Usually this blog sees more frequent posts and updates on a whole spate of investment areas and topics, but an early December ’24 fishing trip to Florida and then a long-awaited knee-replacement surgery that was badly needed in order to continue some of the various exercise and workout activities I’ve engaged in since my mid-40’s, has left fewer posts for clients and readers.

This week, saw a return to a more-normal workload, which meant getting ahead of the Nike (NKE), FedEx (FDX) and Micron Technology (MU) earnings reports of last week.

Nike remains the favorite of the three stocks, while FedEx was sold the vast majority of client accounts on Friday, December 20th, ’24, and no Micron, or Nvidia or the SMH has been owned for months. (More articles are forthcoming on each of these three names in the coming holiday week.)

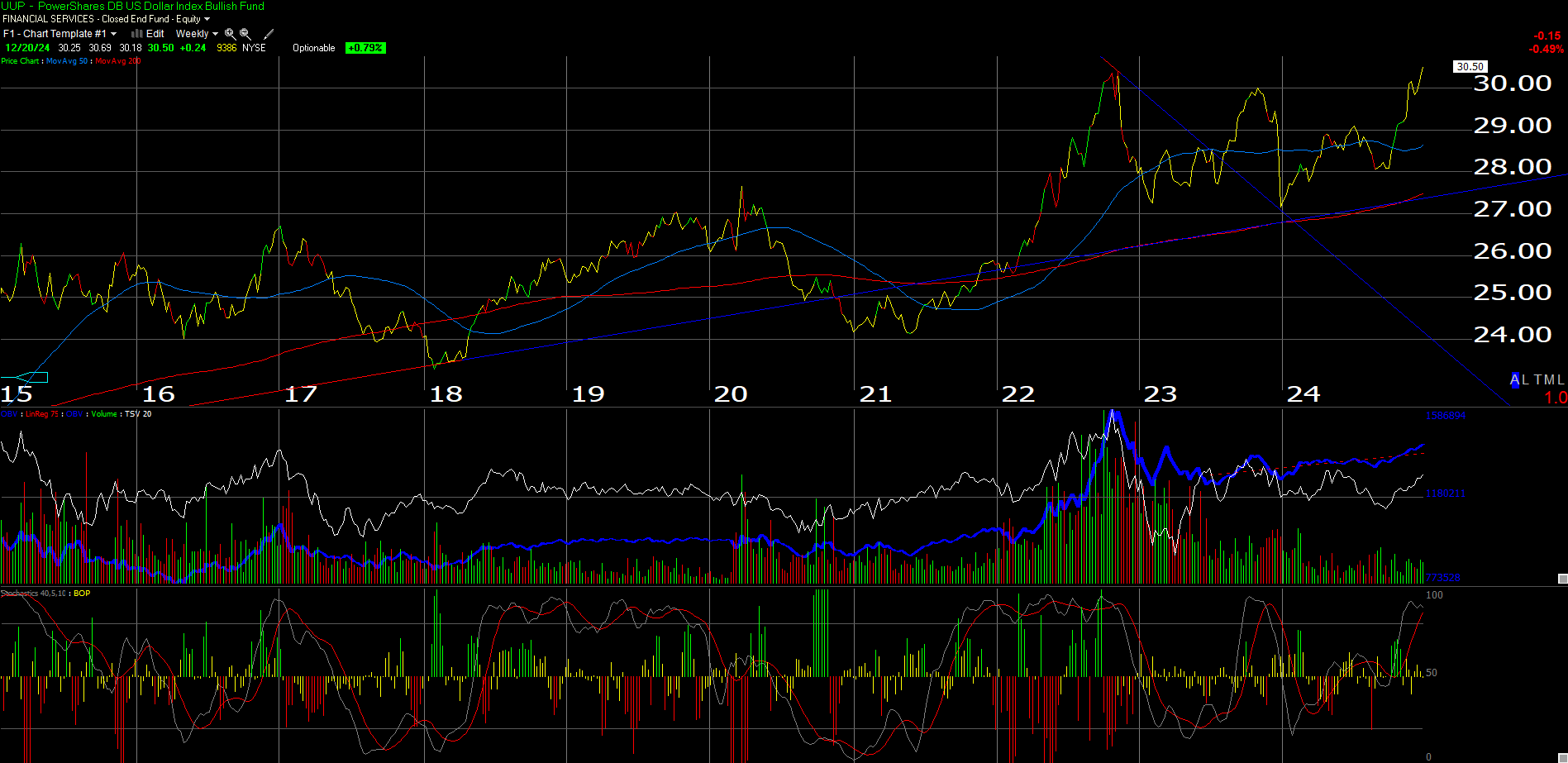

While updating spreadsheets and year-to-date returns for client portfolios this weekend, what jumped out at me was the incredible US dollar strength after the Wednesday, December 18th, ’24 FOMC meeting, and that strength’s impact across various asset classes.

Weekly chart of the UUP:

Source: Worden 2000 (click on the chart to expand / enlarge)

The UUP composition per the Invesco website consists of US Dollar forward contracts (USDX) which are comprised of :

- 58% Euro

- 14% Japanese yen

- 14% British pound

- 9% Canadian dollar

No UUP is owned for clients since it generates a K-1.

Most traders use the DXY as their dollar proxy and after the FOMC announcement Wednesday, December 18th, 2024, the US dollar index (DXY) rose to 108.15, while the same FOMC announcement drove a 13 bp increase in the 5-year Treasury yield to 4.38%, the 10-year Treasury yield rose 11 bp’s to 4.49% and the 30-year Treasury yield rose +8 bp’s to 4.66%.

Here’s the last two-week change in the Treasury security complex in terms Treasury yields:

- 2-year Treasury yield increase: +20 bp increase over two weeks;

- 5-year Treasury yield increase: +34 bp increase over two weeks;

- 10-year Treasury yield increase: +37 bp increase over two weeks;

- 30-year Treasury yield increase: +39 bp increase over two weeks;

Those are sharp drops in Treasury prices and increases in Treasury yields, as the mainstream media seems pre-occupied with rising inflation, or least not yet seeing the kind of “disinflation” that was hoped for earlier in 2024.

Higher Treasury yields attracts foreign capital (particularly as the ROW (rest of world)) central banks are cutting rates, hence the US dollar rises as a result of better absolute yields in the US.

The lesser-known impact of prolonged US dollar strength is that it tends to be “disinflationary”. That should eventually help the SP 500 in 2025, but these lags are tough to quantify and hard to pinpoint exactly.

About 45% of the SP 500 revenue is “non-US” and roughly 55% of the SP 500’s technology sector revenue is also non-US, so this bout of recent dollar strength could be having a marginal revenue impact on the SP 500’s largest sector, at least in terms revenue growth.

The Friday, November 20, ’24 release of the November Core PCE was inline, and seemed to be liked by the US Treasury market, as yields rallied following the report. At a JP Morgan conference in Oak Brook, Illinois, in the spring of 2023, with the proliferation of all the inflation data and new indices that have been produced since the inflation surge following COVID and the pandemic, when Jack Manley (JP Morgan Global Equity Strategist) was asked what inflation indices should be prioritized he stated definitively, “the Core CPI and the Core PCE”.

Watch the Core PCE data which is typically reported the last week of every month. The December Core PCE data will next be released in late January ’25.

Summary / conclusion: The upshot of the US dollar update is that if you follow the UUP, it looks as if the US dollar COULD be putting in a long “double-top” technically, and if the US dollar would gradually weaken, this development would likely be a plus for US stocks, international stocks, and US bond market asset class returns looking forward into 2025 and 2026.

In 2022, the overall capital market pattern seen was a tightening Fed, higher rising fed funds rates, higher Treasury yields across the term structure (i.e. the Treasury yield curve) and lower stock prices.

The same pattern has emerged in the last few weeks, as SP 500 breadth has deteriorated.

My own opinion is that the Fed will continue to reduce fed funds in 2025, to below 4% (which by their own admission is still too far above neutral), but the critical element is whether the longer-end of the Treasury curve from 5-years and longer start to rise in fall and yields as well.

As an anomalous outlier, the Gold (GLD) ETF, is up 26% YTD as of December 20 ’24, even though the US dollar continues to be very strong. I grew up on the “dollar strong, gold weak” correlation that lasted from 1980 to 2000 in that record bull market for stocks from 1982 – 2000. The correlation between the US dollar and gold and US stocks seems much different today, but that’s a longer article for another time.

This blog is less bullish for the SP 500 for calendar 2025, but a weaker dollar could help mitigate or ameliorate weaker equity returns in calendar 2025 if they should materialize.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Any information contained above, may or may not updated, and if updated, may not be done so in a timely fashion. LSEG did not publish their weekly “This Week in Earnings” or “Earnings Scorecard” this week, which are the two primary sources of the weekly SP 500 earnings update, so no update on SP 500 numbers were published on this blog this week. Hopefully, TJ Dhillon of LSEG can get an update out over the Christmas week.

Thanks for reading.