While most of the mainstream media focuses on the technology reports this coming week, Boeing (BA) might be the most interesting company from an “expected forward return” perspective.

Boeing peaked at $446 in March of 2019, shortly after the two plane crashes (Lion Air in October, 2018, and Ethiopian Air in March, 2019) and before Covid sent the stock into a multi-year tailspin. Today, as of January 23 ’26, BA is down 43% from it’s all-time-high in March, 2019, and fighting it’s way out of a monstrous mess, mainly of it’s own doing, but Covid didn’t help either.

Last quarter, when Boeing reported their calendar Q3 ’25, the stock was hammered on the news that the 777-9 was pushed into Q1 ’26, and the larger-then-expected charge on the 777 (per Morningstar).

Here was this blog’s earnings preview, and the follow-up review after the stock drop and after Boeing reported the quarter.

What’s interesting is that after the very dour earnings report and the stock price reaction, just 5 weeks later Boeing management noted at a UBS conference that the aircraft manufacturer expected:

1.) Low-single-digit free-cash-flow growth in 2026.

2.) BA expects 737 and 787 deliveries to be up in ’26.

But the reaction of the stock was positive to this news, since, after the 777-related comments in late October ’25, when the stock was trading near $225 prior to earnings, the stock dropped all the way to $176 by late November, only to start rebounding after the UBS conference comments in early December ’25.

Here’s the detail on the early December ’25 conference guidance from the SeekingAlpha news blog:

Boeing (BA) +8.9% in early trading Tuesday, flying to the top of the S&P 500 leaderboard, after CFO Jay Malave said the company expects positive free cash flow in the “low single digits” next year, reversing the company’s $2 billion cash burn in 2025, in the first detailed look at the company’s cash projections for 2026.

The new CFO still expects Boeing (BA) will eventually reach the $10 billion cash generation target outlined by the previous management team, citing steadily improving production in its factories, especially for the 737 MAX and 787 Dreamliner jets, the reduction of inventory of undelivered aircraft, and an improving business at its defense and services operations; he also expects the 737-10 narrowbody jet to be certified later in the year.

Analysts expect Boeing (BA) to generate $2.46 billion in free cash flow in 2026, according to estimates compiled by Bloomberg, which would mark a turnaround from the cumulative $2.25 billion cash outflow recorded during this year’s first nine months.

Boeing’s (BA) free cash flow has not been positive on an annual basis since 2023, and the company has lost a cumulative $39 billion in the five years through 2024, including $11.8 billion last year. (End of quote).

————-

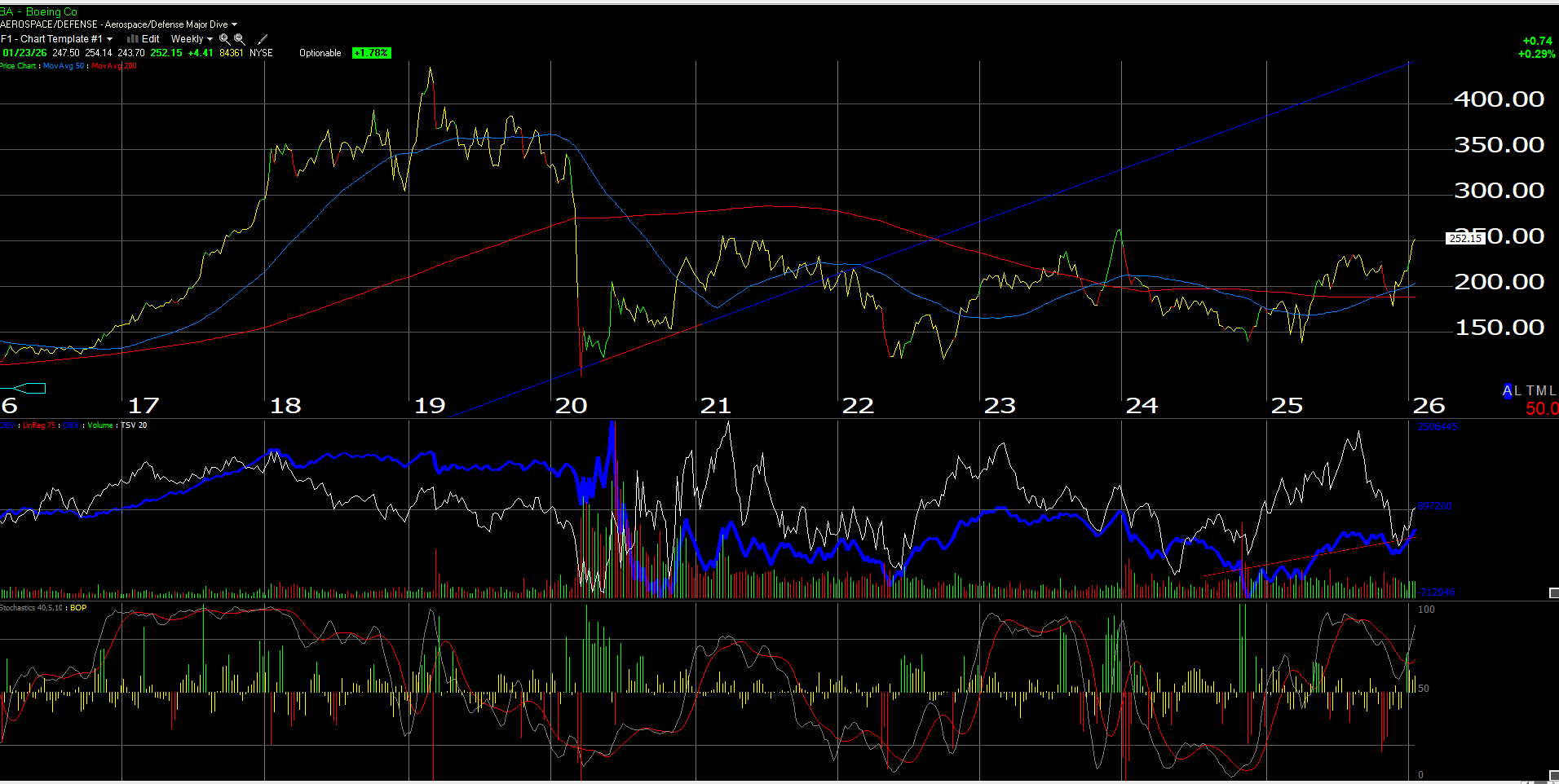

Since early December, ’25 BA’s stock has risen from the $175 area to the $252 area as of Friday, January 23, 2026.

While the stock is very “overbought” on the daily chart, the weekly chart for BA shows the stock less exuberant (so to speak).

(Worden chart)

The next key technical level for Boing will be the $265 – $257 highs from late 2023. Above those levels on good volume and Boeing will be trading at it’s best price levels since early 2020.

So why the concern ?

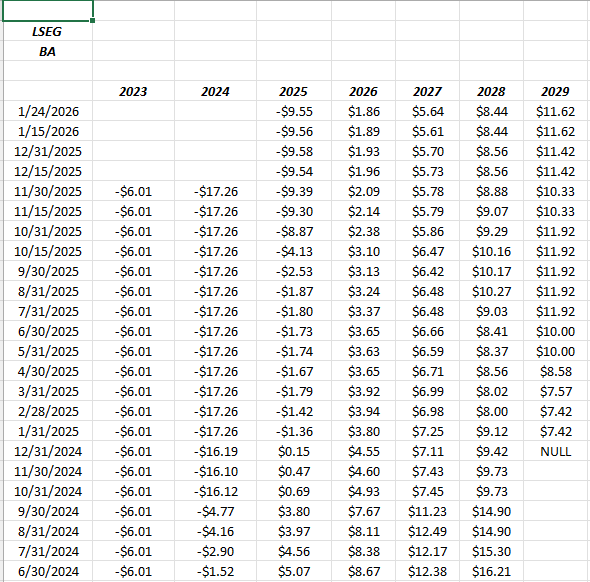

Despite the Trump Administration’s best efforts to negotiate tariff deals with foreign countries that include commitments for these countries to buy Boeing airplanes, the trend in the consensus EPS and revenue estimates is less than joyous:

BA EPS estimate revisions:

(Source LSEG I/B/E/S)

Those are grim declines in expected earnings: 2026 expected EPS as of today is down 79% since June ’24. Expected 2027 EPS is down 55% from June ’24 and – well – not that it matters but expected ’28 EPS is still down roughly 50%.

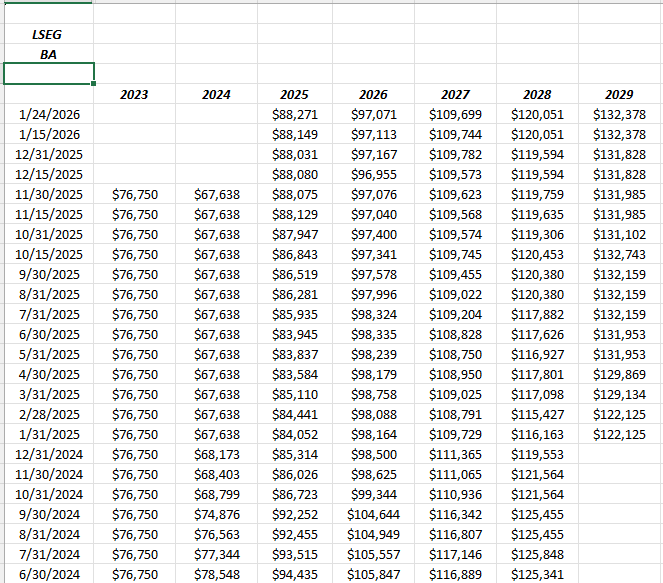

BA revenue revisions:

As readers can see, expected revenue revisions are not nearly as steep in terms of revisions as EPS indicate, which is typical of capital-intensive industries with large manufacturing footprints.

The revenue revisions are actually a good sign, but the revenue revisions have to turn positive at some point, since a large manufacturing concern like Boeing must generate positive revenue growth to “lever” operating income and EPS.

Still, it’s somewhat surprising to see that with the airplane purchase commitments coming from foreign countries with the trade deals signed in 2025, the revenue revisions have yet to turn positive.

Hmmm.

Valuation:

A Boeing valuation discuss today is really a projection as to what the company’s financials look like in 3 – 5 years:

Here’s the next 3 years “expected” calendar EPS for BA as of January 23 ’26, and the multiple based on Friday’s market close:

- 2028: $8.44 = 30x multiple

- 2027: $5.64 = 45x multiple

- 2026: $1.86 = 135x multiple

Looking at historical BA financials back to the year 2000, the financial history seems to indicate that the stock tends to peak when BA hits a 10% operating margin (O/M).

Looking at Boeing’s peak year of EPS and revenue growth looks to be 2018, when BA printed $101 bl in revenue and $17.85 in EPS, which is pretty remarkable since the EPS number implies a 20% net margin, but looking at the 2018 10-K, in fact net earnings were $10 billion, and thus the net margin was closer to 10%.

The 2026 consensus revenue estimate for BA is $96 billion, just $5 bl short of the 2018 record revenue print of $101 billion, so to assume BA could reach a 10% net margin in ’26 of $9.6 billion would be remarkable indeed.

Morningstar’s fair value on BA is $246 as of this writing so – at least according to Morningstar – the stock is fairly-valued today. Morningstar’s operating margin estimate is 12% so it’s actually a little higher than this blog’s assumption of 10%.

My own opinion is that BA should be able to get to $300 per share. When the operating leverage turns, and cash-flow generation greatly improves. the credit rating should be bolstered and the EPS should improve dramatically.

You can’t help but think that with the last 6 years for the stock, the sell-side analyst EPS expectations are still quite subdued.

BA’s one particular problem right now is Boeing’s senior unsecured credit (i.e. debt) rating with a Baa3 / BBB- rating from Moody’s and S&P respectively. The current credit rating is one slim downgrade from being a junk bond. This one metric might give readers an idea of the slipperly-slope Boeing is trying to negotiate.

It’s also causing Boing to dilute shareholders regularly. When BA’s stock peaked in March, 2019, the fully-diluted shares outstanding were roughly 565k. Today those same fully diluted shares are 757k or 33% dilution in the last 6 years.

Not pretty.

Summary / conclusion: On January 13th, 2026, BA reported 1,175 orders for airplanes in 2025, beating out the AirBus 1,000 gross sales reported, beating the European consortium for the first time since 2018, (per the SeekingAlpha news service), and reporting 174 orders in the month of December ’25 as well as 63 deliveries in the last month of the year.

To be frank with readers, while all the good news around orders is a good sign, it still doesn’t explain why the EPS and revenue revisions remain negative, with revenue revisions mildly negative, and EPS revisions demonstrably negative. This pattern – you would think – would have to reverse.

Yes, the FAA is likely applying extreme pressure on BA to make sure they get the manufacturing right, particularly as it ramps with all the new orders, to insure higher volume doesn’t mean sacrificing quality, and that airplane doors aren’t flying off in mid-air again.

From a portfolio construction standpoint, it’s hard not to own BA since the relative performance of BA (compared to the SP 500) since January 1, ’20 shows BA with an annual return of -4.41% versus the SP 500’s +14.47%.

It’s not a stretch to call BA “non-correlated” to the SP 500 or Nasdaq at this point.

The other aforementioned positive is the support of the Trump Administration for the beleaguered airline manufacturer and defense company (BDS). Boeing defense and the global services & support (GSS) divisions now comprise more revenue (52%) than the commercial airline segment (48%) but aren’t nearly as profitable when the commercial airline division “scales”.

With the President’s announcement of the “golden dome” and a $1.5 trillion defense bill in the next two years, BA could still win big, seeing growth in BDS and GSS as well.

One final note, and it’s more of a shoutout to McAlinden Research, who appropriately flagged BA as a short in the 2019, and stayed resolutely short on the stock when it was trading in the $400’s. McAlinden is still sour on Boeing, but I think there is now the potential for a number of tailwinds for the stock and the company if Boeing can maintain quality in the face of increasing production volume. It was a great call by McAlinden and they tried to get me to short the stock, but as a long-only advisor, no stock or sector is ever shorted. I thought it appropriate to give them props since they shared their research with me, but it was never acted upon.

BA is a 2% position within client accounts, with the hope to get own more for clients.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results.