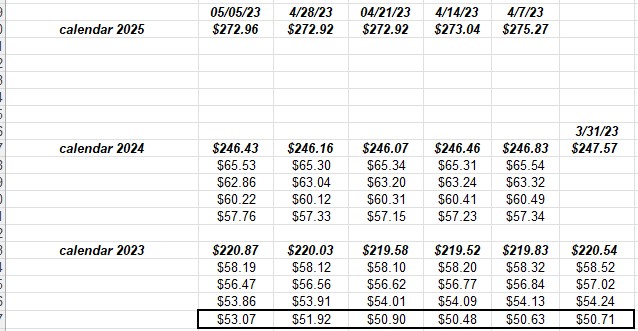

Rather than bury the lead, the blog will show the increase in the Q1 ’23 SP 500 EPS estimate since 3/31/23 i.e. the dark-bordered line in the above spreadsheet,.

That’s a big jump, and it reflects the “upside surprise” discussed two weeks ago and last week on this blog.

Readers likely only care about what’s going to happen rather than what’s happened, but looking at the pattern of future EPS estimates in the above spreadsheet, there continues to be a slight degradation in forward estimates, which is typically the case.

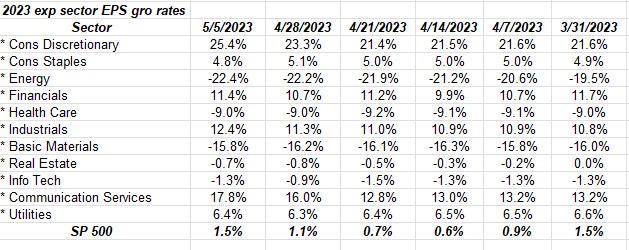

Note the improvement in “expected 2023” sector growth rates: consumer discretionary ( contains AMZN, TSLA, and homebuilders) has shown a roughly 20% increase since 3/31/23, while Communication Services (META, GOOG/GOOGL) has seen a roughly 25% increase since the start of the quarter.

Interestingly, technology is still flat since 3/31/23 and was +3.5% as of the start of the year. Because Refinitiv cuts off the data as of Thursday night every week, technology estimates may not contain the full Apple EPS and revenue revisions, until early this coming week.

SP 500 data:

- The forward 4-quarter estimate increased to $226.28 from last week’s $225.91. The forward estimate of $226.28 compares to $220.49 as of 3/31/23, and $222.91 as of 12/31/23.

- The P/E ratio on ’23 is 18.7x and now on ’24 16.8x;

- The SP 500 earnings yield as of this week is 5.47% vs 5.37% on 3/31 and 5.81% on 12/31/22.

Summary / conclusion: The “upside surprise” or so called beat rates for the SP 500 EPS and revenue could be a function of the dire recession that has been predicted for 15 – 16 months, that hasn’t materialized, therefore margins are better even though SP 500 revenue growth at +3.5% is just slightly better than the +2.5% average for SP 500 revenue growth, pre-Covid.

There could a lot of reasons for the EPS upside, not the least of which is still a US economy that continues to grow nicely despite considerably tighter monetary policy in the last 16 months.

Comparing the sentiment coming into the Q1 ’23 earnings reporting season to the actual results, analysts were really cowed coming into the latest earnings season.

I’m watching Walmart this week. EPS is expected to be flat year-over-year. Their comments on grocery inflation will be quite important. Expect inventory growth to be lower than revenue growth again for this quarter ended April ’23, another sign Walmart is moving beyond the inventory backup that hit them hard in calendar ’22.

Take all the opinions rendered here with considerable skepticism and a healthy grain of salt. Past performance is no guarantee of future results, and any information enclosed herein may or may not be updated in a timely fashion. All earnings data is sourced from Refinitiv and IBES data from Refnitiv. Capital markets can change quickly for both the good and bad: assess your own appetite for market volatility.

Thanks for reading.