Next week, beginning October 13th, at least 30 financial services companies are scheduled to report their Q3 ’25 earnings and the reports appear to cover the market cap spectrum.

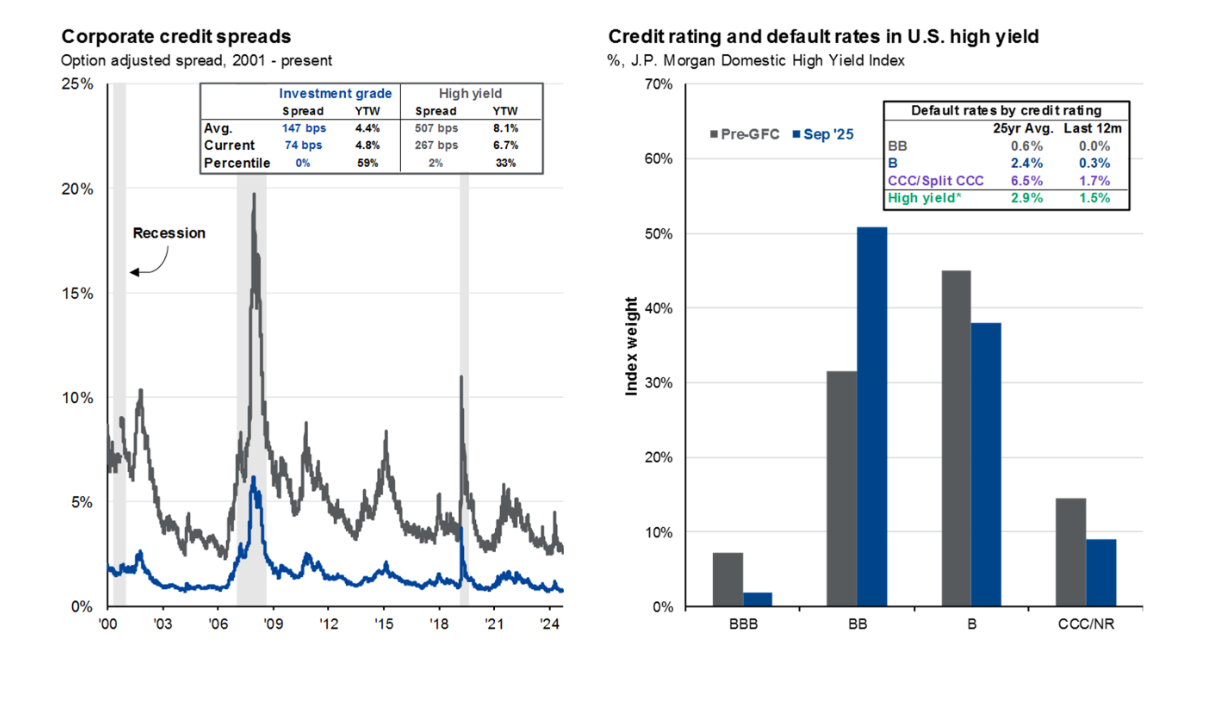

The big issue for banks is usually the credit health of the customer base, and looking at the above slide published by David Kelly, JPMorgan’s Chief Global Strategist, from the September 30, ’25 JPMorgan Guide to the Market (p. 36) it’s shocking to see the corporate default rates this low (defaults detailed by credit rating). Even if we see a tick-up in defaults in the next few quarters, for the CCC-rated credits, the actual default rates today are still less than 1/3rd the “average” default rate for that rating vintage.

Private credit probably has something to do with this, but as of yet I haven’t seen any white-papers or articles of significance from any source discussing how the explosion in private credit the last 10 years, has favorably impacted the publicly-rated corporate credits.

So readers understand, the above slide is corporate credit, not personal credit, i.e. credit card, auto loans, and mortgage delinquencies and charge-off data.

Tuesday morning, October 14th, we will get the 3rd quarter financial results from the following larger-cap financials:

- JPMorgan (JPM): +30.67% YTD return as of 10/7/25

- Citigroup (C): +41.38% YTD return as of 10/7/25

- Wells Fargo (WFC): +17.30% YTD return as of 10/7/25

- Goldman Sachs (GS): +39.65% YTD return as of 10/7/25

- Blackrock (BLK): +15.29% YTD return as of 10/7/25

JPMorgan: When JP Morgan reports Tuesday morning, October 14th, before the opening bell, analysts are expecting EPS of $.83 and net revenue of $45.35 billion for expected y-o-y growth of 11% and 5% respectively. With the tailwinds aiding the banking sector in general including reduced capital requirements, (resulting in higher dividends and share repurchases), healthy capital markets in both the debt and equity underwriting and trading, a very healthy credit environment, (it’s probably close to “peak credit” in late 2025, from both the corporate and personal credit loss perspective), I wouldn’t expect to hear much bad news from JPM’s report on Tuesday morning.

One item to note: JPM’s q3 ’24 quarter was a mild growth quarter with net rev’s +6% and EPS +1%, but Q4 ’24, after President Trump was elected, could make for a very difficult compare for the bank, since JPM put up a 17% EPS beat ($4.81 vs $4.11 estimate) on 11% net revenue growth, as investment banking and advisory fees soared in the Q4 ’24, understandable after the Trump Administration win and the Republican majority in both houses of Congress.

JPM’s 5-year annual trailing return as of 10/7 was 27.01%, versus the SPY’s 16% 5-year annual return for the same period, proving Jamie Dimon’s reign as one of the top CEO’s in the SP 500, probably not just the last 5 years, but the last 15 years.

Where JPM sticks out is the ROTCE (return on tangible common equity) which has consistently been between 20% – 25% for years, where Citi has been closer to 10% and Bank of America (BAC) has been low to mid teens.

Jamie Dimon was a vocal critic of the Biden Administration’s regulatory constraints that were put on banks after 2008, and while some were clearly needed, by the time 2020 rolled around it was time to loosen the reins so to speak, and the Trump Administration and Treasury Secretary Bissent have loosened the capital to be held by banks. JPMorgan has responded by raising their dividend smartly (already) and repurchasing shares. Just in the last 3 quarters alone, JPM has repo’ed almost $20 billion ($19.2 billion to be exact) of common equity.

JPM has been this blog’s largest position for clients over the last several years, but the position has been clipped to keep the stock’s weight in line and with the “macro” so good, you have to wonder how long the credit cycle can continue.

JPM is trading at 15x expected ’25 and ’26 EPS with EPS growth the next two years per the current estimates only expecting 8% and 5% respectively. Where analysts likely get nervous is JPM’s premium to book and tangible book value, which is much higher than Citi and Bank of America’s book value valuations, probably due to ROE.

The final flaw to JPM’s incredible story as a bank and a stock is that Jamie Dimon is likely going to be leaving the bank in the next 3 – 5 years. Iconic CEO’s departing the roost, usually doesn’t bode well for the stock price performance post-departure. I’m sure the bank has a deep bench and good culture, but it’s always tough to find two Jamie’s in a row.

Citigroup: Citi also reports next Tuesday morning, October 14th, before the opening bell, and I look at Citi as the yin to JPMorgan’s yang. A newer CEO – Jane Fraser – who is trying to get the bank up to speed on both a growth and ROE perspective, but JPM’s +20% ROE consistently, is met with Citi’s 8,9,10% ROE every quarter, as Jane and Citi have far more overhead than business to generate the right return.

That being said – ironically – for Q3 ’25, analysts are looking for $1.90 in EPS on $21 billion in net revenue for expected y-o-y growth of 26% and 4%, with Citi’s EPS growth expected to far outpace JPM’s 11%.

Citi is expected to grow full-year EPS 27% in 2025, and then again 29% and 19% in ’26 and ’27, for a stock that is sporting a multiple of 13x and 10X respectively.

Again relative to JPM, Citi’s book value and tangible book value are $106 and $94 respectively, so the stock is just 1x book and tangible book, versus the 2.40’ish metrics for JPM.

Citi was trading under $50 in late 2023, so in just the past two years the stock has doubled in value.

On a pure valuation basis Citi is a screaming buy relative to JPMorgan, but there is no question that operationally, with the depth of JPM’s segments in consumer, corporate, and investment banking, JPM is the right bank at the right time of this cycle to maximize returns.

If someone had read off the five banking / financial services names at the top of this earnings, would you have guessed that Citi would have the best YTD return of all five stocks ?

This blog will be out with separate reviews of Morgan Stanley and Goldman Sachs together, before next week. (Unfortunately, Wells Fargo and Blackrock are not followed fundamentally.)

Summary / conclusion: This blog probably does not own enough Citigroup for clients, and maybe owns a little too much JPMorgan since the stock remains client’s #1 holding across all accounts treated as one portfolio, but this blog has been shading JPM and re-weighting the stock based on appreciation, and not adding enough Citi.

The valuation dichotomy is striking, as is the expected EPS growth for Citi in the next few years relative to JPM’s.

Then again, analyst expectations are not always reality.

This is year 1 of the current Presidential Administration, and the impact of the tax bill isn’t expected to hit fully until tax refunds in 2026, so there is probably more upside to the banks and financial sector in ’26 as the tailwinds remain favorable.

Just be aware of JPMorgan’s very tough compare in Q4 ’25 versus Q4 ’24.

None of this is advice or a recommendation, but only an opinion. Past performance does not guarantee future results. All EPS and net revenue data is sourced from LSEG.com.

Thanks for reading.