FedEx (FDX) reported their fiscal Q4 ’24 earnings results Tuesday night, June 25th, 2024 after the closing bell, and the stock rose $39 or 15% yesterday, June 26th, on heavy volume as FedEx disclosed on page 2 of the earnings release that “FedEx Freight has announced plans to further optimize its operations and match capacity with demand through planned permanent closure of 7 freight facilities…(further on in press release), “FedEx management and the Board of Directors are conducting an assessment of the role of FedEx Freight in the company’s portfolio structure and potential steps to further unlock sustainable shareholder value.”

To keep this summary short and sweet and digestable for clients and readers, here’s a quick summary of the important points in the quarter.

First though, this blog has to apologize for a mistake made in the earnings preview, where I greatly understated the improvement in FedEx’s operating income in fiscal ’24, thanks to erroneously looking at the “expense” progress the last 4 – 6 quarters.

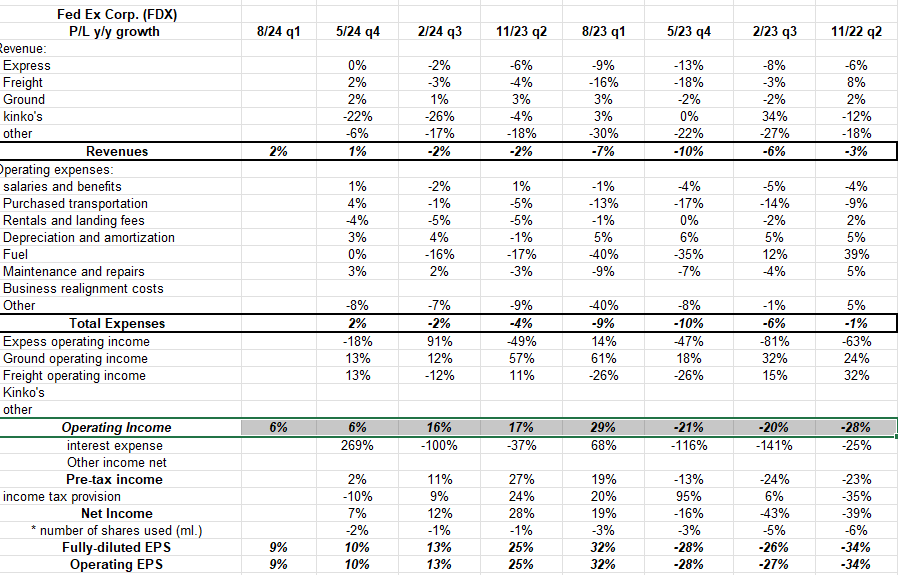

FedEx P/L y-o-y growth

In the preview, y-o-y operating income (3rd blocked or highlighted line) started improving smartly in the August ’23 quarter (fiscal Q1 ’24), and continued through this last quarter, but the expense line was cited erroneously.

The valuation story remains intact:

Here’s the next three years key metrics after revisions post earnings:

- Fiscal ’27 EPS estimate: $26.89, +13% expected growth

- Fiscal ’26 EPS estimate: $23.86, +15% expected growth

- Fiscal ’25 EPS estimate: $20.79, +17% expected growth

- Fiscal ’27 PE: 11x

- Fiscal ’26 PE: 12x

- Fiscal ’25 PE: 14x

- Fiscal ’27 revenue estimate: $99.2 billion, +6% expected growth

- Fiscal ’26 revenue estimate: $93.9 billion, +4% expected growth

- Fiscal ’25 revenue estimate: $89.97 billion, +3% expected growth

Estimate source: LSEG.com (formerly IBES data by Refinitiv)

Even with the 15% jump in stock price on Wednesday, June 26th, the PE remains quite reasonable to expected EPS growth (and I’m not really a fan of the PEG ratio), and price to sales is still below 1.0x at 0.83x after Wednesday’s close.

Free-cash-flow (FCF) has improved dramatically over the last 4 quarters, (trailing-twelve-months or TTM), rising 45% over the last 4 quarters, and 18% over the last 12 quarters.

FCF spiked dramatically during Covid, peaking at $4.25 billion (TTM) in the May ’21 quarter. It ended the May ’24 fiscal year at $3.13 billion.

FedEx still sports a 4% free-cash-flow yield after Wednesday’s 15% increase in stock price.

Here’s a little simple math being done to get to peak EPS for FedEx:

The fiscal 2025 rev estimate is $90 billion times 9% operating margin = $8.1 billion times effective tax rate of 25% (1 – 0.75), equals $6.075 billion divided by 248 million shares outstanding or $24.50 per share. (This is an estimate, not a prediction, and remember this is a full-year EPS estimate). The fiscal 2025 EPs estimate per the above data is currently $20.76, which didn’t change much after FedEx’s conservative guide for ’25.

The FedEx management team is gunning for the 10% operating margin, but 9% was assumed for fiscal ’25.

If FedEx stock trades up to $325, with a $24.50 EPS estimate, it’s still trading at just 13x EPS. That assumes too just a small improvement in the operating margin and no additional shares repurchased.

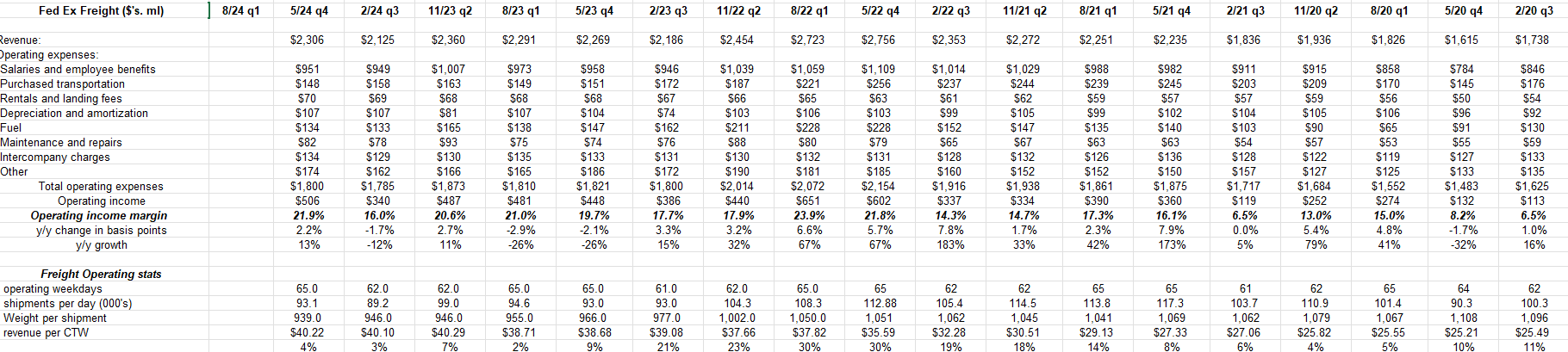

FedEx Freight:

FedEx consolidated guided to $5.2 billion in capex for fiscal ’25, which is exactly where fiscal ’24 came in (i.e. $5.176 billion), but fiscal ’24 was down 16% from fiscal ’23. It’s hard to say if the Freight facility closures are already in fiscal ’25 capex, or perhaps they are not material.

The potential spinning off of Freight is another potential additional catalyst for FedEx stock. Morningstar’s analyst Matt Young didn’t address the Freight divestiture in his comments, only focus on current operations, but Jeffries Stephanie Moore, did say that FedEx Freight could be worth $30 billion, in a sale.

Freight has consistently been 10% – 11% of FedEx’s total revenue but with much higher margins of late after management fixed the issues in the latter part of last decade.

Here’s this blogs internal spreadsheet on Freight’s financial history: note the improvement in operating margin.

If Freight can sustain the operating margin, it may not be a bad time to get rid of the segment.

Summary / conclusion: Like the earnings preview title, which was right on target, I still think FedEx is too cheap but give it some time to consolidate the 15% jump in the stock price yesterday.

Raj Subramaniam’s is still sticking to the 10% operating margin target, but I suspect FedEx will eventually do better than that. Even if Freight is spunoff with it’s 15% – 20% operating margin, (much higher than Ground’s 11% – 12% and Express’s 4% – 5%), the economic logic or the financial logic here is that Freight’s capital-intensity will be jettisoned too.

The expected revenue growth over the next 3 years has returned to positive growth, versus negative y-o-y declines.

As the performance chart on the earnings preview demonstrated, FedEx’s stock price performance has lagged the SP 500 for 5 and 10 year time periods, but the stock has always delivered. Raj Subramaniam, and the FedEx management team have obviously been “greenlit” by the Board and probably Fred Smith too (now Executive Chairman) to take measures to improve returns-on-capital and drive shareholder value (i.e. get the stock price moving) after the fundamentals of the Express business have changed over the years.

Look for slightly higher revenue growth ( a mild recession shouldn’t impact FedEx too greatly at this point), higher EPS on continued margin gains, higher free-cash-flow on lower capex and capital intensity, more capital returned to shareholders in the form of dividends and buybacks, and a more focused and leaner FedEx going forward.

A leaner and more profitable FedEx should result from the changes over the next year or so. I hope FedEx management finds other areas to improve the transport giant.