Nike reported their fiscal Q2 ’25 financial results last Thursday night, December 19th, ’24, and despite the tough guidance for the last two quarters of fiscal ’25, primarily due to inventory re-alignment, the best sign for the stock was that despite the tempered outlook, and expected margin compression, the stock finished almost unchanged in trading Friday, December 20th, on nearly 3x average daily volume, (33 million shares traded versus the 12 million average).

If readers would look at how Micron (MU) traded after Wednesday night’s fiscal Q1 ’25 earnings release, and how FedEx (FDX) traded Friday, December 20th, stocks that don’t go down on bad news, are as telling as stocks that drop sharply after a great quarterly report.

So much of trading and even the longer game of true investing is based on “expectations” around sentiment, around earnings, around management, and even around guidance, etc.

Nike peaked at $180 per share in November ’21, and is still well below the 50% decline mark, and just may be getting thoroughly washed out, in terms of unanticipated bad news.

Here’s a quick re-hash of Nike Q2 ’25 financial metrics:

- Revenue beat the estimate by 2% for the quarter, while EPS beat it’s consensus estimate by 24% (and operating income beat by 57%), as revenue fell 9% y-o-y (constant currency based), operating income fell 24% y-o-y and EPS also fell 24%;

- Gross and operating margins fell 100 bp’s and 240 bp’s y-o-y respectively in Q2 ’25, much of this Elliott Hill (new Nike CEO) noted would continue to pressure margins until Q4 ’25 or the May ’25 quarter end;

- Because Nike does not publish a cash-flow statement with earnings, even though the rest of the world’s great brands do, i.e. Coca-Cola, Apple, Nvidia, Tesla, etc. it looks like Nike generated $500 million in free-cash-flow for fiscal Q2 ’25, up slightly from last quarter’s $274 million, and undoubtedly pressured by the inventory liquidation;

Note this: Nike’s operating income has fallen y-o-y for 10 of the last 13 quarters.

Comparing margin metrics when Nike was trading at $180 per share in late ’21, versus today’s margin metrics with the stock at $80 per share, where’s what’s happen to gross and operating margins since:

- Gross margin: late ’21 average about 46.5%, versus today’s 43.6%;

- Operating margin: Late ’21 average of about 15% versus today’s 11.20%;

- Price to cash-flow and free-cash-flow valuation in late ’21 of 38x and 40x versus today’s P/CF and P/FCF valuation of 18x and 22x;

- Price-to-sales valuation today of 1.86x versus the late ’21 valuation of 4.86x

Here’s the real problem though:

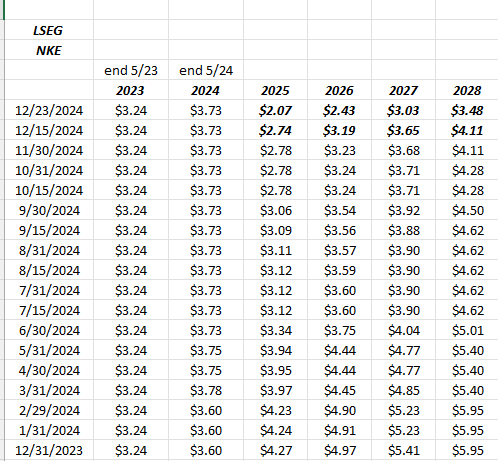

Nike EPS estimate revisions:

Source: LSEG

Have to be frank with readers and say right upfront these are brutally ugly downward revisions to Nike EPS estimates for fiscal ’25, ’26 and ’27.

Doing the quick math, that’s a 25% one-time negative revision for fiscal ’25, a negative 24% revision for fiscal ’26, and a 15% negative revision for fiscal ’27.

That’s grim.

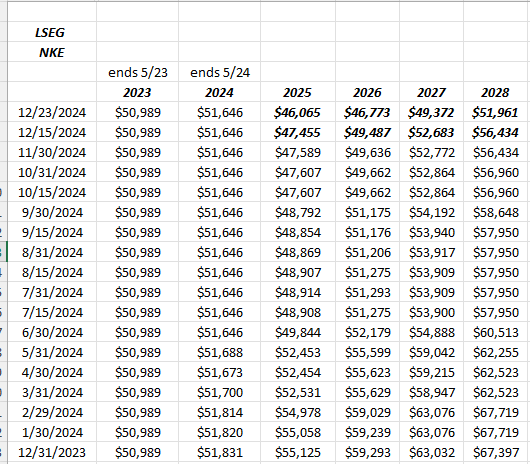

Nike revenue estimate revisions:

Just since 12/15/24, the fiscal ’25 revenue estimate has been revised lower by -3%, the fiscal ’26 estimate by -5%, and shockingly, the fiscal ’27 estimate by -6%.

Personally, I didn’t expect to see that since the main Nike problem today is still inventory, and – well – excess inventory, and you’d expect management to be able to bite the bullet, take the margin and cash-flow hit and get the old product out the door.

These negative estimate revisions smack of analyst worry about longer-term consumer demand and the lack of innovation about the Nike product line.

Summary / conclusion:

The price action in Nike’s stock last Friday, December 20th, ’24, despite the revenue and margin guidance was actually encouraging, but I wasn’t prepared for the degree of downward revision to Nike EPS and revenue estimates for the rest of fiscal ’25 as well as fiscal ’26 and fiscal ’27.

Fiscal ’25 with two quarters remaining in the fiscal year how expects a 48% decline in EPS (for the full year) on an 8% revenue drop y-o-y.

This blog has modeled Nike EPS and revenue growth since 1992, and in the 33 years between fiscal ’92 and fiscal ’24, Nike has only seen 4 years of negative revenue growth y-o-y, and that was 1994 (-4%), 1999 (-8%, brown shoe craze was the reason), 2010 (-1%, assuming due to global slowdown post 2008), 2020 (-4% Covid driven).

The inventory liquidation will impact earnings, revenue and cash-flow for the rest of fiscal ’25 (ends May 31), that much was clear from Elliott Hill, Matt Friend (CFO) and the rest of the Nike team. Underneath all this inventory liquidation, Elliott needs to restore “Nike energy” to the brand and be innovative and create buzz around the fiscal 2026 product line, and judging by the tenor of the conference call notes, I thought Elliott Hill – like any good CEO – was hesitant to “overpromise” on that front.

The stock is down 60% from its November ’21 all-time-high near $180 – $181. This correction is similar to the late 1990’s “brown shoe craze” (sorry about the name but that’s what it was called at the time, as consumer shoe preferences shifted away from the Nike brand towards what were then mountain hiking boots and more non-athletic footwear).

Nike’s stock was under water from the late 1990’s through 2003 when a number of issues internally were fixed, like the supply-chain, like an expansion of the Nike footwear brand, etc.

Technically, I’d prefer the stock to remain above the July ’24 near $70 – $71 and NOT trade through $70 on heavy volume. One technician that this blog follows thinks $60 is the ultimate technical support for Nike.

This blog has it’s biggest position in Nike in the last 15 years the last year thanks to the much more reasonable valuation. It’s still not “absolutely” but on a 25-year relative valuation measure, the stock sports a 4% free-cash-flow yield and a 2% dividend yield, for the first time in years. Clients have cost basis positions between the $70’s and the $125’ish range.

Morningstar puts a “fair value” on Nike around $115 per share, meaning the stock is thought to be undervalued by 33% as of Monday, December 23rds’ open.

Investors can expect the next two quarters to remain grim, thanks to inventory liquidation a still weak China. China revenue has fallen -4% and -8% the last two quarters, while China EBIT has fallen -4% and -27% the last two quarters. (China revenue is roughly 14% of Nike total, while China EBIT is 28% of Nike’s total EBIT in the last quarter.)

Some tax-loss selling may be done before year-end ’24 in taxable accounts, and some small allocations of Nike might be bought for those accounts with the biggest loss just to reduce cost basis over time.

There is no question the stock price reaction to an ugly quarter is a positive. As old traders and portfolio managers say frequently, “price (action) is everything.”

Today, Nike will remain a longer-term position, for clients, but that could change quickly.

None of this is advice or a recommendation, but only an opinion. Performance is no guarantee of future results. This information may or may not be updated, and if updated may not be done in a timely fashion. Investing can and does involve the loss of principal, even for short periods of time. Nike revenue and EPS estimates are sourced from LSEG.

Thanks for reading.