There is a lot of focus on the 10-year Treasury yield thanks to comments from President Trump and Treasury Secretary Bessent.

This week the hotter-than-expected core CPI (+0.4% actual vs +0.3% expected) sent Treasury prices lower, and then they rallied back, only to end the week unchanged. The 10-year Treasury yield closed this Friday, February 14th, 2025 at 4.48%, and closed last Friday, February 7th at 4.48%.

Begin to get anxious about inflation and the Treasury market if the 10-year Treasury closes above the October ’23 high of 4.99% – 5% on volume.

You’d never guess this listening to the mainstream financial media.

SP 500 earnings:

- The forward 4-quarter estimate ended this week at $270.46, versus last week’s $271.24 and January 3rd’s $272.67.

- The PE on the forward PE ratio is now 22.6x vs 22.2x and January 3rd’s 21.8x

- The SP 500 earnings yield is now 4.42%, versus 4.5% last week, and 4.6% as of January 3rd ’25.

Here’s what’s worth watching:

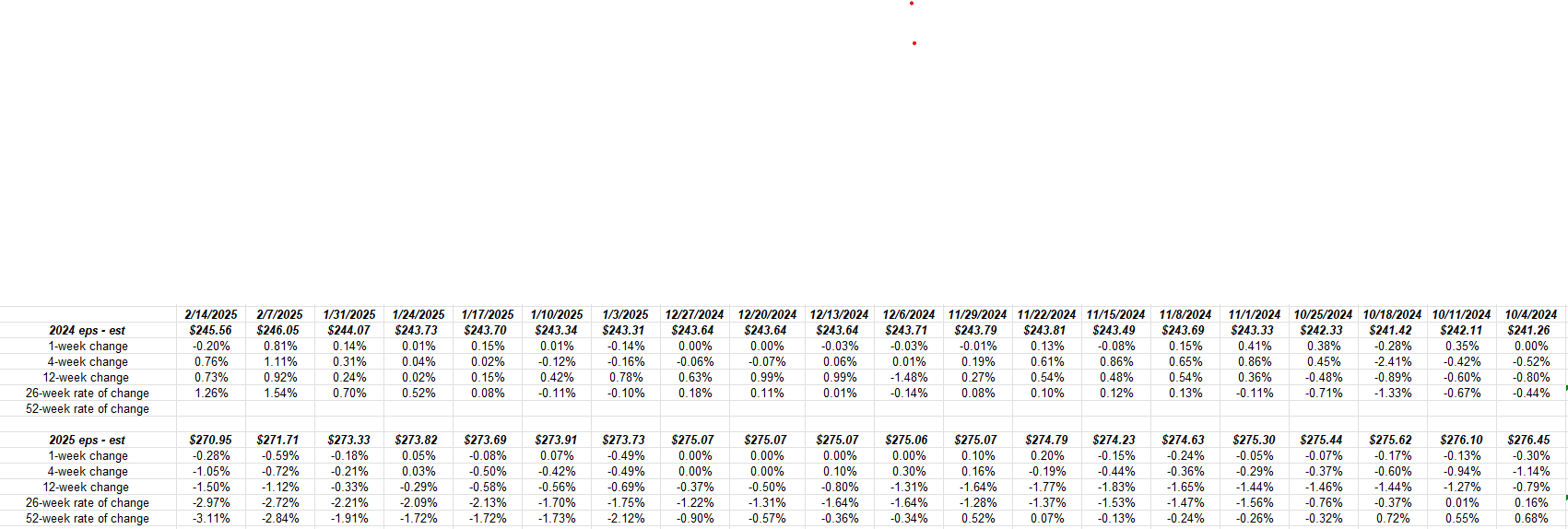

Click on the above spreadsheet and note the rates of change for the expected 2025 SP 500 EPS estimate.

Part of this weakness is a function of how strong ACTUAL Q4 ’24 SP 500 earnings turned out:

![]()

This spreadsheet cut shows the weekly progression in expected Q4 ’24 SP 500 EPS and revenue growth, starting with the beginning of the quarter. Q4 ’24 earnings unofficially ends this week with Walmart’s earnings, but readers can see how strong the “upside surprise” was for both Q4 SP 500 EPS and revenue.

The point being that 2025 estimates will naturally be cut a little more based on the strong Q4 ’24.

As it stands today, 2024 SP 500 EPS and expected 2025 EPS are both expected to grow 11% each year. 2024 EPS has been revised higher the second half of calendar 2024 from 9%, while expected 2025 SP 500 EPS growth has been revised lower from 14% – 15% last October ’24 to 10% as of this weekend. (Click on the spreadsheet below to see the expected growth for the SP 500 EPS from 2024 – 2026. )

![]()

Summary / conclusion: While this might cause some readers some anxiety or alarm, the fact that we have a new Administration, with a whole new set of tariff initiatives not to mention other initiatives, is likely causing some angst on the part of analysts that might be unsure how to factor in healthcare policy commentary, defense industry commentary, and many other aspects of the new Administration.

While the megacap 7 or megacap 10 have seen some pressure on 2025 revenue estimates, the negative revisions are not yet too concerning.

A problem would arise if we started seeing negative pre-announcements, from which we could infer that companies are seeing economic conditions deteriorate faster than their previous guidance expected.

Corporate credit spreads continue to remain well-bid. Even with inflation uncertainty and a little Treasury volatility, credit spreads continue to grind lower.

That’s a plus for the economy.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal, even for short periods of time. None of the above information may be updated, and if updated, may not be done in a timely fashion.

Thanks for reading.