When IBM reported their Q3 ’24 financial results, the night of October 23rd, ’24, the stock has had a nice run into the earnings release, trading above it’s previous, April 2013, all-time-high of $213 – $215 per share. Now with the pullback since the Q3 ’24 earnings update, the stock is still being bought in small quantities, as the stock is already oversold, now trading between the April, 2013, all-time-high of $213 – $215, but above the April – May, 2024 highs of $198 – $199.

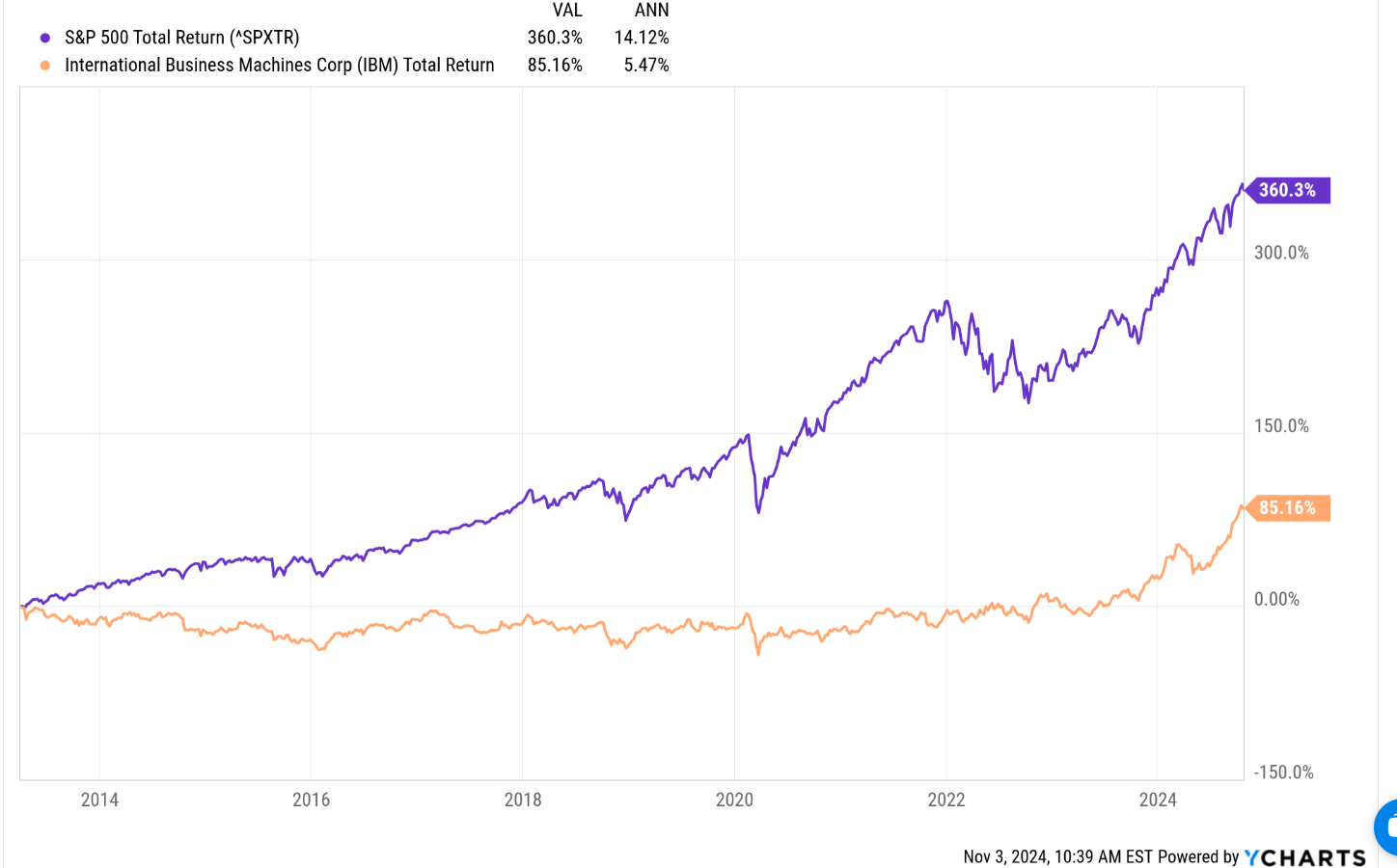

Here’s a quick chart showing IBM’s total return vs the SP 500 since IBM peaked in April, 2013:

From a “portfolio construction” standpoint” this return analysis is important, but we’ll get into it, further down the earnings review.

Let’s start with the bad news:

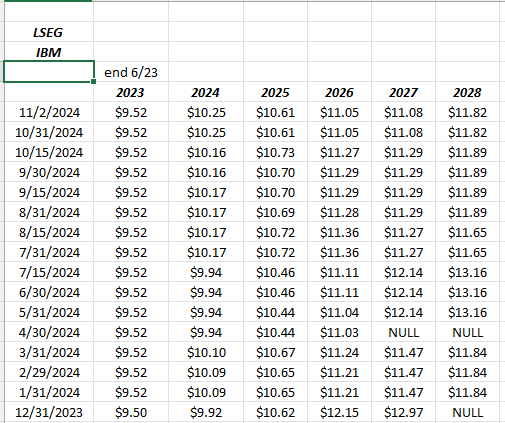

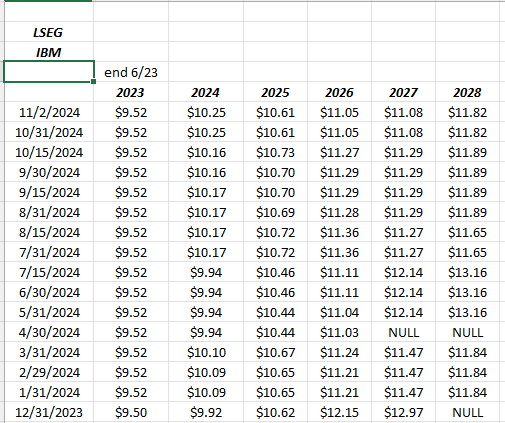

IBM EPS estimate revisions:

While IBM’s 2024 EPS estimates were revised higher after the 10/23 earnings report, the negative revisions for 2025 and 2026 were not good to see. IBM’s software unit had solid results for Q3 ’24, with revenue +9.5% in the quarter, and IBM’s guidance for software revenue for the Q4 ’24 quarter was also positive, but the consulting unit’s drag on Q3 ’24’s results sounds like the unit’s issues will continue into Q4 ’24 and into 2025.

In Q3 ’24, consulting, infrastructure and the other IBM segments all saw negative y-o-y revenue growth.

IBM reiterated that they continue to transition the business into higher-growth, higher-margin businesses, like software, and AI, but a lot of businesses say that, while execution is much tougher.

What was encouraging on the call was that the AI “book” since inception now stands at $3 billion, up from $2 billion at the end of the 2nd quarter ’24, but that’s cumulative $3 billion book on an expected total revenue estimate for 2024 of $62 billion.

In other words, it’s a start, but investors are looking for better.

IBM EPS estimate revisions:

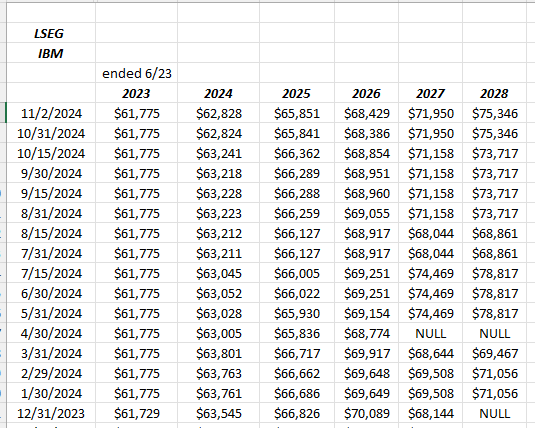

IBM revenue estimate revisions:

While IBM’s forward estimate revisions are seeing mild downward pressure, it’s nothing like the drop in EPS estimates after earnings were released.

Usually when you get a dynamic such as this (sharper revision in forward EPS estimates, than revenue estimates), it’s usually because analysts are expecting a margin issue.

IBM “Light”: Capex continues to shrink:

Here’s the history of IBM’s capex the last 12 – 13 years:

- 2024 YTD: $459 ml YTD

- 2023: $1.245 bl

- 2022: $1.35 bl

- 2021: $2.01 bl

- 2020: $2.6 bl

- 2019: $2.3 bl

- 2018: $3.4 bl

- 2017: $3.2 bl

- 2016: $3.56 bl

- 2015: $3.57 bl

- 2014: $3.74 bl

- 2013: $3.62 bl

- 2012: $4.0 bl

- Source: IBM annual report(s)

It’s not rocket science to say that IBM has gradually pulled back on capex over the last 12 years.

The calendar Q4 every year is typically IBM’s strongest quarter every year, so expect a bump in the full-year 2024 capex.

Valuation:

At $206 per share, IBM is trading at 20x and 19x expected EPS growth in 2024 and 2025 of 7% and 4% respectively.

IBM’s price-to-revenue is a little over 3x, while price-to-cash-flow and price-to-free-cash-flow is much more reasonable at 13x and 14x the trailing-twelve-month (TTM) numbers.

As was noted in IBM’s earnings preview, IBM hasn’t repurchased $2 billion in stock in any single quarter since December, 2019.

Here’s the TTM average growth in free-cash-flow for IBM:

- 4-quarter avg: $12.9 bl

- 8-quarter avg: $10.6 bl

- 12-quarter avg: $9.7 bl

- 20-quarter avg: $9.8 bl

- 40-quarter avg: $11.1 bl

While TTM EPS for IBM as of the September ’24 quarter was $10.28, the cash-flow and free-cash-flow per share were $15.29 and $14.40 respectively.

That indicates that IBM still has an acceptable quality of earnings, and the stock is cheaper than the EPS multiples imply.

Summary / conclusion:

If you’ve studied finance and economics as long as I have, and managed money as long, readers would know the dwindling capex could be a double-edged sword: it could mean that Arvind Krishna and the Board are not finding businesses with a sufficient return-on-invested-capital to either or build or buy at IBM, or Arvind is letting the old data management business run off, that Sam Palmisano left for Ginny Rometty to die a slow business death under, while IBM tries to target new opportunities for growth.

The AI book is encouraging, but it’s still just 5% of revenue, and that’s since “inception” so investors would sure like to see IBM develop that further.

The growth in free-cash-flow is encouraging, but the lack of a share buyback program – in fact IBM is mildly diluting shareholders since fully-diluted share count has grown from 904 million shares in June ’21 to 924 million shares as of September, ’24 – is frustrating, and I do think could be a forward catalyst for the stock. IBM took on $18 billion in long-term debt to acquire RedHat in June ’19, and while some of the debt has been paid down, IBM still has $52 billion of the Sept ’24 quarter. (The point being maybe the debt load is keeping IBM holding onto cash for now.)

It’s tough for the Board and Arvind to turn a pure hardware business into a software business, but that’s what looks to be happening. Software today is 44% of IBM’s total revenue.

In terms of holding IBM in client accounts, part of the recent interest is that IBM is “old tech” and as the above Ychart shows, the stock has dramatically underperformed the SP 500, and thus if the mega-cap 7 or mega-cap 10 or large-cap growth or momentum, or whatever name you wish to assign to the SP 500’s leadership the last 10 years starts to fade, or even correct sharply, IBM remains “uncorrelated” to the tech momentum crowd. (While they don’t report for a couple of weeks, but Cisco is starting to show better relative strength. Old tech is starting to find some traction.)

IBM is now trading between the first quarter ’24 highs of $198 – $199, and the 2013 all-time-high of $213 – $215 per share. More shares will be accumulated within this range, as long as IBM doesn’t fall too far below $198 – $199.

IBM reinvented itself in the late 1990’s buy buying Lotus 1-2-3, under Lou Gerstner, after Big Iron lost a lot of ground to the PC and server in the late 1980’s and early 1990’s. Under Sam Palmisano, IBM found good business in data management using the old mainframe business (as I understood it). Since then, IBM has struggled, but perhaps AI is big enough to allow for the smaller, niche players to operate and earn sufficient returns.

The technical breakout in the stock above that former April ’13 all-time-high is what got my attention.

IBM, Arvind Krishna and the management team now need to follow through with revenue and EPS growth.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal, even for short periods of time. This information may or may not be updated and if updated may not be done in a timely fashion. All revenue and EPS estimates are typically sourced from LSEG, unless otherwise noted.

Thanks for reading.