- SP 500 YTD decline: -12.99%

- Barclay’s Agg YTD decline: -9.43%

- 60/40 portfolio YTD decline: -11.57%

At the FOMC meeting this Wednesday, May 4th, the only debate seems to be whether it’s “50 bp’s and a heavy done of QT” or just 50 bp’s, and then you’d have to wonder whether Jay Powell keeps his foot on the hawkish brake by talking tough after the meeting or, if he sounds a little more conciliatory.

With the 2-year Treasury yield at 2.70% as of Friday’s close, and 1-year Treasury at 2.10%, the short end of the Treasury yield curve has already incorporated a lot of tightening by the FOMC.

Although I hate to quote the fat man, several weeks ago Josh Brown made the exact right point that the more Powell and Bullard and the Fed can accomplish with “jawboning” or as my old Money & Banking text used to call it, “moral suasion”, the less “open market operations” might eventually be required.

My own opinion is that the “inflation” story is completely distorted by the financial media. CNBC has become the financial equivalent of “The View” and most of that crew wouldn’t know the difference between a fixed-weight inflation index, or a deflator.

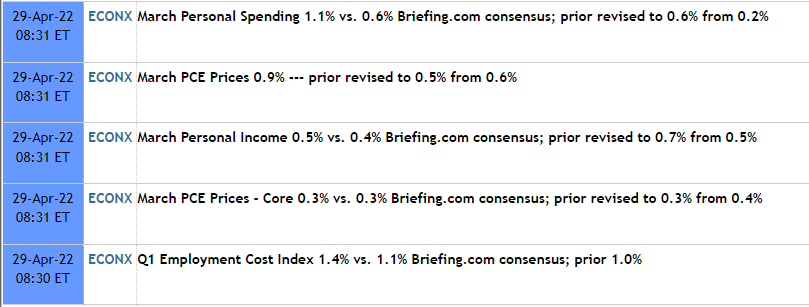

This stack from Briefing.com showed the Core PCE and the PCE deflator being revised lower from February’s data, and while it’s easy to intellectualize away, it’s more telling for me that the mainstream financial media rarely mention this because it doesn’t make for anxiety-inducing headlines.

One of my favorite economists is Brian Wesbury at First Trust. He and Bob Stein do a very good job explaining the data, month in and month out. Westy is an inflation bull and for good reason. Maybe Mr. Buffett and Berkshire’s adding more to their Chevron (CVX) position (announced this weekend) means the Energy complex will be well bid all year. Good technician’s are telling me that the spike in crude oil in early March ’22 was likely the top for crude.

SP 500 data:

- The SP 500’s forward 4-quarter estimate this week jumped to $234.97 from $234.04;

- The PE on the key benchmark fell to 17.5 from last week’s 18.25x;

- The SP 500 earnings yield jumped to 5.69% from last week’s 5.48%;

- The quarterly bottom-up EPS estimate jumped to $53.03 this week from $51.93 last week;

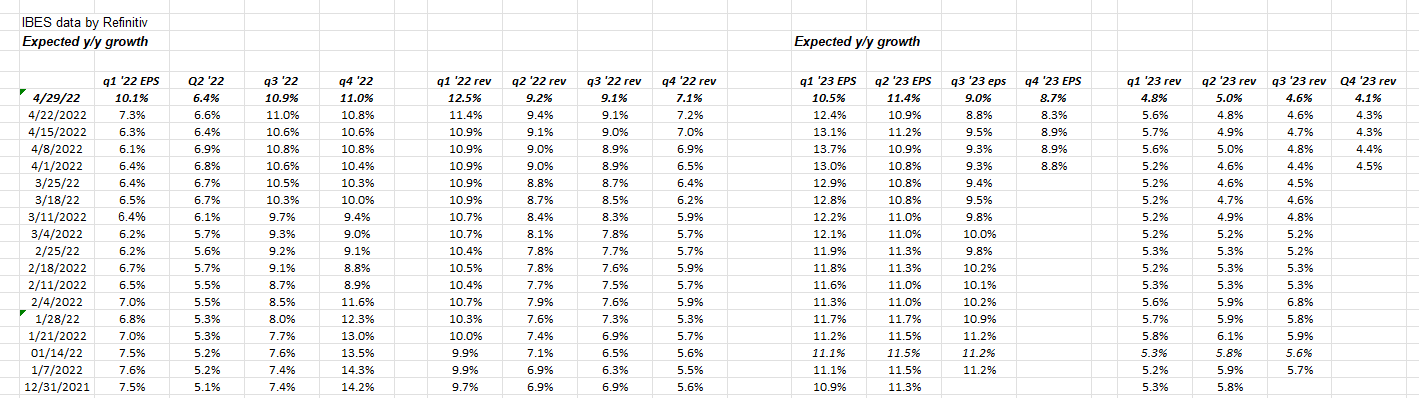

Here’s another data point: SP 500 EPS revisions are still becoming more positive:

Source: IBES data by Refinitiv

Note the positive revisions from last quarter or Q4 ’21 (lower black box) and now look how positive or “up revisions” have improved as we’ve moved through April ’22. This could be a lot of energy names, or basic materials or commdity stocks, but what’s interesting – for all the financial company’s I follow – most of them saw slightly higher EPS revisions, but even stronger revenue revisions. (That’s an article for another time, if I can find the time.)

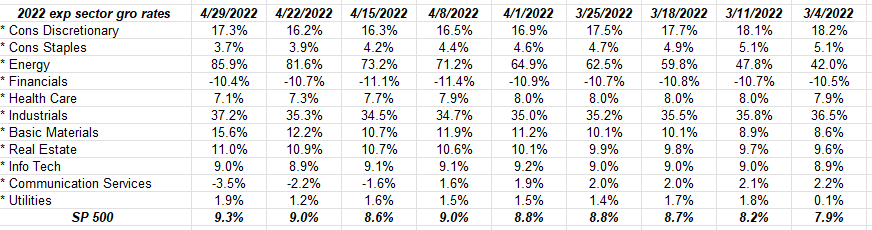

Here’s how full-year calendar 2022 EPS estimates have changed since early March ’22:

Source: IBES data by Refinitiv

Readers can see 8 of the 11 SP 500 sectors saw their expected EPS growth for 2022 increase in the last week, and increase since early March 22. It’s important to keep the longer horizon in mind when quarterly earnings come out.

One caveat: because Amazon and Apple’s quarterly earnings were released Thursday night, April 28th, Amazon and Apple’s revisions might not be in the IBES data yet since the report is cut off on Thursday night. For example, look at Consumer Discretionary, and how it’s expected growth rose last week, which is a little surprising given Amazon’s weight in the sector. It will be looked at next week.

Quarterly SP 500 expected EPS and revenue growth:

The data is from Refinitiv’s “Earnings Scorecard” while the table is my own.

Of all the data collected and re-organized by this blog, this table is one my favorites.

Readers can see the expected revenue growth along side the expected EPS growth over time by quarter.

Summary / conclusion: While SP 500 earnings are coming in better-than-expected in the aggregate, the market is almost totally ignoring it and focusing on the Fed and the expected 50 bp increase this week. I do think a lot of the stock market’s reaction will be predicated on Powell’s tone following the announcement, i.e. does he sounds as hawkish or is his commentary more dovish.

The other critical data point is Friday’s April ’22 jobs report. Briefing.com’s and consensus numbers are around 400,000 net new jobs added for both gov’t and private payrolls.

There are two other aspects to SP 500 earnings data that deserve separate posts so they will come Monday or Tuesday of this coming week.

Take all this with a grain of salt. Past performance is no guarantee of future results and readers should weigh all the information in light of their own situation. Capital markets change quickly both positively and negatively.

Stay on your toes – this is a very big week for the Fed.

Thanks for reading.