FedEx revenue has declined on a y-o-y (yoy) basis for the last 6 quarters.

When the transportation giant reports their fiscal Q4 ’24 after the closing bell on Tuesday night, June 25th, 2024, here’s what the street consensus is expecting:

- Revenue: $22.1 billion for yoy growth of 1%;

- Operating Income: $1.8 billion for yoy growth of 4%;

- EPS: $5.36 for yoy growth of 9%;

Readers will likely consider those metrics “uncompelling” in the world of Nvidia and large-cap tech, but it’s the first expected, positive, yoy growth for the three primary FDX metrics since mid-22.

In fact, operating income hasn’t been positive for FDX since May ’22 or the last 7 quarters.

In fiscal Q3 ’24, reported in March ’24, FedEx stock popped after Express margins expanded to 2.11% while Ground margins also came in better-than-expected at 11.1% and Freight margins slid to 16%, down from 20% the prior quarter. (Freight is FDX’s small business segment at 10% of total revenue.)

The two big initiatives that FedEx announced in May ’23 were “FedEx One” which was the merging of the three FedEx segments – Express, Ground, and Freight – into one consolidated income statement starting with the next quarter i.e. fiscal Q1 ’25 (which began June 1 ’24) – and “FedEx Drive” – by far the more important initiative – is the removing of $4 billion of “permanent cost reductions” from the FedEx cost structure by May ’25.

For some perspective, FedEx generated $81.5 billion in expenses for the trailing twelve months ended February ’24, so $4 billion is roughly 5% of total annual expenses (4.91% to be precise) and my guess is – given some of the commentary on the conference calls – that FedEx will be removing greater than $4 billion by the time “Drive” is over.

Here’s some previous articles written on FedEx: here, here, and from Seeking Alpha (here and here).

Here’s a little history on FedEx operationally:

In the last 10 years or so, FedEx Express, the original segment started by Fred Smith when FedEx was founded, has been a drag on returns. It’s a very capital intensive business, and returns have been eroded for a number of reasons over the years . The FedEx Ground business wasn’t started until the year 2000 and it’s been a very healthy business for FedEx, with Ground revenue being a smaller percentage of FedEx total revenue than Express, but Ground operating margins usually “carrying the freight” (bad pun intended) as a bigger percentage of FedEx’s total operating margin for each quarter. (Obviously, results can be volatile with a capital intensive business like FedEx, but readers should get the point between the two segment margins and their overall contribution to FedEx’s total operating margin.)

And that’s the rub: whenever FedEx hit a 10% operating margin over the last 25 years (this blog started modeling FedEx back in the mid 90’s) it usually meant “peak FedEx stock price” as well.

Raj Subramaniam, the FedEx CEO who took over after Fred Smith was appointed Executive Chairman, in the last 18 months has said that FedEx’s goal is for consistent (within reason) 10% operating margin over time, but I personally think Raj and the FedEx management team will have to do better than that for shareholders.

Recent history for FedEx is that parcel volume exploded beginning in March, 2000, with the Covid lockdown. FedEx had to take part-time employees, pay for 2nd hand freight delivery and push the proverbial bowling ball through the snake (in terms of package demand and logistics), but even with parcel delivery demand soaring, FedEx’s operating margin couldn’t get higher than 8% – 9% and then when demand began to “normalize” in 2002, the stock fell from the pandemic high of $315 – $320 in mid ’21, down to the $150 area in September ’22.

The point being that the US and the rest of the world are returning to a more normal ecommerce and freight delivery market the last 24 months, and Fedex will be greatly served to continue to rationalize margins and push for better efficiencies.

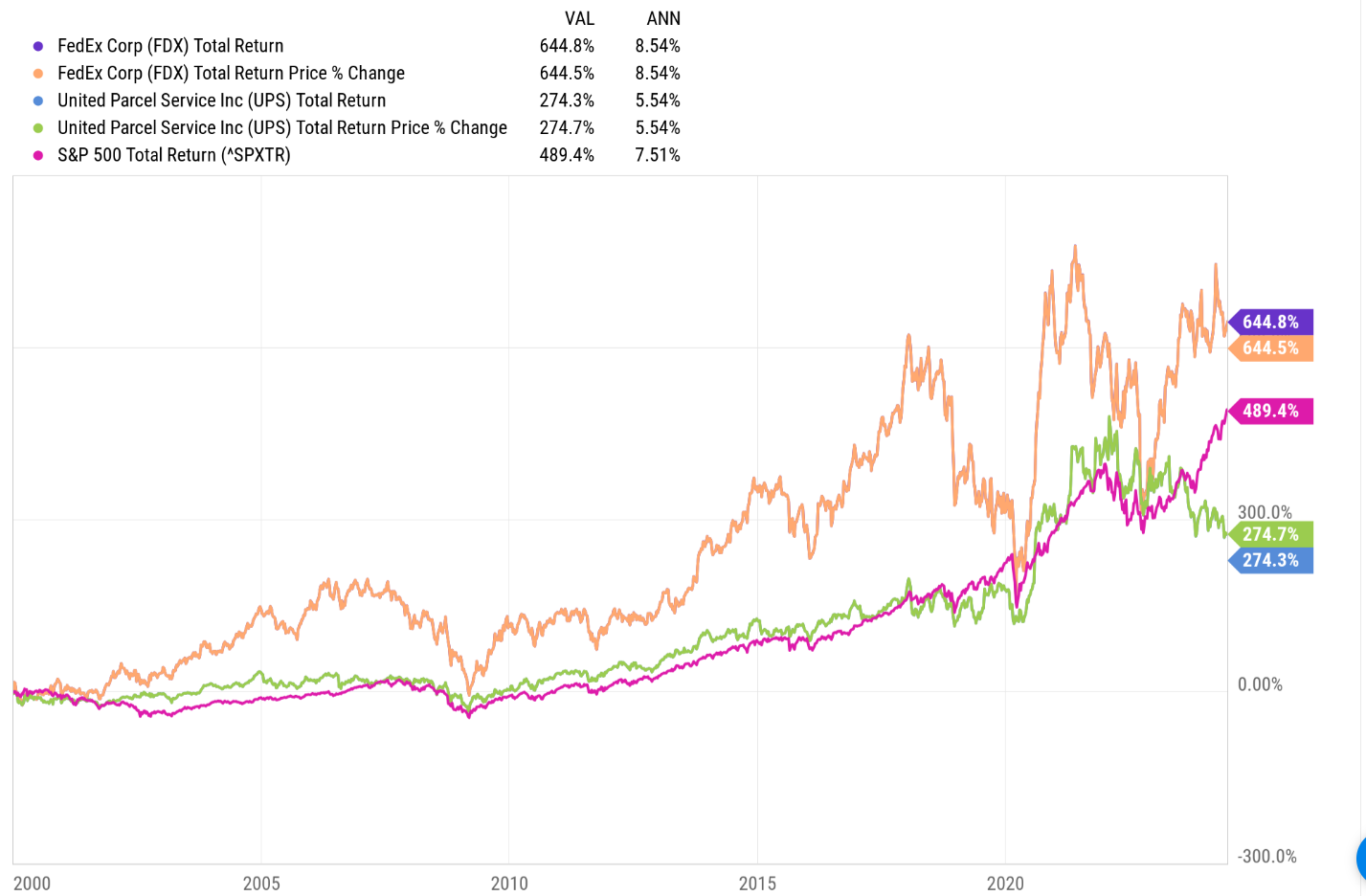

FedEx Returns vs UPS and SP 500:

This Ycharts graph surprised me since it shows FedEx outperforming both the SP 500 and UPS since January 1 of 2000. I suspect a lot of that is due to Ground and it’s relative performance over the last 25 years, but FedEx is a much more capital intensive business than the average SP 500 company.

Over the last 25 years, FedEx has outperformed UPS by about 300 bp’s a year and the Sp 500 (total return) by 100 bp’s per year.

Valuation:

If fiscal Q4 ’24 meets consensus, FedEx will have grown EPS 19% in fiscal ’24 but more importantly EPS growth as of today is looking for 18% and 13% growth in fiscal ’25 and ’26 respectively, while the stock is trading at a 12x – 13x PE looking at the next 3 years expected EPs growth.

Just like last quarter, (see above preview linked), FDX remains cheap on a PE basis.

Expected revenue growth – critical since there has been no yoy growth for the last 6 quarters, is expecting -3% for full-year fiscal ’24 and then 3% and 4% in fiscal ’24 and ’25 respectively, which will be a big improvement.

A capital intensive company that can generate mid-single digit revenue growth on an expanding operating margin, with the $4 billion cost savings, will see EPS growth likely accelerate sharply.

The other valuation metric that usually signaled a stock price peak for FDX was 1.0x price-to-sales (really market-cap to sales) and with trailing-twelve-month (TTM) revenue about 0.61x – 0.62x, Fedex’s $81 billion market cap today, still indicates the stock is undervalued.

If and when FDX trades up to a $90 – $100 billion market cap, it’s likely getting fully-valued given history, BUT (again) much depends much depends on the operating margin.

Fiscal ’25 EPS and revenue is looking for $20.97 in EPS and $90 billion in revenue for an expected +18% EPS growth and +3% revenue growth.

This blog estimates fair value for the stock is $280 to $310, while Morning star has the stock overvalued with a fair value estimate of $235 – $240.

Summary / conclusion: The nice aspect to Raj Subramaniam and the FedEx management team is that they control their own destiny to some extent by reducing expenses and shrinking the capital intensity of the business, but they still need to contend with a global business ( a big chunk in Europe that was sidelined by the TNT hacking attack and the mess around Brexit), and now the slowing of China’s economy.

When this blog ran the performance numbers for FDX and UPS from 2005, 2010 and 2015, FedEx did NOT outperform the SP 500 through June 21, ’24, but did outperform UPS until 2015. The last 9 – 10 years is when the under-performance began, and I suspect this is when Express started to cause issues in terms of being a drag on returns.

The stock is cheap today on a PE basis (price-to-growth), on a price-to-sales basis, and a free-cash-flow yield basis.

Playing with the valuation numbers, and price-to-sales, a $375 stock price puts a 1.0x price-to-sales valuation on the stock, with no change in fully diluted shares outstanding, but take that with a considerable grain of salt, given all that needs to happen.

Come Tuesday night and the earnings release, I have no clue whether the stock will be up or down 5% – 10% after the numbers come out, but I do think FedEx Drive is a longer-run winning solution for a capital intensive business. That being said I think Fedex One or the consolidation of the three segments into one P/L and traditional reporting statement, is not a plus. FedEx was a leader in terms of company disclosure of financial and package volume data. FedEx gave investors a LOT of good information to cogitate over every quarter. That appears to be going away, which I don’t think is a plus.

This fiscal Q4 ’24 to be reported Tuesday night is the last quarter where investors will get segment information (which I assume investors won’t get segment margins disclosed) as well as volume data.

Personally I think it’s a shame, since I’ve always favored investing in companies that disclose more rather than less.

However, let’s see what the new disclosure looks like, which begins next quarter, fiscal Q1 ’25 ended August ’24.

Clients hold a 2% position in the stock, headed into earnings.