Contrary to most investors thinking that gold is primarily an inflation hedge, thinking about gold and its correlation to long-term equity returns, my own opinion is that gold is really a hedge for sub-par equity market returns, and gold and the GLD really adds “alpha” (so to speak) when long-term equity returns are below-average.

Because the GLD ETF only came public in 2005, I have to work from memory from the late 1970’s to through the early 2000’s on what happened with gold bullion and the physical gold that was traded in the 1980’s and 1990’s.

By the late 1970’s when i was a kid studying money & banking (and doing a none too good of a job at it in fact), gold peaked around $800 an ounce, which was sometime around the 1979, 1980, time period

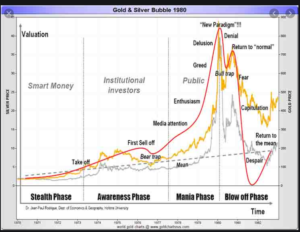

Here’s a chart of gold in the 1970’s:

The chart shows that gold bullion did peak near or just above $800 in late 1979, or early 1980.

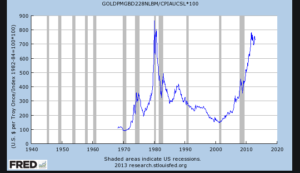

Here is another chart from the FRED (St. Louis Fed database) that shows the subsequent gold action from 1980 through 2013:

So with one of the most robust equity bull markets of the 20th Century, from 1980 to 2000, gold fell from $800 to $200 an ounce, eventually bottoming in late 1999 between $200 – $300 per ounce.

From gold’s low in 1999, early 2000, it took off and traded up to $1,850 per share in September, 2011, and then correcting down to $1,000 by late 2015 (using GLD and its price for the bullion proxy).

So what’s the nexus or what’s the correlation between the 1970’s, 1980’s, 1990’s and then 2000 through 2011 ?

In the 1970’s gold really didn’t take off until the mid 1970’s (top graph) even though the SP 500’s cumulative return for the first half of that decade was -3%. In fact the 1973 – 1974 bear market for the SP 500, which was 50% at it’s peak, was the first 50% correction in the SP 500 since the Great Depression or the 1930’s. Soaring gas prices, the Iran Hostage Crisis, and Russia invading Afghanistan all were events during the Jimmy Carter Administration, as was a 20% fed funds rate, and that’s the period when gold took off. (Some will say the big event in the early 70’s was the US dollar converting to a flexible – rather than fixed – exchange rate.)

What’s ironic is that inflation and monetary policy were exact opposites to one another during the late 1970’s (high inflation) and then after housing peaked in 2006 and Great Recession (zero rates and liquidity trap) and gold acted similarly in both periods.

The 2000’s were similar to the 1970’s in that we saw commodity inflation in both decades for vastly different reasons: the OPEC supply shock in the 1970’s (supply driven) versus the “decade of China” from 2000 to 2006 (demand driven) when we saw China growing GDP 15% a year, which drove demand for crude oil (peaked in ’07 at $145 per barrel), fertilizer, coal, and just about any raw material that China could get their hands on.

So what’s the similarities between the 1970’s and 2000 – 2009 other than dramatic gold out-performance within portfolio’s ?

As noted, interest rates and monetary policy were at polar opposites, while commodity inflation was very similar.

Writing this piece, another similarity between the two decades that comes to mind, was that in each decade, the SP 500 fell 50% at one point (or in the case of 2009, twice).

As mentioned previously, the 1973 – 1974 bear market was a 50% SP 500 correction, while most investors alive remember clearly 2001 – 2002, and 2008, both of which were 50% corrections in the SP 500.

The arithmetic “average” return for the SP 500 in the 1970’s was 7.5%, while the “average” return for the SP 500 from 2000 – 2009 was around 1.25% per year.

From Samantha LaDuc (@SamanthaLaDuc) Trading: Sam is more favorably disposed to gold than I am. When we talked about it on twitter, her thoughts on gold’s prospects for “alpha”:

- Currency hedge: would agree with negative correlation with US dollar;

- Crisis hedge: more temporary or short-term, but I think Sam’s right;

- Inflation hedge: post-2008 dispelled this myth I thought, but maybe not;

- Bond proxy: could be same as inflation hedge, i.e. unanticipated inflation causes interest rates to rise and prices to fall – gold can hedge that;

(Sam’s an excellent analyst, but somewhat more trading-oriented than I am for clients.)

Summary / conclusion: Since the primary belief of this blog is that the SP 500 remains in a secular bull market, that began on March 9, 2009, or in April, 2013, when the SP 500 closed above its March, 2000, and October, 2007 highs of 1,550 and 1,575 respectively, ceteris paribis, because of the last 50 year correlation, then I must believe that gold’s direction will be flat to lower over the longer-term, until the secular bull market in US equities ends. Take all this with a substantial grain of salt and draw your own conclusions. Gold seems to do best, when there is the greatest economic uncertainty, and when the SP 500 is poised to correct 50%.

In what was probably the best trade for clients from late, 1999, through the start of the new bull market in 2009, client portfolios had exposure to either gold stocks (like FCX or Phelps Dodge or others that worked in the early 2000’s, but once the GLD came public, all gold-related equity exposure was transferred to the GLD to get the direct correlation to the gold price.

Ultimately the GLD was sold around $160 in 2012.

The whole point of this history lesson was to show how gold traded over long bull markets like the 1980’s and 1990’s, and it seems to be repeating that pattern again with this bull market. However, this could very well be wrong.

(Here are some of this blog’s earlier post on gold, here, and here. )

Thanks for reading.

(Please remember, all opinions on this blog are just – an opinion – and all readers should not only do your own homework, but invest and trade at your own comfort level. Conditions in capital markets can change rapidly.)