52 from $6.16

The “from” estimates are the EPS estimates after Schwab released Q2 ’25 results, so somewhere from mid to late July ’25.

This table from LSEG shows how Schwab’s EPS estimates have been revised each month, starting with December 31 ’24.

Source: LSEG estimates.

Note the jump in the EPS estimates from June 30 to July 31, which is similar to what the Sept 30 to October 31 estimate should look like after October ’25 ends.

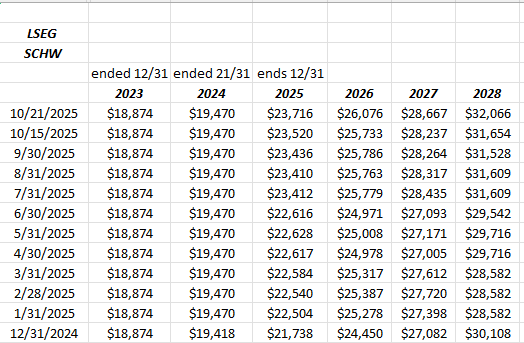

Net revenue revisions:

While not nearly as “robust” as the EPS estimate revisions, Schwab’s net revenue revisions are still positive.

Valuation:

Morningstar’s valuation on SCHW after last week’s results saw a bump from $105 to $109, which – in my opinion – is still too low.

This blog’s spreadsheet model which uses a “price-to-book” divided by ROE to arrive at a target PE, shows Schwab is fairly valued at $144 per share, which is – in my opinion – is probably too salty.

Using an average of the two models, Schwab trading at $95 – $96 means the stock is probably 25% – 26% too cheap to fair value.

It needs to be the topic of another post, but ROE is a very important metric for financial stocks, and Schwab’s ROE has consistently been in the mid-teens range.

Post-publishing addendum: After hitting the “publish” button, I realized i left off some of the most compelling valuation metrics: at $95 per share, and after updating the EPs estimates Schwab is trading at just 20x 2025 EPS and 17x expected 2026 EPS, for EPS growth over the next two years of 47% and 16%.

Expected revenue growth this year and next is 21% and 10%.

So you can buy Schwab today in October ’25, which is expected to grow full-year ’25 EPS and revenue by 47% and 21%, for a 20x multiple.

Think about that.

Summary / conclusion: While JPMorgan is this blog’s largest financial holding, Schwab (SCHW) is the 2nd largest and is certainly a better value than JPM, given it’s price. (There’s nothing wrong with JPM after least week’s earnings, but the stock has the highest book value valuation of all eth major banks, and Jamie Dimon will likely be departing in a few years.)

Years ago, about 80% of Schwab’s valuation was driven just by net interest income, but after the TD Ameritrade merger, Schwab’s “net interest income” as a percentage of total net revenue has fallen to 27%, which means revenue is more diversified and Schwab is much less dependent on the yield curve shape than it was historically.

Given that 80% figure above, 2008 to late 2016 were tough periods for Schwab where money market fees had to be waived thanks to the “zero-interest-rate policy” (ZIRP) after 2008, and then again around Covid from 2020 to 2021.

The point being that – in my opinion – Schwab today is in a much business and financial position than at any point in the last 20 years, but the stock still seems to trade like it’s 2015.

One surprise in the latest earnings release last week, was the amount of shares repurchased. Schwab never was a big share repurchaser, and was always very disciplined about capital allocation. SCHW has repo’ed $2.7 bl shares YTD as of 9/30/25. That’s a good sign, both in terms of the excess capital, and Schwab’s willingness to return it to shareholders.

Maybe the 25 basis point rate cut next Wednesday, 10/29, will finally catalyze the stock, particularly if the Treasury yield curve steepens.

Today, an expected 3.875% fed funds rate with a 10-year Treasury yield of 3.99% – 4%, doesn’t allow the financial sector to capture the “ride the yield curve” spread that existed for decades.

Schwab’s earnings power is telling you the stock is too cheap, and with the pre-tax margin backs into the low 50% area, I would have expected the shares to reflect some of these positive forward EPS revisions. SCHW’s stock is up 29% YTD as of Monday’s, October 20th close, however technically, the stock has not broken out above it’s early ’22 series of highs near $95 per share, just prior to the Fed’s tightening of monetary policy in 2022 and 2023. Since early 2022, Schwab’s stock has underperformed the SP 500.

Be patient.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. This blog has followed and modeled Schwab since the 1990’s. None of this information may be updated, and if updated, may not be done son in a timely fashion.

Thanks for reading.