Up 26% YTD as of Monday night, October 27th’s market close, the fact that the stock is up that much was a little surprising given the fact that investors are still waiting – 6 years after the stock peaked at $446 per share in March, 2019 – for the airplane manufacturer to generate a positive year of earnings growth.

Boeing has lost $60 in earnings per share (EPS) since the two airplanes went down – the Lion Air Flight in 2018 and the Ethiopian Air Flight in March, 2019 – which sent the stock reeling after a completely tone-deaf response and an appropriate show of respect to the FAA and the regulators.

The stock is still down 50% from it’s March, 2019, high.

That being said, it’s all in the past now and Kelly Ortberg, Boeing’s CEO has adopted the right tenor and stance in his public comments.

The best Boeing news lately came out of a note from Bernstein on October 20th, which noted that the FAA has allowed Boeing to raise production from 38 to 42 planes per month. Per the note, the increase for the Max is 7 per month, with the intent to be eventually cleared for 10 per month in 2026.

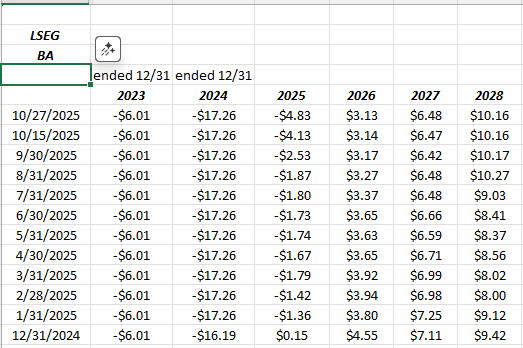

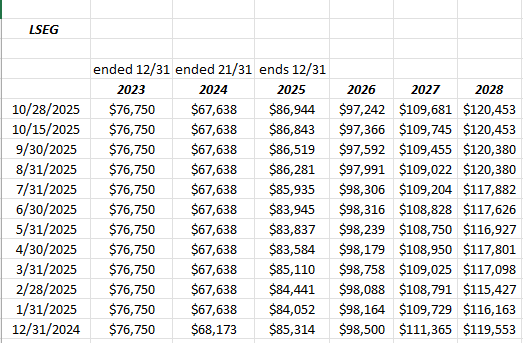

EPS and revenue estimate revisions:

Source of estimate revisions: LSEG

Have to say, I’d prefer to see positive revisions to both EPS and revenue estimates for Boeing, in anticipation of higher production, and higher operating leverage.

Given the disappointments in recent years after doors were flying off planes, and bolts were missing from plane doors, I can understand the analyst reluctance to boost numbers.

Summary / conclusion: The biggest positive to the Boeing story is the Administration support of the the airplane manufacturer, as each of these trade deals that has been signed, seems to have an aircraft purchase order attached to it, with a commitment to buy Boeing aircraft. Obviously, of the trade deals, China matters the most and that deal looks like it will get done in the next few weeks.

Jefferies called President Trump, “Boeing’s Best Salesman” and he hasn’t disappointed. With this research piece dated 10/27, Jefferies noted that announced and previously announced commitments were 50 orders out of Vietnam, 30 orders out of Malaysia, and 45 firms orders out of Thailand, with options.

Like this article written before the July ’25 earnings report, the set-up is the same coming into the October ’25 report i.e. ambiguous EPS and revenue revisions, Boeing still hampered by FAA restrictions, although the constraints are starting to loosen, and this St. Louis union strike which can’t seem to get dealt with.

This blog is long both Boeing (BA) and the ITA (Aerospace and Defense ETF) of which BA is the 3rd largest position in the ETF, at a 7.9% weight.

Despite the constant AI attention in the financial media, the industrial sector has performed well in ’25, even outside GE Aerospace, with the defense stocks and BA being a big part of that. The ITA ETF is up 51% YTD as of last night’s close given what’s happened in Europe and the Trump Administration’s importance on defense spending.

Boeing needs to put up a year of positive EPS and healthy cash-flow and free-cash-flow, the sooner the better.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. None of this information may be updated, and if updated, may not be done in a timely fashion.

Thanks for reading.