This week the blog is starting off with what I call the “spot curve” of the forward 4-quarter estimates of the SP 500. (What does the forward 4-quarter estimate tell us 1,2,3 and 4 quarters from now ?)

In other words, if we look at the “forward 4-quarter estimate” today, and then add one future quarter as one quarter falls off, what does the rate of change tell us, if anything ?

Readers – if you click on the above table and expand it – you’ll see that forward revisions continue to be positive across all time trends, i.e. sequential, 4-week rate of change, and then this week for the first time, the 12-week rate of change for the quarterly estimates that were added (by LSEG) for 2025, around April 1 ’24.

What’s abnormal with the above pattern is that typically we see negative revisions for the sequential rates of change at this time of the quarter, as analysts pull in their estimates, and get more conservative as the 2nd quarter ends, and until 2nd quarter earnings start being reported around July 10th – 12th.

Instead – as the table shows – we see consistently steady, upward revisions.

A number of brokerage firms and Wall Street strategists have raised their SP 500 targets for year-end 2024.

SP 500 earnings estimate revisions could be one reason why.

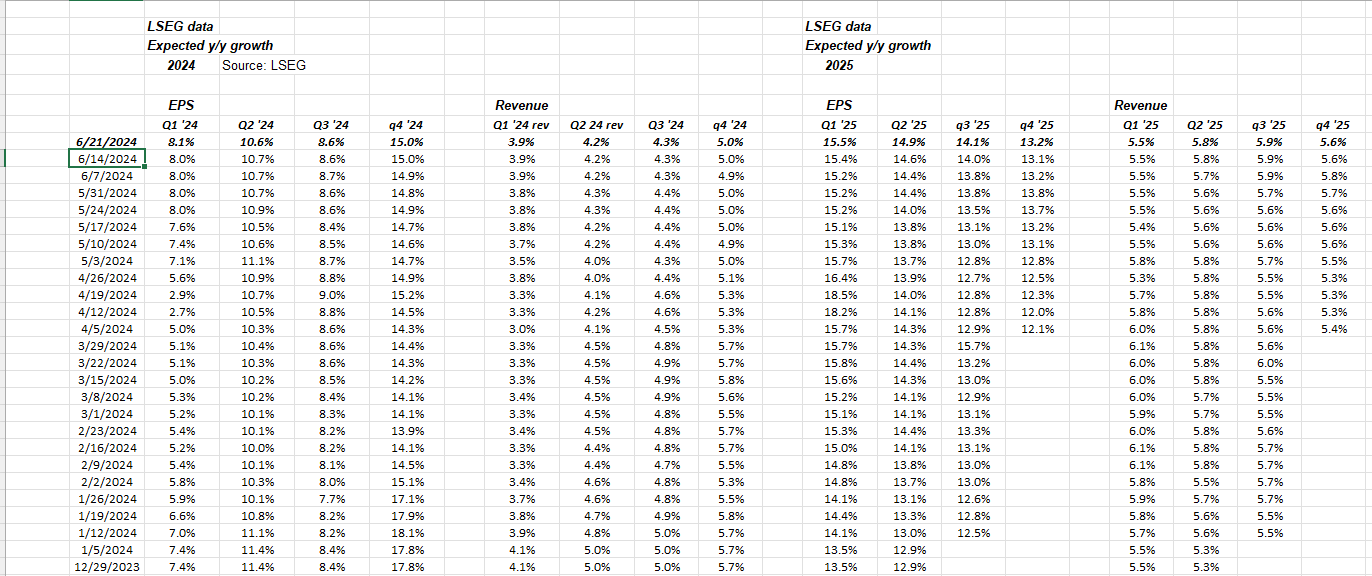

This is another table that is updated weekly from LSEG data: note the 2015 SP 500 EPS and revenue data.

I’m starting to wonder if these estimates are starting to factor in a Presidential election result.

Without being political, let’s face it, a Republican victory similar to 2016, is usually “very pro-growth” for the US economy meaning policies are typically passed or enacted that support above-trend GDP growth, low unemployment and low inflation. This is typically pretty healthy for the stock market(s) and not so conducive for higher bond prices.

Don’t assume this yet with the 2025 data though, but the numbers do at some point start to discount actual 2025 EPS and revenue for the SP 500. Readers might think we are still too far out from 2025 for the estimates to be realistic, but readers would be surprised.

Personally I’ll pay much more attention to 2025 estimates as we roll through July ’24 earnings for Q2 ’24 and see how the numbers change. We’ll see what the revisions look like as we move through the 3rd and 4th quarters.

SP 500 data:

- The SP 500’s forward 4-quarter estimate this week is $253.54, versus last weeks $253.42, and March 31’s $242.94. I just realized the forward 4-quarter estimate has risen $11 in the last 10 weeks.

- If we assume it’s the next quarter (i.e. July ’24 through June ’25) already, the forward estimate (1 quarter forward, see the top table) is $262.30, and that’s a $9 expected increase, but much depends on actual Q2 ’24 results.

- The PE ratio on the forward estimate is 21.55x, versus 21.6x as of 3/31/24. What’s interesting about tracking the PE versus the forward estimate is that the first 90 days of the year and the nice rally in the SP 500 in Q1 ’24, was all “PE expansion” but the 2nd quarter rally to new all-time highs after the April correction, has been all EPS growth. The SP 500 PE is almost identical to where it was on March 31 ’24. (Navel gazing, I know. This is my life.)

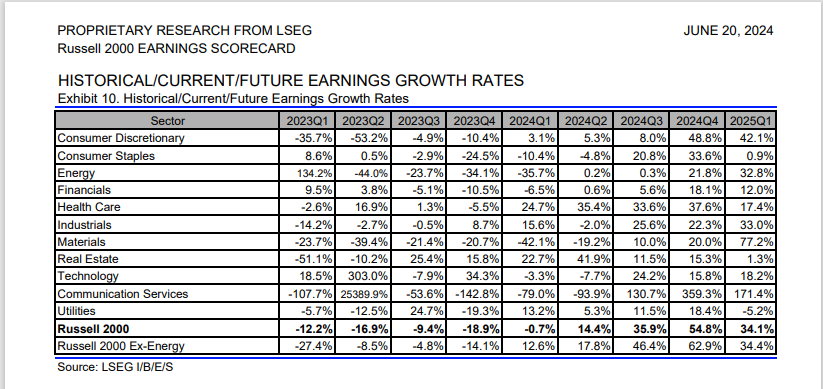

Russell 2000 data: faces easier compares for rest of 2024:

What might be telling for readers is that 2023 was not great for Russell 2000 earnings, so 2024, particularly the back half of the year, will see very favorable “compares” against the same quarter of 2023. It’s not the sole reason to have a position in the IWM, but as it’s return versus the SP 500 becomes more disparate and disconnected, don’t ignore the asset class.

This blog will be putting out more info on the R2k from an earnings perspective, if for nothing else, my own curiosity about the EPS and revenue patterns around the Russell 2000 asset class.

Summary / conclusion: FedEx (FDX), Micron (MU) and Nike (NKE) all report their May ’24 quarters this coming week, which will give us a good look at a cross-section of the US economy. This blog’s Nike earnings preview, was posted last night. While a few analysts expect Nike to benefit from the coming Summer Olympics, the bigger issue might be that the brand has gone stale, and has become relatively dull. This blog’s thesis is laid out in the preview. If consensus estimates don’t change, fiscal ’25 for Nike is expected to see another year of 1% revenue growth, which would be unprecedented. Nike remains about 50% below its November ’21 high, and this blog has bought the stock for clients since it’s “uncorrelated” to this latest rally off the October ’22 lows.

FedEx (FDX) is similar. The transportation giant can benefit from AI, and FedEx is ultimately a higher-operating-margin story.

Micron (MU) too is seeing a sharp increase in the demand for DRAM (dynamic random access memory) as AI-enabled computers require more DRAM to operate efficiently. The stock is not owned for clients directly but through the SMH. This comment will likely get me booed off stage, but it took 23 years for Micron to make a new all-time-high, finally surpassing it’s late summer 2000 high of $99 (before falling back to single digits in 2002 and 2003), in March 2024. In the late 1990’s one hedge fund manager called it an “airline with a fab attached”, which was proven in 2002 and 2003 since returns-on-invested-capital returned to negative numbers. Micron is capable of huge ROIC returns in good markets like today, but I wonder how much it’s truly changed since the nuclear winter for technology which followed after March, 2000. Certainly the NAND business helped diversify the Micron revenue stream, but DRAM is what’s driving the stock these days.

None of this is advice or a recommendation, only an opinion. Past performance is no guarantee of future results. Investing can involve the loss of principal, even over short periods of time. All SP 500 and Russell 2000 EPS and revenue data is sourced from LSEG (www.LSEG.com). Readers should evaluate their comfort level with their portfolio and / or market volatility and adjust accordingly.

Thanks for reading.