As an aside, the 10-year Treasury yield jumped late Friday, January 16th, and ended up closing above the 4.20% yield level for the first time in several months. Didn’t see any specific news on why the yield jumped like that, but the equity indices also faded more than expected late Friday.

This sector returns post from Morningstar on Saturday, January 17th, shows the start of what could be the long-awaited “rotation” for stocks.

Note where the tech sector ranked as of the first two weeks of 2026. This blog post from this weekend talks about how the tech sector growth rates are still rising and 2025’s expected tech sector EPS growth of 25% (as of this weekend), is still expected to be exceeded by 2027’s +31% EPS growth.

Maybe some or a lot of that growth is coming from semi’s: check this table from WallStEngine last Friday afternoon:

Those are the respective stock returns, but I’ll bet the expected EPS growth is supportive of those returns.

Remember, too, in cycles like the late 1990’s and AI today, the semiconductor sector can generate extraordinary return-on-invested-capital (ROIC) returns, and then generate losses after the cycle has peaked. This blog learned it’s lesson on Micron Technology (MU) in the late 1990’s, early 2000’s. This sector can destroy capital – like an airline – for long periods of time.

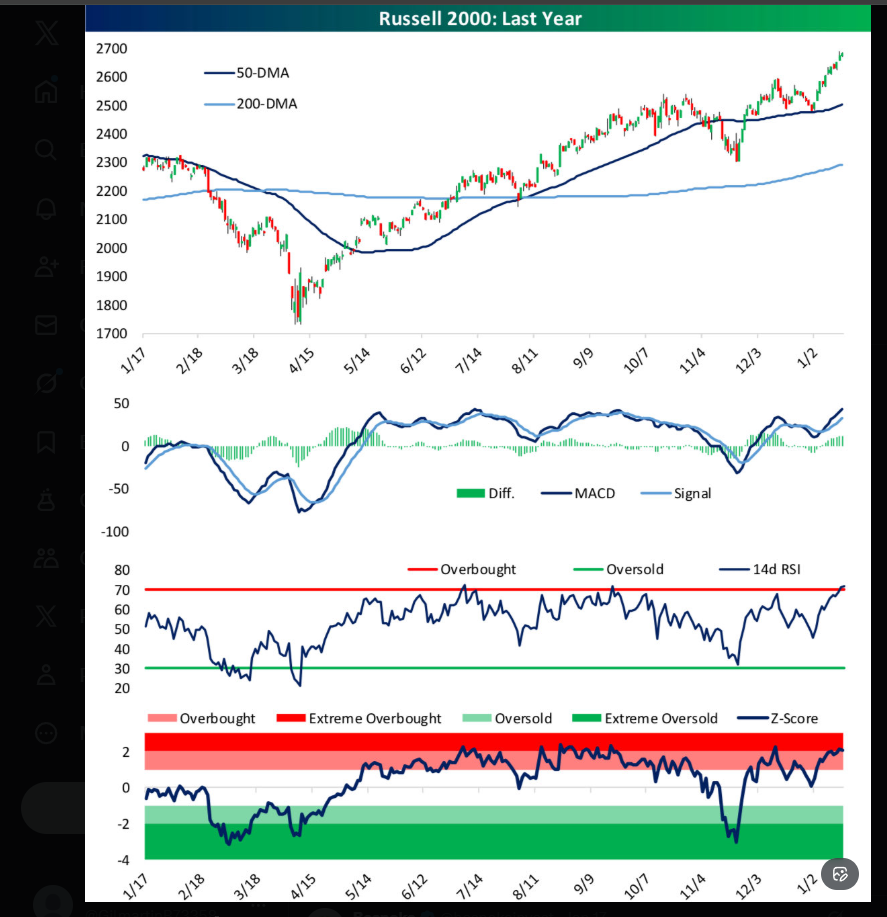

This chart from Bespoke last week shows the breakout in the Russell 2000 (IWM) which started in late ’25. It’s already overbought in early ’26.

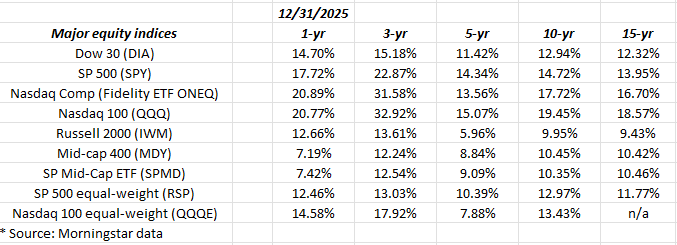

One last table: equity indices annual returns as of 12/31/25:

This spreadsheet gets posted occasionally showing annual returns for the US equity asset classes. Note the 5,10, and 15 year returns for the Russell 2000, the mid-cap 400, the SP 500 equal-weight, and the Nasdaq equal-weight, versus the SP 500 and Nasdaq 5, 10 and 15-year returns.

Summary / conclusion:

If AI stocks like the Mag-10 put up solid numbers for Q4 ’25 and then guide strongly for 2026, the rotation into some of these long-dormant sectors could be stalled. Investors follow returns, at least many retail investors, while many professional investors look for “non-correlated” and “value” sectors until the growth infatuation stops.

Mid-March, 2000, was a seminal moment: with the SP 500 and the Nasdaq making all-time-highs, the music stopped and the indices didn’t make new all-time highs for 13 years (the SP 500) and 16 – 17 years for the Nasdaq.

That’s the issue with riding the longer-term secular bull market: you don’t know how long it will take the market to recover former highs, i.e. 3 years, 5 years, 10 years ?

Tech earnings start at the end of the month of January. Guidance will matter the most, relative to current expectations. Will be out with previews for readers.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results.

Thanks for reading.

The JGB made a six-sigma move.

thanks. good info.