In market environments like today, it’s very tough to attempt to discern when a stock or security has fully discounted all the negative news that’s been published on the stock.

Tesla is the poster-child of that process for the Q1 ’25 earnings season.

After the electric vehicle (EV) giant, released it’s Q1 ’25 production and deliveries (362,000 and 366,000), in early April ’25, the stock turned south once again, although it had been selling off since December ’24, when it hit a high of $488 around Christmas. (Don’t kid yourself, Tesla trades like a soybean future, and this was well before Elon went “political”.)

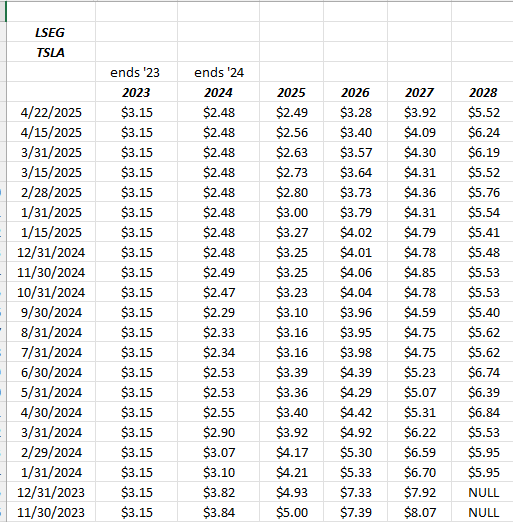

One way to get around sentiment is to look at the numbers: coming out of the Q4 ’24 earnings release, the sell-side consensus was looking for +14%, +30% and +20% respectively for EPS growth for ’25 through ’27. Today’s those same estimates now are expecting +3%, +32% and +20% respectively.

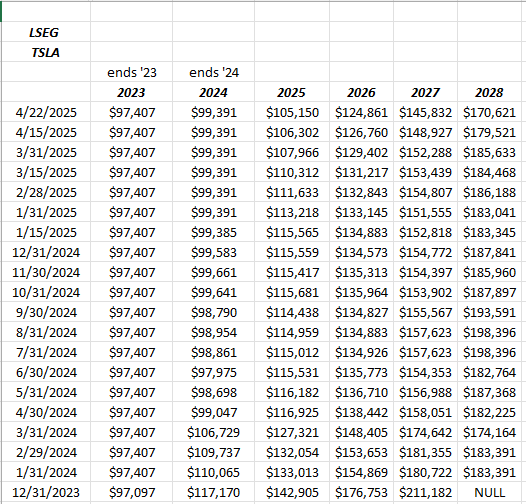

Revenue growth isn’t much different: after Q4 ’24 was released the sell-side consensus was looking for +13%, +18%, and +16% for ’25 – ’27 in terms of expected revenue growth, while the new current estimates (as of this morning) reflect +8%, +19%, and +17% for the same years, ’25 through ’27.

Estimates for tonight expect $21 billion in revenue, $1.1 billion in operating income, and EPS of $0.39 per share for expected y-o-y growth of -1%, -6% and -13%. (Frankly I was expecting much bigger percentage declines.)

The key metric above is the revised expectations of revenue growth for ’25 from January ’25’s estimate of +13% to the current +8%. Tesla is a business with a high degree of operating leverage i.e. small changes in revenue account for large changes in operating income and EPS.

What are the positives ? The “energy-related” revenue (energy storage biz) is still growing at a rapid rate, doubling in size in 2024 and now accounting for 23% of total revenue) and what’s really critical is Elon and the team continue to improve auto-related gross margin, by lowering cost-of-goods-sold. The auto GM is nowhere near where it was in late 2021 when interest rates were at zero, but the rate hikes in 2022 and then Elon’s politicization in the last year, have impacted auto sales. Volume (sales and production) also impact gross margins as well.

The biggest negative that came out this weekend on the stock is that the “low-price” or under $30,000 Tesla version would be delayed. It was supposed to be out in June ’25, and naturally and maybe for good reason, the reason the sell-side gives for the delay is Elon’s preoccupation with DOGE and his time spent in Washington.

The other negative is that Waymo is thought to be well ahead of Tesla in FSD (full self driving or autonomous driving).

Technically, Tesla needs to regain the $250 area or 200-week moving average in my opinion. The stock hit a multi-year low of $100 in early ’23 after falling from $414 in November ’21.

Tesla EPS and revenue estimate revisions:

Tesla EPS estimates have been reduced by 50% in 2025, and more than 50% for outer years.

Revenue revisions negative as well.

Source: LSEG as of this morning, 4/22/25.

Tesla’s valuation:

It’s still nose-bleed level, only complicated by the falling EPS and revenue estimates:

- 91x expected ’25 EPS

- 68x expected ’26 EPS

- 6.71x 4-quarter trailing revenue

- 85x 4-quarter trailing cash-flow

- 153x 4-quarter trailing free-cash-flow

These numbers could change quickly with a low-end, “under $30k” version of the Tesla

Summary / conclusion:

Tesla’s a tough long today, and for good reason. The delay of the low-cost model was not well received by investors. Ron Baron of Baron Capital was an early investor in the stock in the early part of last decade, and he was on CNBC in 2024 after the company delivered their “June ’25” launch expectations for the low-cost model, noting the cheaper version was critical to the Tesla story. Tesla is or was Baron’s #1 position in his fund.

The positive to the Tesla story is that the EV maker would benefit greatly from lower auto-financing rates, i.e. lower interest rates. Personally, I do think Jay Powell will start lowering interest rates this summer, but only after evaluating the impact of tariffs on inflation data (particularly PCE data) and if crude oil continues to decline.

Tesla’s stock troubles started in 2022 when the Fed hikes the fed funds rates from zero to ultimately 5.375% in July ’23.

None of this is advice or a recommendation but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal even for short periods of time. None of the above may be updated and if updated may not be done in a timely fashion. readers should gauge their own comfort with market volatility and adjust accordingly.

Thanks for reading.