1.) Looking at the sector weights in SP 500 market cap terms as of Friday night, 11/1/24, technology is 32% of the SP 500, while the financial sectors is 13% of the SP 500’s market cap. To take it another step further, health care is 11% of the SP 500’s market cap and consumer discretionary is 10% (mainly Amazon and Tesla). The point being 45% of the SP 500’s current market cap is two sectors and 66% is 4 sectors.

Financials get bid up during secular bull markets for good reason: the economy is usually in good shape, the capital markets are thriving and have ample liquidity.

It’s not just “tech” that represents concentration risk.

2.) Credit spreads are nearing “all-time tights” again, close to 2005 levels per Kathy Jones of Charles Schwab. An article was read this past week about the JNK (corporate high-yield bond ETF) and the HYG (corporate high-yield bond ETF) starting to decline in price, but the author didn’t really do much homework before the article was written. The high-yield bond ETF’s like HYG and JNK, have a 3% – 4% duration bogey, which means they will still have some sensitivity to moves in the equivalent-maturity Treasury, hence even high-yield ETF’s can be sensitive to yield curve changes. Credit spreads actually tightened further last week, per the Bespoke data, and with an economy that grew at 2.8% in the Q3 ’24 (per GDP last week) it makes sense spreads behaved that way.

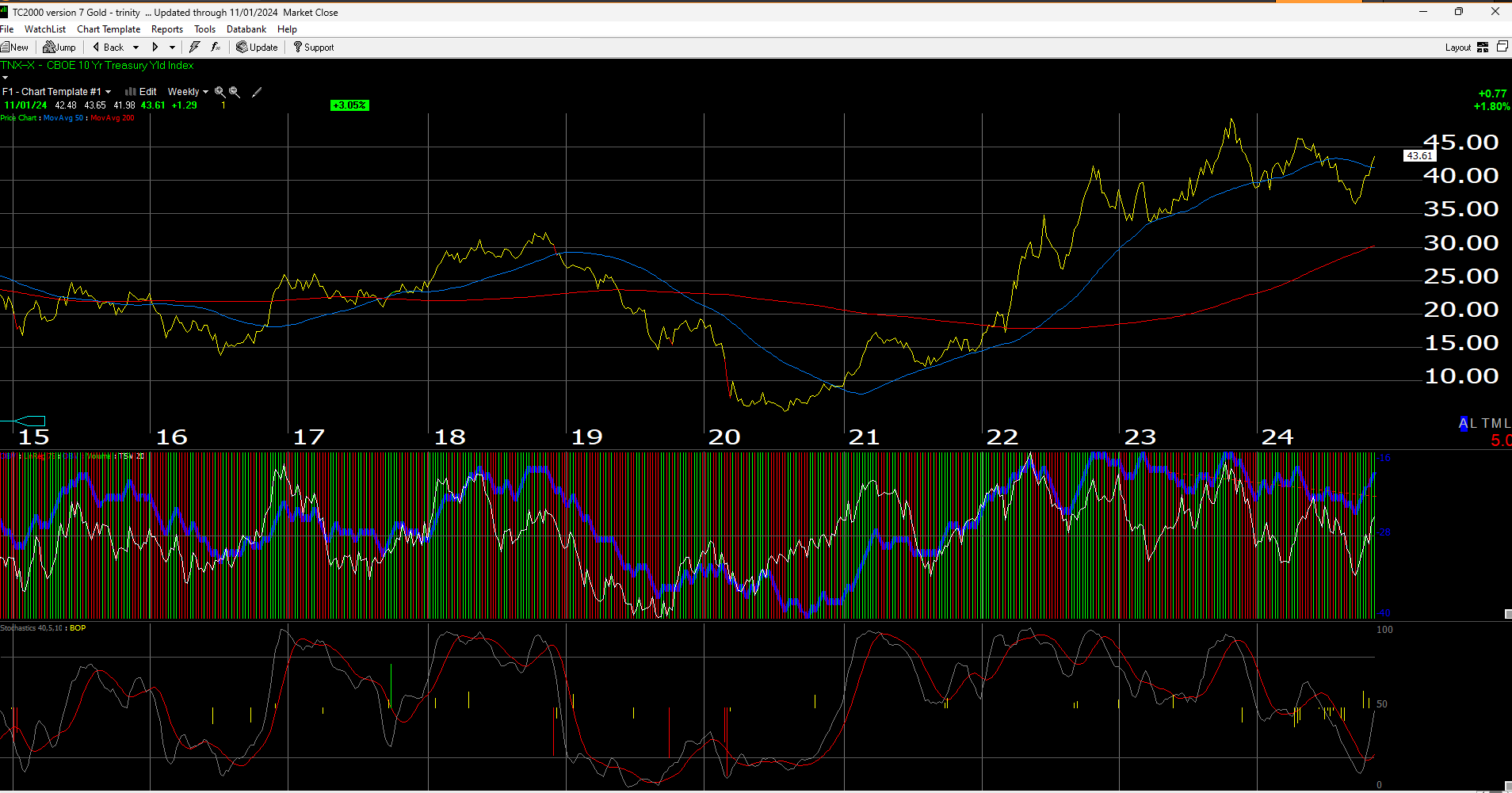

3.) Treasuries – particularly the TLT and the 10-year Treasury “yield” contract (traded at the CBOE), are on the verge of breaking substantial support.

The above chart is cut-and-pasted from @GarySMorrow over at X. I’ve know Gary for years and he’s an excellent technician. He posted this chart this past week and sent a copy.

This chart of the CBOE 10-year Treasury “yield” index was cut-and-pasted from Worden.

The 10-year yield reaction to the weak October ’24 jobs report was not really a good sign.

The ultimate breakout though for the TNX will be a heavy-volume close above the April ’24 high yield tick of 4.75%.

The yield high for this 10-year Treasury move off the 2000 lows is 4.99% struck in October ’23 though. That’s ultimately the break-out point. Stan Druckenmiller, CNBC’s Rick Santelli (and Rick is a very good bond market technician and prognosticator), and a few other notable big-name investors that the mainstream financial media love to quote frequently, are looking for – potentially – 7% on the 10-year Treasury yield thanks to the budget deficit, and a host of other reasons, that would push yields higher.

4.) These “tech” charts don’t look good:

Cut-and-pasted from Trendspider, this chart isn’t comforting.

Cut-and-pasted from Trendspider, this chart isn’t comforting.

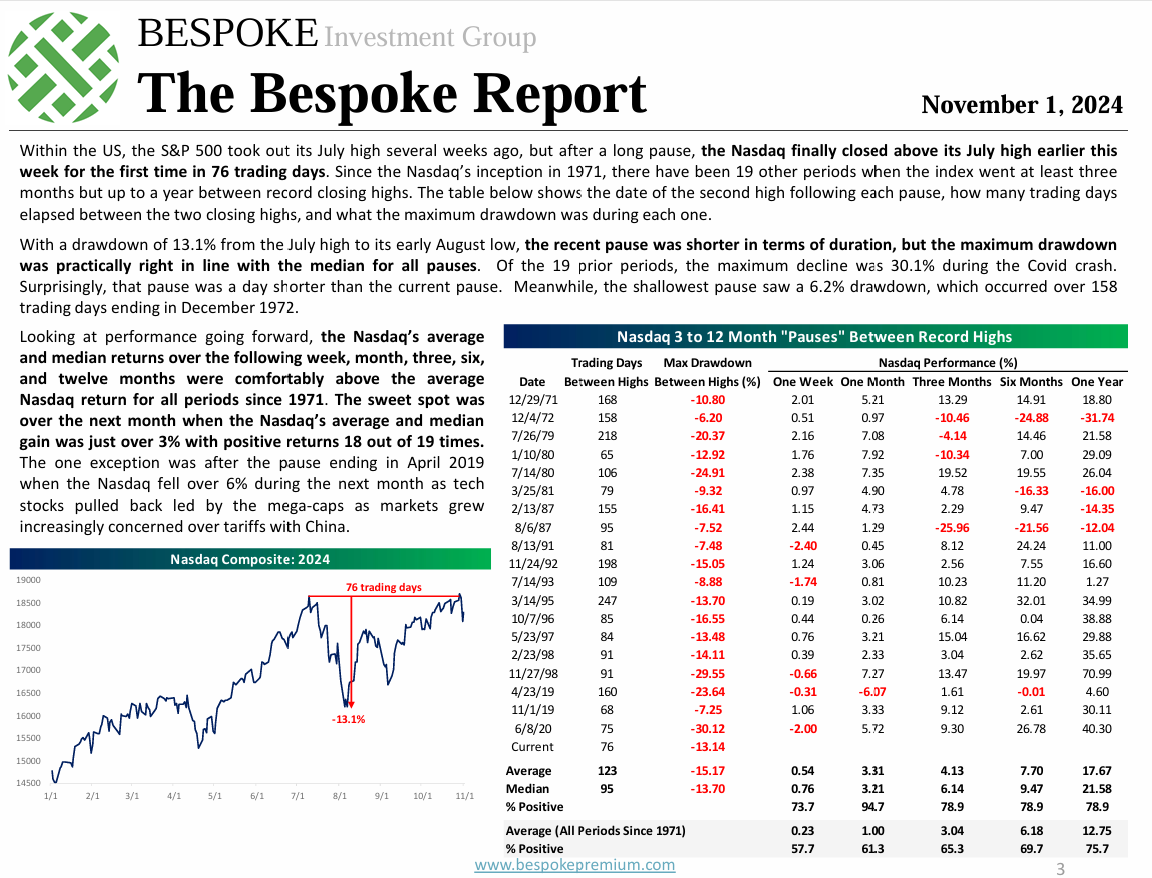

The above chart is the weekly gratuitous plug of support for Bespoke’s great work, with that chart in the lower, left-hand corner, being another technical trouble-spot.

Bespoke notes (read the columns surrounding the chart) that “expected, forward returns” for the Nasdaq after such a drawdown are positive, but both Microsoft and Apple this past week, had rather “meh” quarterly earnings reports.

The antidote to all of the above is that with November 1 passing, we are set to enter one of the seasonally-strongest periods of the year for the SP 500 and the Nasdaq, between 11/1 and 5/1. November and December are two of the strongest months of the year speaking in historical monthly returns.

None of this is a recommendation, or advice, but on reflection, simply an opinion. Past performance is no guarantee for future results. Investing can and does involve the loss of principal even for short periods of time. Opinions offered on this blog can change quickly, and may or may not be updated, and if updated, may not be done in a timely fashion.

Thanks for reading.