Nike (NKE) reported their fiscal Q1 ’26 financial results last Tuesday night, September 30, ’25, and while the stock rose $4.50 the next day following the quarter’s results, the headwinds cited during the conference call, might mean the turnaround will be slower than originally suspected.

The big surprise for me personally was that Nike raised their expected tariffs to $1.5 billion, from the expected $1 billion originally forecast in June ’25. Nike has 1.497 billion in fully diluted shares outstanding, so Nike is effectively being hit with a $1 per share tariff impact, versus the $0.67 per share one quarter ago.

While this could change with a Presidential tweet, the size of the tariff impact cannot be ignored.

EPS and revenue estimate changes for Nike from pre to post-earnings release:

- FY 2028 EPS estimate: was $3.09 pre-release, which fell to $2.97 post-release;

- FY 2027 EPS estimate: was $2.43 pre-release, which rose to $2.49 post-release;

- FY 2026 EPS estimate: was $1.66 pre-release, which fell to $1.67 post-release;

- FY 2028 revenue estimate: $50.716 bl pre-release to $51.340 bl post-release;

- FY 2027 revenue estimate: $48.09 bl pre-release to $49.103 bl post-release;

- FY 2026 revenue estimate: $45.77 bl pre-release to $46.73 bl post release;

While EPS estimates were rather mixed, each of the fiscal year revenue estimates were higher post-earnings, which tells us the Nike margin picture is very much in question moving forward, much of which could probably be explained by the tariff guidance, and trade ambiguity.

Treasury Secretary Bissent did say on a CNBC interview last week that the US expects a “big breakthough” with China within the next month, or before the November 10th tariff review. Will Nike benefit from this – personally I can’t say and we will just have to see what unfolds in the next 30 days.

There were many positives for Nike in the fiscal Q1 ’26 report, but as a long-time analyst, I try to watch the numbers closely and the lack of any real upward movement in Nike’s EPS or revenue estimates was somewhat disconcerting.

The metric that improved the best in my opinion was that North American revenue improved to +4% y-o-y, versus the -3% expected, as the running segment improved 20% y-o-y.

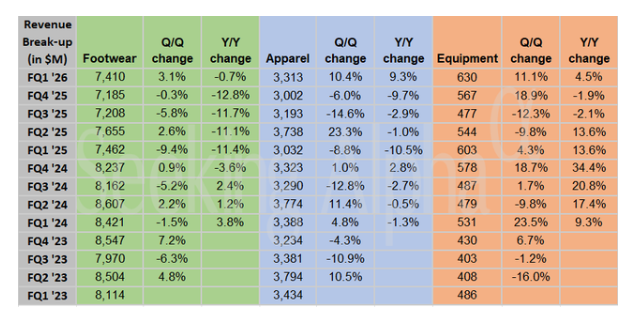

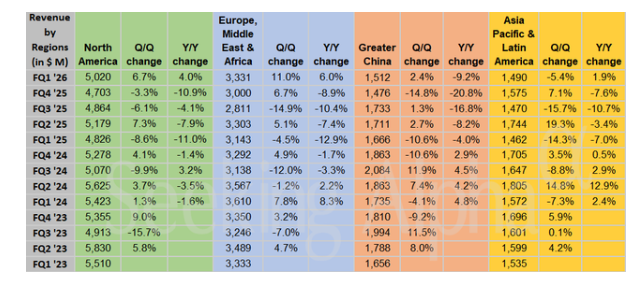

These two charts from www.SeekingAlpha.com give a good rundown of historical numbers:

The table at the top shows the Nike revenue breakdown by product line (footwear, apparel and equipment) while the 2nd table shows the Nike revenue breakdown by region.

The China region today is 13% of Nike total revenue and 42% of EBIT, and for this latest quarter, China revenue fell 9% y-o-y, while EBIT fell 25% y-o-y.

Summary / conclusion: While clients remain long the stock, the turn for Nike will not happen overnight, unless something dramatic happens with tariffs and the China relationship.

Elliott Hill and the team are making progress on a playing field that is decidedly tilted against them.

There was not a whole lot said about the SKIMS launch, but the earnings release was three days after the launch, so Nike management likely decided to hold off on any disclosure.

I do sense that Elliott Hill is “underpromising” with the intent to “over-deliver” down the road.

Thanks to Matt Friend, the Nike CFO, who released Nike’s 10-Q within a day or two after earnings, ( I thought this was a first) since it gives analysts / investors a way to look over the cash-flow statement. Nike’s fiscal Q1 each year is typically the weakest. Free-cash-flow for Q1 ’26 was just $15 million, which is quite small given the 20-quarter average is $1.2 billion per quarter, but some dated inventory is still bleeding out the door, and again, the fiscal first quarter is typically the weakest metrics for the year.

It has surprised me that given the decline in the stock since late November ’21 from it’s $179 all-time-high, free-cash-flow has remained positive almost every quarter for Nike.

Small amounts of Nike were added after the earnings release this past week, with the intent to add more gradually as we move through the quarter and wait for the next earnings release in late-December ’25.

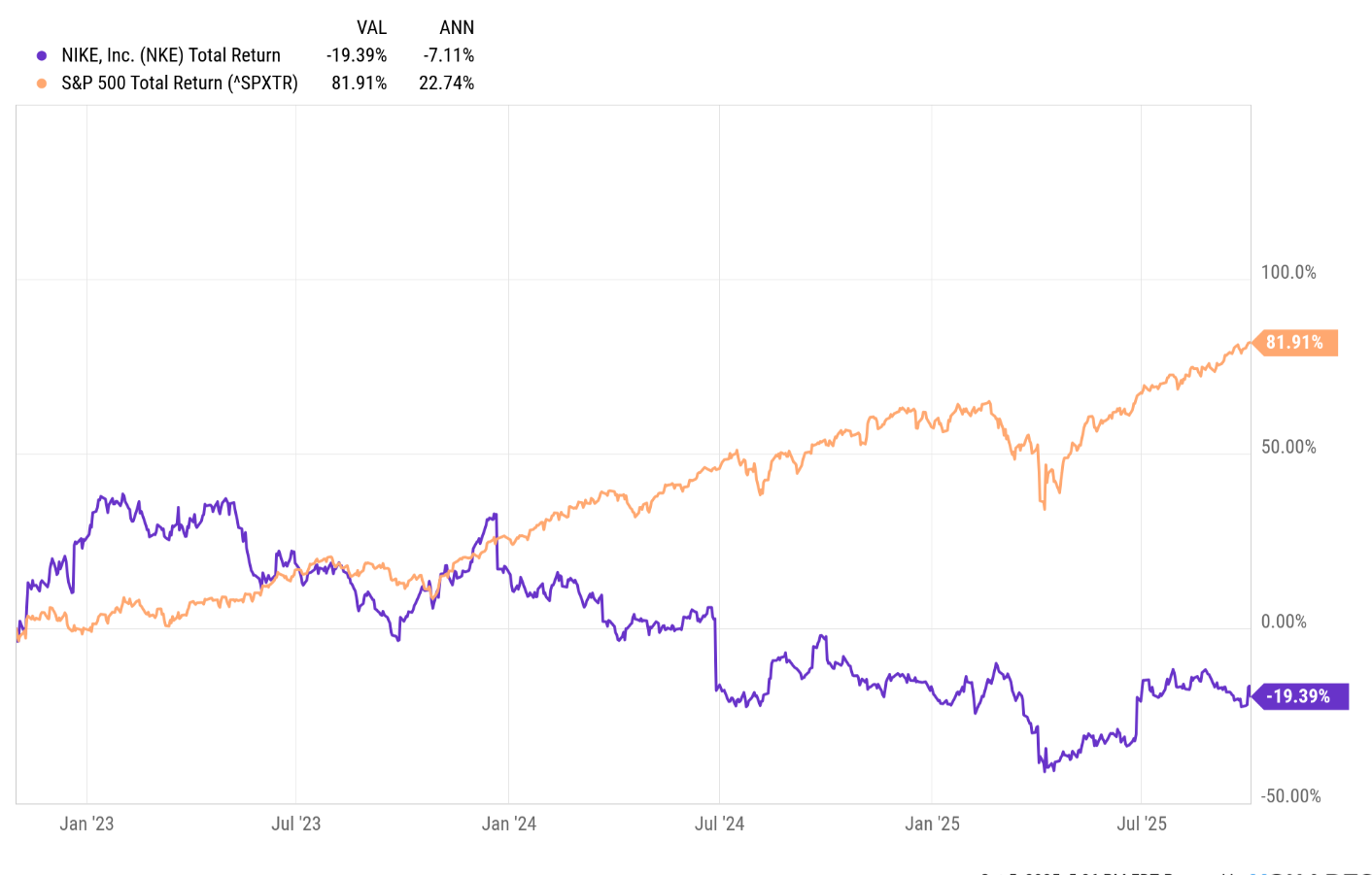

This is a longer-term chart (source:Ycharts) showing Nike’s total return versus the SP 500’s total return from 11/1/2022 through 10/3/25.

That’s a huge discrepancy in “annual return” which makes Nike one of the better “uncorrelated” stocks from a portfolio construction standpoint.

Nike went through a similar period in the late 1990’s from something called the “brown shoe” craze starting in 1997. The stock underperformed dramatically in the last few years of the 1995 – 1999 bull market in the SP 500, then broke out on it’s current run which ended November ’22, which means the dramatic outperformance for Nike began as the SP 500 and the Nasdaq peaked in the early 2000’s.

The same dynamic is setting up again in the stock.

Mark Parker, the former Nike CEO before John Donahoe, brought Elliott Hill back to Nike after Elliott left Nike when Donahoe was named CEO in 2020, and if you followed Nike during the Mark Parker years you know what a great CEO he was. Mark Parker convinced the Nike board to re-hire Elliott Hill, and if Mark Parker believes in Elliott then the buy-side investment community probably should too.

Given the tenor of the conference call my guess is Nike will probably see another flatter year in fiscal ’26 (ends May 31 ’26) and investors should look to the back half of calendar 2026 before the stock starts to turn the corner, meaning low teens EPS growth, high-single-digit revenue growth and a move towards mid-teens operating margins.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. None of the above information may be updated, and if updated, may not be done in a timely fashion.

Thanks for reading.