Oracle (ORCL) the former enterprise software database giant that has had to transition to the cloud in the last 10 – 15 years and is now forced to tackle the AI evolution, is scheduled to report their fiscal Q4 ’24 financial results after the closing bell on Tuesday, June 11, 2024.

Street consensus is expecting $1.65 in EPS in $14.56 billion in revenue for expected yoy growth of -1% and +5% respectively. Operating income is expected to come in at $6.65 billion for expected yoy growth of 8%.

Typically the fiscal 4th quarter is one of Oracle’s strongest quarters of the fiscal year. The software giant really pushes to close business for Q4 ’24.

When Oracle reported their fiscal Q3 ’24 in March ’24, they reported a very strong quarter: revenue rose 7%, operating income grew +12%, and EPS grew +16%. Oracle Cloud Infrastructure (OCI) backlog grew 29% yoy, and the RPO (remaining performance obligation) grew 29% as well to $80 billion.

Fiscal Q3 ’24 was solid for Oracle and the stock jumped sharply after the release.

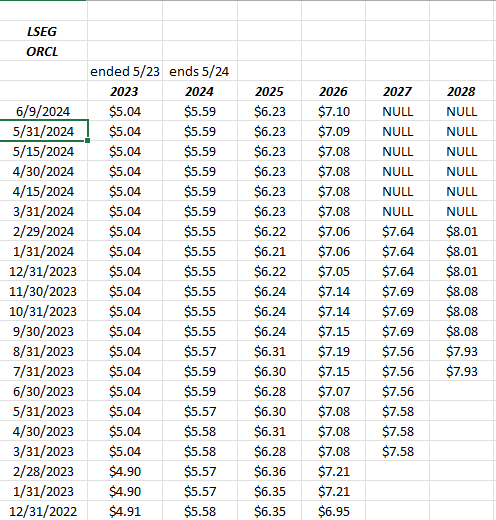

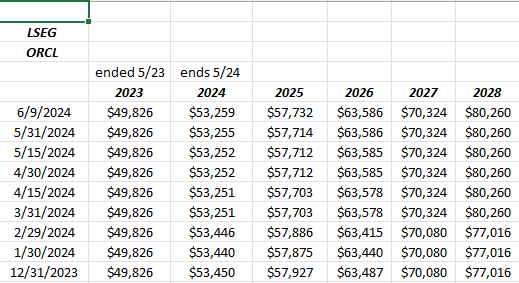

The EPS and revenue revisions continue to be positive:

Note the positive EPS revisions after the March ’24 earnings release.

Revenue revisions are less robust, but part of that might be the Cerner acquisition.

Technical analysis:

An Oracle trade through $130 – $133 would be a break out to a new all-time-high. One thing that’s puzzled me about Oracle over the years is that it’s shown difficulty putting a consistent string of good quarters together as the database business fades, and these new secular trends emerge in the cloud and now AI.

Valuation:

Oracle is trading at 23x and 20x expected ’24 and ’25 EPS of $5.59 and $6.23, for expected growth to finish off ’24 and into ’25 of 9% and 11%.

Currently consensus estimates for fiscal ’25 (began June 1) are expecting EPS growth of 11% and revenue growth of 8%. The current estimates are for $6.23 and $57.7 billion, so let’s see what the guidance is on the conference call after results are released for Q4 ’24.

Oracle is not an expensive stock on a valuation basis, but as an enterprise software vendor trying to find a strategy for AI, the growth is better in Microsoft as you’d expect since Azure and the Intelligent Cloud were both better suited for the cloud than Oracle’s offering.

Summary / conclusion: Just as the cloud did, AI is presenting another opportunity for Oracle to pivot off the cloud and away from their legacy stand-alone database business, and the software giant is doing that. It’s evolve or die for Oracle and they have successfully done that as the legacy database business will continue to grow at lower rates.

Oracle’s biggest challenge is that they remain well behind Amazon’s AWS and Microsoft’s Azure in the secular growth of cloud.

That being said, never bet against Larry Ellison, and even in 3rd place within market share within the technology space, Oracle has always managed to drive growth and returns, even with their dilutive acquisition strategy.

I’ve worried about Oracle’s enormous acquisitions for years since this blog includes the acquisitions in capex which typically crushes free-cash-flow for 4 – 8 quarters, and since these acquisitions are heavily dilutive to Oracle shareholders since Oracle makes big options grant to management of the acquiring companies, and these options get exercised over the next few years of the acquisition, expanding fully-diluted share count.

Morningstar carries a 30% free-cash-flow yield target for Oracle, which I found surprising since the internal valuation spreadsheet of this blog (which calculates the “free-cash-flow yield” as trailing twelve month free-cash-flow divided by Oracle’s market cap), is between 4% – 8% over long periods of time. (This blog’s Oracle spreadsheet goes back to the 1990’s.) Only if Oracle free-cash-flow is divided by revenue, do I get anything close to a 30% FCF yield target.

One final thought for readers: I’ve found over the years, Oracle stock typically peaks between 47% and 50% operating margin. The last three quarters operating margin for Oracle have been 43.6% (2/24 qtr), 42.8% (10/23) and 40.6% (8/23/23 qtr).

The last time Oracle printed a 51% operating margin was 2014, both the stock and the operating margin fell sharply, with the operating margin dropping back to the high 30% – low 40% range, and thus the stock didn’t make a new high again until 2017 when the operating margin returned once again to the low to the mid 40% range.

Oracle is a small position across client accounts with a weight less than 0.5% globally.

What worries me from a bigger picture perspective, is that not all software companies will thrive under AI, in fact AI integration and implementation, may hasten the demise of many.