With the markets closed Monday, January 19th, it will provide an extra day to prepare for the onslaught of Q4 ’25 earnings over the next two weeks.

A break was taken the last 4 weeks from writing about SP 500 earnings, since there appeared to be a glitch in the LSDEG I/B/E/S data starting in mid-December ’25.

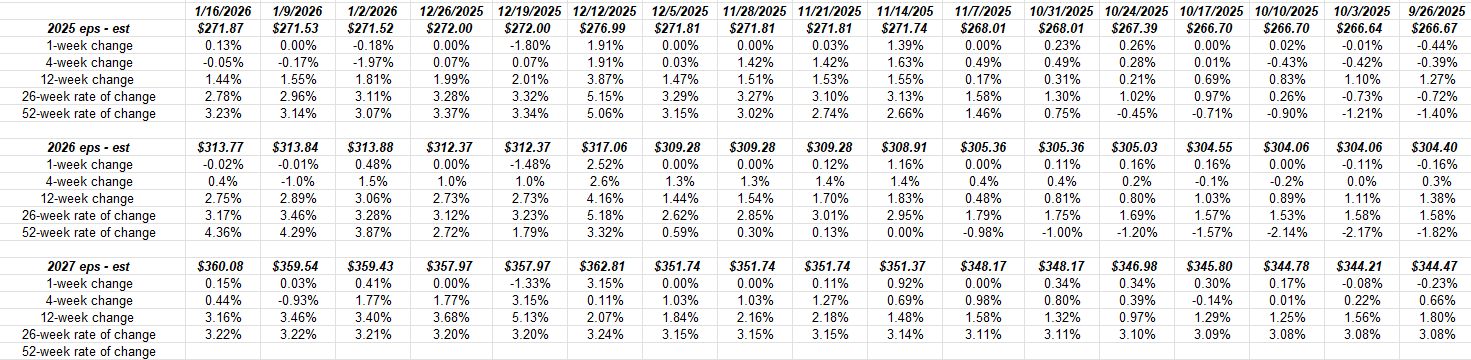

Here’s how the calendar 2025, 2026, and 2027 have progressed since late September ’25:

Readers should expand the spreadsheet and note the increase in calendar EPS estimates from 12/5/25 to 12/12/25 and then back down again the following week of 12/19/25.

IBES acknowledged the issue and looks to have resolved it.

Tech sector expected growth rates:

A couple of points to make about the expected 2025 and 2026 sector growth rates noted in the spreadsheet immediately above:

1.) Note how the SP 500’s expected growth rate for 2025 (top half of spreadsheet) has risen from +20.9% on October 17th, to a now-expected +25.4% as of January 16, 2026. That’s a sharp increase in one quarter’s time, but TMC’s results this week, support that increase. Note how the expected 2026 tech sector growth rate is much more subdued, which is more normal, but is still higher than 2025’s expected growth rate.

2.) Note how the expected technology sector growth rate is looking for even faster growth in 2026. As of this weekend, the tech sector is expected to growth +25.4% in full-year 2025, which will essentially be concluded by mid-February ’26, while the tech sector for 2026, is expected to grow at a +31.1% rate for full-year 2026.

While COVID distorted tech sector growth rates this decade, and AI is the primary driver of tech sector growth since 2023, here again are average EPS growth rates for the tech sector over the last 15 years:

- From Q1 ’23 to Q3 ’25: +18%

- From Q4 ’22 back to Q1 ’20: +19%

- From Q4 ’19 back to Q4 ’11: +10%

It’s not rocket science that as AI filters through the tech sector sub-sectors, well above-average growth is now being seen.

Summary / conclusion:

Of the 3 largest names in the SP 500 by market cap, two of the three, Apple (AAPL) and Microsoft (MSFT) report the last week of January ’26, with Microsoft reporting January 28th, and Apple reporting January 29th, so we still have a few weeks before hearing from the MAG-10 from an earnings perspective. The two other names, Nvidia (NVDA) and Broadcom (AVGO), report the last week of February ’26.

The re-classification of the SP 500 a few years has moved what many less-informed investors consider “tech stocks”, into areas like Consumer Discretionary, i.e. Amazon (AMZN), and Tesla (TSLA), and Communication Services, i.e. Alphabet (GOOGL), and META (META).

Oakmark, the great value shop here in Chicago, has Bill Nygren as it’s highest profile US value manager leading the Oakmark Fund (OAKMX), and Bill noted on a conference call a few months ago that if the SP 500 had not re-classified Amazon, Alphabet and probably Tesla into other sectors of the SP 500, that the technology sector’s market cap weighting in the SP 500 today, would be closer to 55% than today’s 33.7%.

The top 3 stocks in the SP 500 today – Nvidia, Apple and Microsoft – are just shy of 20% (19.77%) of the SP 500’s total market cap as of Friday, January 16th, 2026.

The concentration risk is well known, but I have to keep writing about to continue to remember to trim winners with the heavier weights and re-allocate proceeds into long-dormant sectors and asset classes that have been out of favor for years.

2026 is starting out well, but tech and the large-cap growth crowd might not convincingly break out until we see what Mag 10 earnings report and more importantly guide. No question fund flows are seeking out areas like international and emerging markets, and technically the Russell 2000 (IWM) broke out above the key $250 technical level.

There is a general broadening of market returns, which is always a plus for diversified portfolios.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. All SP 500 earnings data is sourced from LSEG I/B/E/S. Remember, readers should gauge your own comfort with portfolio volatility and act accordingly. None of the information on this blog post may be updated, and if updated, may not be done on a timely basis.

Thanks for reading.