2019 was the last year investors saw what could be called “normal” easing cycle driven by macroeconomic growth concerns and falling SP 500 EPS estimates.

That was the third year of President Trump’s term and obviously just before the pandemic, which wound up having an enormous influence over monetary and fiscal policy.

To give readers the backdrop, 2018 was year when the Fed was still tightening monetary policy and trying to get the fed funds rate off zero percent, as it remained from late 2008 through Q4, 2016. Janet Yellen started raising the fed funds rate in Q4 ’16 shortly after President Trump was elected, and then President Trump replaced Yellen with Jay Powell, but Powell continued the restrictive monetary policy as US GDP growth remained healthy and the US economy was in decent shape. (My impression back then was that Powell wanted to get the fed funds rate back to 3%, to give the FOMC some latitude for future monetary policy changes, but I believe the 2018 peak for the fed funds rate was ultimately 2.75%, before it was reduced in 2019.

The interesting aspect to late 2018 was the correction in the SP 500 in Q4 ’18: the last 90 days of 2018, the SP 500 fell -13.5%, but if we end the performance calculation on Christmas Eve or December 24 ’18, when the market closed that night, the SP 500 was actually down -18.90%.

That was a sharp SP 500 correction and it caught a lot of people off guard.

On December 26th, the SP 500 opened lower again and then reversed higher to close the day +4%, and that was thought to be the moment where the equity market sniffed out Jay Powell’s sentiment turn from “higher-for-longer” to it’s time for a mid-cycle correction. I don’t recall whether Powell gave a speech on December 26th, or it was just the SP 500 being the discount mechanism it is, and figuring out that the Fed was about to turn “easier”.

If you look back at the FOMC releases in 2019, Jay Powell termed the lowering of the fed funds rate as a mid-term cycle correction, and that could be what we are faced with today, in 2024.

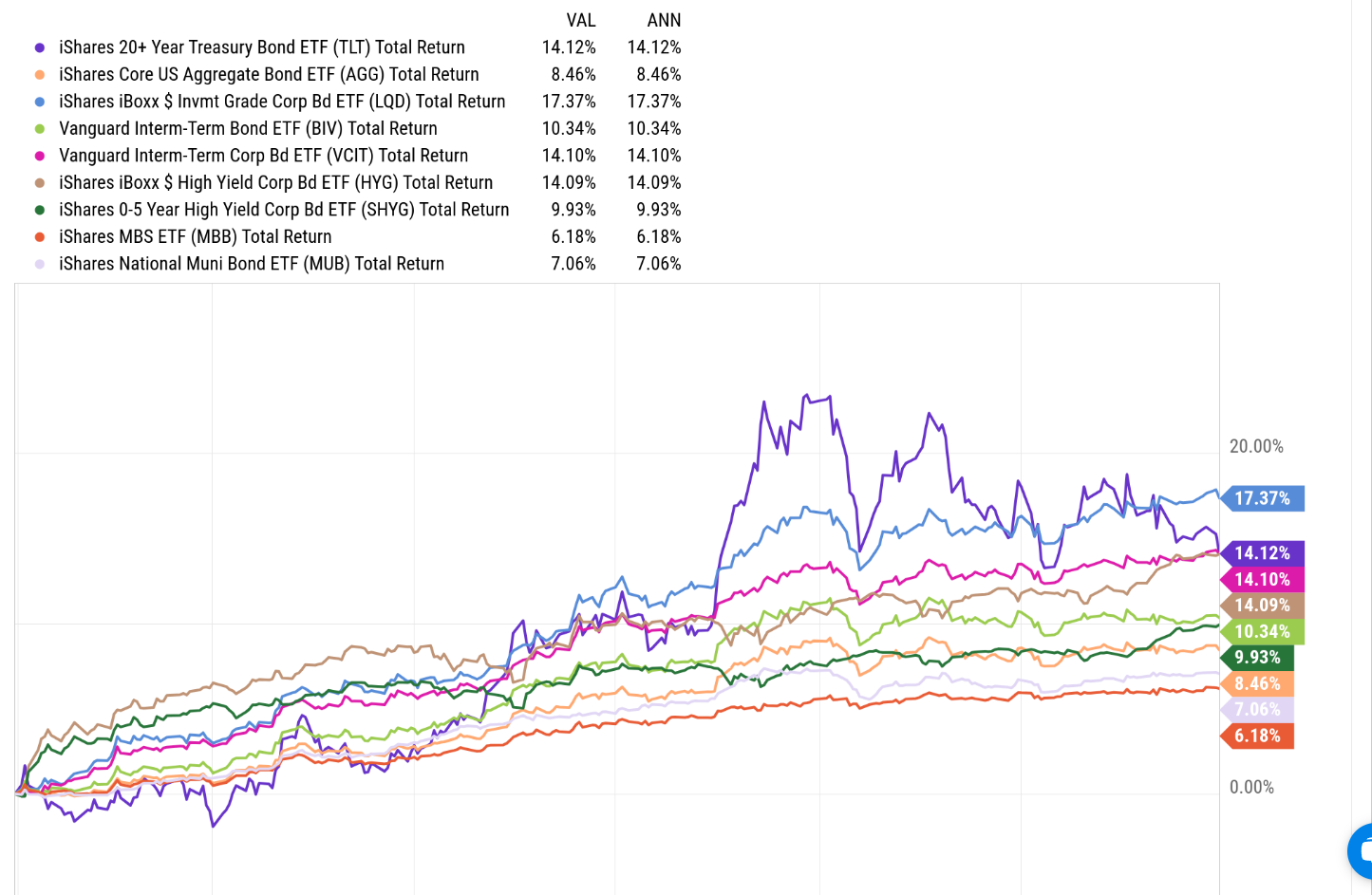

Using ETF’s, here’s how the various bond asset classes performed in 2019:

- The BBB-centric LQD ETF returned +17.37%;

- The TLT or the 20-year Treasury ETF returned +14.12%;

- Vanguard’s Intermediate-bond ETF’s (VCIT) returned +14.10%;

- The High-yield Bond ETF (HYG) returned +14.09%;

- The Vanguard Intermediate Bond ETF returned +10.34%;

- The 0-5 year High yield ETF (SHYG) returned +9.93%;

- The iShares Barclays Aggregate (AGG) returned +8.46%;

- Muni’s (MUB) and mortgages (MBB) underperformed the Aggregate, returning 7.06% and 6.18% respectively.

The economic backdrop was different then, than today. Back in 2019 – 11 years after the 2008 crisis – inflation was still below 2% at 1.5%. The IMF thought there was a “global synchronized slowdown occurring” in early 2019, per the statements from that time.

Corporate America – particularly their balance sheets – were undoubtedly in great shape, thanks to zero interested rates for 8 years, and maybe that’s why US corporate bonds and in particular high-yield bonds performed so well in 2019.

Frankly, you could make the same case today. Credit spreads haven’t widened much with the recent equity market volatility, as was written about last weekend here.

Also interesting is that while the “forward 4-quarter estimate” for the SP 500 started to roll over in Q4 ’18, it ended the quarter about where it started. here’s a quick rundown of the history of the forward 4-quarter EPS through Q4 ’18:

- 8/31/18: $169.12

- 9/28/18: $168.72

- 10/26/18: $173.24

- 11/30/18: $171.01

- 12/28/18: $168.95

By the end of June, 2019 the forward 4-quarter estimate was $170.74, so it’s clear by the numbers that SP 500 earnings growth had stalled as we moved into 2019 from 2018.

What surprised me in looking back at 2019, the FOMC didn’t reduce the fed funds rate until the July ’19 meeting when it cut 25 bp’s and then it cut 25 bp’s again in September and October ’19 as well.

Summary / conclusion:

“Past is prologue.”

We’ve all heard that Shakespearean expression.

History repeats but readers and investors want to know how it will repeat and of course we don’t know that exactly.

Credit spreads and the sequential increase in the SP 500’s “forward 4-quarter” estimate and the improvement in “rates-of-change” certainly seem to bode well for the SP 500, but 3rd quarter results will matter.

The reversal in the SP 500 today is reminiscent and almost exactly patterned the December 26, ’18 reversal, although the SPY today only finished up 1% versus the SP 500’s return on 12/26/18 of +4%.

For us fundamental investors, Oracle’s earnings report led Morningstar to conclude that “demand continues to exceed supply” in Oracle’s Cloud Infrastructure (OCI) segment, now Oracle’s largest division. It’s been remarkable how quickly Oracle has gained share in the AI segment, and is now considered on par with Microsoft, Amazon and Google.

Nvidia and Jensen Huang’s comments today also seemed to help the market rally.

None of this is a recommendation or advice, but only an opinion. Past performance is no guarantee of future results. Investing can and often does involve loss of principal even for short periods of time.

Hope the 2019 returns among the bond asset classes gave readers food for thought.

Thanks for reading.