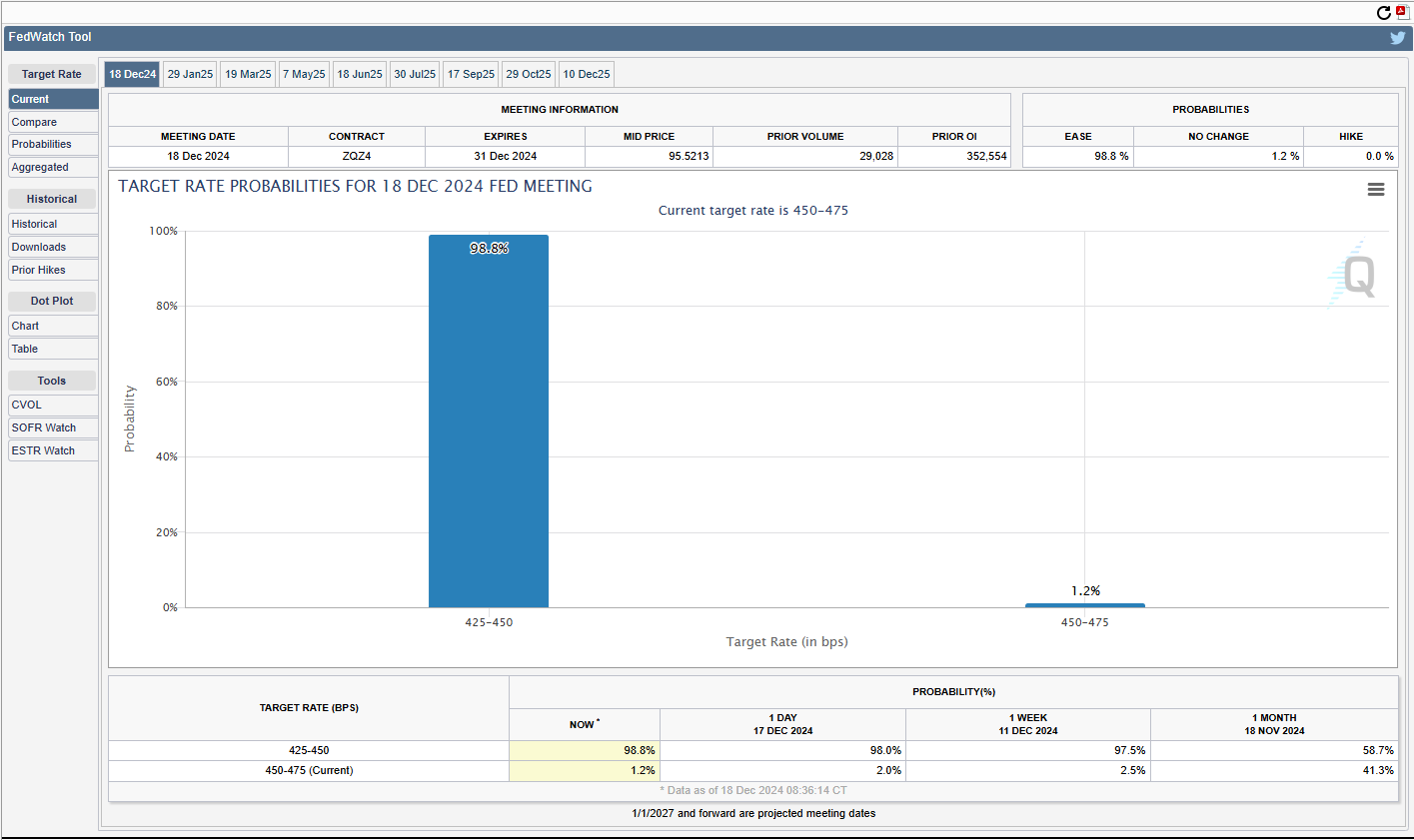

The last FOMC announcement of 2024 is coming in a few hours. Here’s what the current fed funds futures market at the CME is expecting:

There is a 98.8% probability that the FOMC announcement today will result in a new fed funds rate of between 4.25% and 4.50%.

This implies a mid-point for the new fed funds rate of 4.375% after the FOMC release today.

Here’s what the yield curve looks like right now assuming 25 bp’s lower fed funds:

- Fed funds: 4.375%

- 2-year Tsy: 4.21%

- 10-year Tsy: 4.40%

While the Fed would love to see a steeper yield curve (in my opinion) after the near 24-month inversion, and which for the first time in history did not result in a recession, after the FOMC release and assuming the 10-year Treasury continues to trade around 4.40%, the US Treasury yield curve will be almost perfectly flat after 1:00 pm central today. However, readers should assume there will be some volatility around the longer end of the Treasury curve, based on the FOMC statement. It seems like Wall Street is looking for a “hawkish pause” tenor to the Fed statement from Jay Powell, saying he’s worried about the uptick in inflation, etc.

It’s also not unrealistic to expect the fed funds rate to be below 4% by June 30 ’25. (The wild-card around this being the Trump fiscal policy initiatives (pro-growth tax changes), and tariff / trade adjustments.)

Micron Technology’s Fiscal Q1 ’25 earnings preview:

While the Fed and FOMC are definitely the “macro” lever to US monetary policy, after the closing bell tonight, and after all the weeping and gnashing over the new fed funds rate and the change in the Fed statement, Micron Technology (MU), an important semiconductor company, that is in the process of manufacturing a HBM3E chip to capture more of power required of AI computing, will report their fiscal Q1 ’25 financial results.

The sell-side analyst community is expecting $1.76 in earnings per share (vs a loss of $0.95 in EPS one year ago) on $8.72 billion in revenue, for expected year-over-year growth of nearly 300% in EPS on 85% revenue growth. Operating income is estimated at $2.3 billion versus an actual $922 ml in last year’s 11/23 quarter.

For readers, the problem or issue is that the stock (MU) typically needs to be sold when the shares look the cheapest, i.e. trading at 9X forward estimates, or low price-to-cash-flow multiples. The operating leverage inherent in this chip giant is just enormous: take a look at the history of the gross, operating and net profit margins over the last 4 years:

![]()

While part of this is the Covid inventory accumulation, and then spend-down, also attached below this is a Micron margin spreadsheet showing behavior from late 2019 back through 2014.

![]()

As someone who has followed the stock since the late 1990’s, it’s not just the stock that’s volatile, but the operating business model as well.

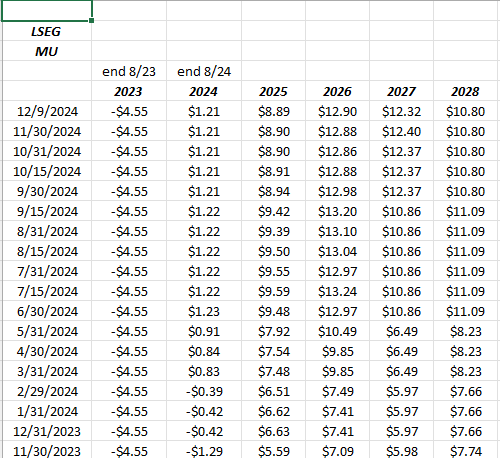

MU’s history of EPS revisions (as of 12/18/24):

Source: LSEG.com

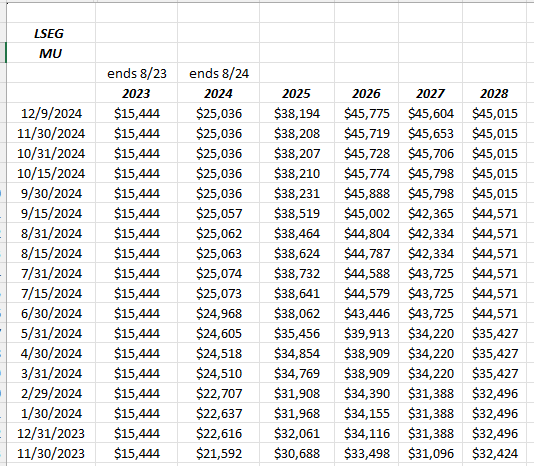

MU’s revenue revision history (as of 12/18/24):

Readers can see how the fiscal 2025 EPS estimate peaked in mid-July ’24, while the revenue estimate revisions have stayed slightly positive or firm (steady) in the last 6 months.

It looks like there is mildly downward pressure on MU’s EPS estimate for fiscal ’25 and fiscal ’26, while fiscal 2027’s revisions remain steadily positive.

Quick summary: Micron will put up strong y-o-y growth for most if not all metrics tonight, and then has another easier compare for the February ’25 quarter, and then the numbers get tougher in the back half of ’25.

The problem for me is what represents “normalized EPS” for MU, and thus given it’s inherent business model volatility the remarkable changes in EPS and revenue growth from year-to-year.

Morningstar had an intrinsic value estimate for MU as of 2019 of $40 per share, which jumped to $90 by November ’21, and which sits at $110 today. Respective, “free-cash-flow per share” (trailing twelve months) for MU as of those respective dates was roughly $5 per share, $4 per share and as of today (last quarter or August ’24 q4), is $1.07.

Micron is still trading well below it’s late June ’24 peak of $150, and is poised to trade above it’s 200-day moving average today, December 18th. Clients hold no positions coming into the release, but if semi’s were to be played for any client, i.e. the MU, NVDA, SMH, trade, the SMH would be used.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. None of this information my be updated, but if it is updated, may not be done so in a timely fashion. Investing can and does involve the loss of principal, even for short periods of time. All Micron EPS and revenue estimates are sourced from LSEG.com.

Thanks for reading.