Promised readers in this weekend’s SP 500 earnings comments that a quick history of the “upside surprise” for SP 500 revenue and EPS would be forthcoming:

- Q1 ’23: +7.7% EPS, +1.5% revenue

- Q4 ’22: +1% EPS, +1.6% revenue

- Q3 ’22: +3.4% EPS, +2.3% revenue

- Q2 ’22: +5.5% EPS, +2.5% revenue

- Q1 ’22: +7% EPS, +2.6% revenue

- Q4 ’21: +5.1% EPS, +2.7% revenue

- Q3 ’21: +10.2% EPS, +2.9% revenue

- Q2 ’21: +15.7% EPS, +5.2% revenue

- Q1 ’21: +22.3% EPS, +4.0% revenue

- Q4 ’20: +15.7% EPS, +3.7% revenue

Last weekend, this blog previewed the mega-cap companies reporting earnings last week, and the title referenced the post Covid hangover, and that’s exactly what’s happening.

Readers can see that after the gradual erosion in SP 500 EPS and revenue “upside surprises” in 2022, Q1 ’23 is breaking the trend.

Personally, I’d rather see stronger beat rates coming from revenue, but it’s clear corporate management are much more disciplined around expense management than the last 2 years.

No question, Q1 ’23 SP 500 EPS have come in much stronger-than-expected.

The various market narratives or “fears” that constantly arise in the financial media:

- Recession: the jobs market needs to crack. Corporate CEO’s have been fearing recession for 15 months now. You have to assume it will happen at some point;

- Inflation: Services inflation is turning out to be “stickier” than expected. The majority of the inflation indices have rolled over;

- The Fed and FOMC: will do another 25 bp’s this week. The question is, “When does the FOMC stop hiking fed funds ?”

- SP 500 earnings and revenue weakness: not so much, at least so far in Q1 ’23;

- Credit spread weakness: none really to speak of, certainly nothing like 2001 – 2002 or 2008. (More on this later in the blog);

- Banking “crisis”: now contained, although First Republic Bank (FRC) will be taken over. No systemic risk in evidence;

- The debt limit battle: needs to be addressed, still in front of us. Could get ugly;

- “The 60/40 portfolio is dead” per Blackrock this week. Doubtful…

Other narratives:

- Market-weight is outperforming equal-weight, the opposite of last year. The SP 500 and the QQQ are up 9% and 21% respectively, while the RSP (SP 500 equal-weight) and the QQQE are up 3% and 11% respectively.

- The 60% / 40% benchmark portfolio is up 7% YTD as of 4/28/23.

- Market breadth isn’t great – it’s a big peg in the bear case;

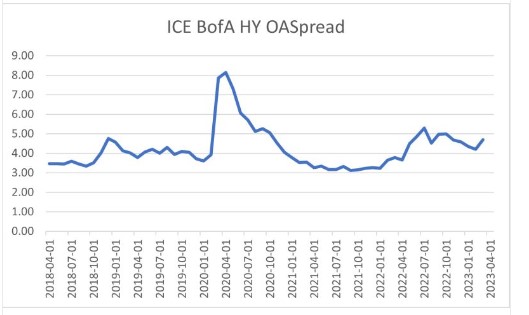

Credit Spreads Have Been a Pleasant Surprise:

Good graph cut-and-pasted from John Silvia’s column on LinkedIn.com. John was a former economist at Kemper in Chicago and Wells Fargo in the 1990’s. I knew him from his time in Chicago in the early 1990’s.

Here’s a quick run-down of YTD returns of credit-related ETF’s and mutual funds so far in 2023:

- Investment-grade corporate: +4.29% (Bloomberg source)

- iShares Investment-Grade ETF (LQD): +5.28%

- PIMCO Corporate ETF (CORP): +4.85%

- High-yield corporate: +4.60% (Bloomberg source)

- Barclays Aggregate( AGG): +3.92%

- iShares High Yield ETF (HYG): +3.94%

- iShares short-duration Hi Yld ETF (SHYG): +3.42%

- PIMCO Corporate High Yield (PHDAX): +4.59%

- Invesco Financial Pref’ed ETF (PGF): +5.10%

- iShares Pref’ed and Income Sec (PFF): +4.54%

- SPDR Bloomberg Convertible Bond (CWB): +3.13%

You heard a lot of talk by corporate bond fund managers about “upgrading credit quality” after Silicon Valley Bank collapsed, and yet most of the corporate credit ETF’s and funds are still trading at or near YTD highs. Many of these funds and asset classes, rallied sharply in January ’23, sold off in February ’23 on higher inflation worries, and then again in March ’23 with regional bank and credit constriction concerns, but have rallied back again.

The interesting vehicles to me are the LQD and PIMCO’s CORP, which are both primarily BBB-rated ETF’s, which is probably not a bad place to be on the capital stack (to borrow a Rick Rieder term), to sit between the “better economic growth ahead” and “it’s going to be an ugly recession” dynamic.

There is no question that corporate credit and corporate high yield spreads have held up much better over the last 16 months than many anticipated in early 2022. I’d get nervous about corporate high-yield if the monthly jobs report started losing 200,000 – 300,000 jobs per month. That would be the first sign of potentially-deeper credit trouble.

FOMC meeting May 3rd, 2023:

According to CME’s FedWatch tool, there is an 84% chance of the FOMC raising the fed funds rate to 5% – 5.25% Wednesday evening May 3rd. The future rate hikes look somewhat less “robust” right now, but that will change based on Jay Powell’s press release and presser. The next FOMC meeting is June 14th, 2023.

Personally, the core inflation rates – particularly services inflation – are still too high. We’re still a long way from 2%.

There is no question that the majority of inflation indices have rolled over, and are headed south, but they remain above the FOMC’s desired target range, and there seems to be little reason for Jay Powell to turn “dovish”.

The only question is whether the asset – liability or “duration mismatch” within the banking system is thought to be enough of an issue at the Fed to try and return the Treasury yield curve, to it’s normal, positive slope.

Apple (AAPL) reports Thursday night, a day after the FOMC announcement.

Summary / conclusion: If readers turned off CNBC, and Bloomberg and Fox and simply watched “price action” you’d think all was well with the world. Even international markets are having a good year, and 2022’s so-called “bear market” wasn’t that bad. 2022 was simply a correction from the over-heated Covid stimulus.

Everything is up this year in terms of YTD returns, i.e. Treasuries, corporate credit, municipal credit, mortgages, even emerging market credit, not to mention large, mid and small-cap stock indices and international. Like a mirror-image of 2022, the only asset that is down in 2023, which was up in 2022, is the US dollar.

And yet sentiment is so bearish.

Maybe this week is THE week that the bottoms falls out.

None of this is advice, or a recommendation to buy or sell, and past performance is no guarantee of future results. Add SP 500 EPS and revenue data is sourced from IBES data by Refinitiv. More importantly, any information may or may not be updated in a timely fashion, if at all. Capital markets can change quickly for both the positive and negative (depending on how you are positioned.)

Thanks for reading.