It was only after posting last week’s SP 500 earnings update that it was realized that the data metrics usually posted each week were left off last weeks blog post. Here’s last weeks SP 500 data:

- The forward 4-quarter estimate was $252.21 up $0.40 from the prior weeks $251.81;

- The PE ratio on the forward estimate last week was 19.7x

- The SP 500 earnings yield ended the week above 5% – 5.08% to be exact – for the first time since January 19th;

SP 500 data (this latest week):

- The forward 4-quarter estimate this week was $252.55, up from $252.51 last week;

- Assuming a close in the SP 500 today around 5,100, the PE ratio on the forward estimate is 20.2x

- Assuming a 5,100 close, the SP 500 earnings yield will fall back under 5% to 4.95% this week;

- The Q1 ’24 bottom-up SP 500 estimate rose to $54.42 from $53.74 last week;

- More importantly, with 233 SP 500 companies having reported, the “upside surprise” for EPS was 9.5% for this quarter, significantly stronger than the pretty strong three previous quarters, but let see if it tempers next week, when more than half the SP 500 will have reported;

- The upside revenue surprise was 1.3% though this week, also stronger than the last 2 quarters;

Again, the unusual pattern to speak of is the steadily higher sequential revisions since the start of April ’24:

- 4/25/24: $252.55 (mega-caps start reporting)

- 4/19/24: $252.21 (financial sector reports)

- 4/12/24: $251.81

- 4/05/24: $251.58 (the quarterly bump)

- 3/31/24: $242.94

Things looked pretty normal last week, except for the higher revisions and now we’ve seen 5 consecutive weeks of sequentially higher estimates.

SP 500 earnings are pretty strong, with just under half the index reporting.

Normally the sequential revisions are negative.

What’s the forward quarterly patterns look like ?

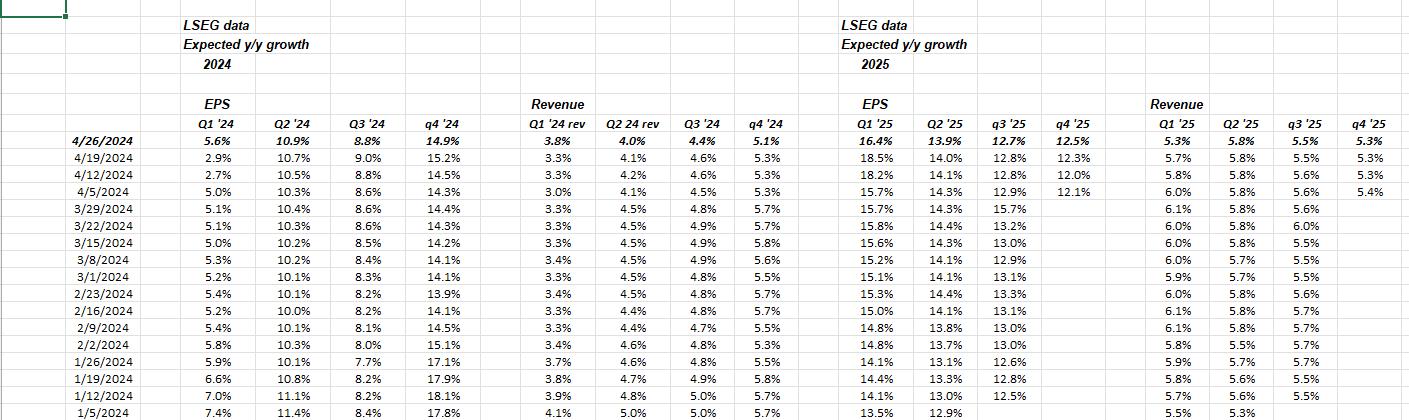

Click on the above spreadsheet and note the expected growth for Q1 ’24 SP 500 EPS:

- This week: +5.6%

- One week ago: +2.9%

- Two weeks ago: +2.7% (that was the low for the quarter)

This same pattern referenced in last weeks blog post is playing out again almost exactly as expected.

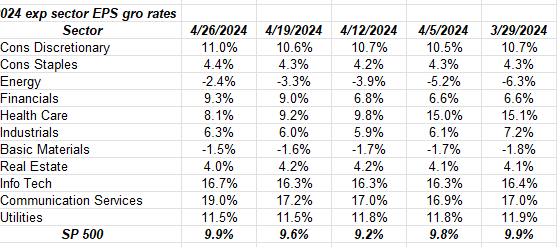

If you look at the above table, the financial sector is showing the biggest expected change in full-year ’24 EPS growth, jumping from 6% to 9%.

Industrials and health care have suffered the biggest downside.

Technology is stable, but that numbers should be higher by the end of next week. Remember, last night’s Microsoft and Google earnings reports won’t be in the data till next week.

Remember none of this is advice or a recommendation. Past performance is no guarantee of future results. Investing can involve loss of principal even over short periods of time. All SP 500 EPS and revenue data is sourced from LSEG. Readers should gauge their own comfort with portfolio volatility and adjust accordingly.

Summary / conclusion: Frankly, the SP 500 EPS data continues to look pretty good. Next week, we get Amazon, Apple, Starbuck’s, Coca-Cola, Pfizer, Coinbase, and a many, many others. 175 companies will report in total next week.

Inflation, and the bond market(s) were two good reasons for stocks to buckle, but the earnings are still healthy. The SP 500 rose 2.7% this week, after falling roughly 3% last week.

High-yield spreads have suddenly gotten volatile: 3 weeks ago corporate high yield credit (on average) was trading +310 over Treasuries, but last week it jumped to +342, and then this week, high yield credit spreads tightened to +319.

The high yield bond market is your early-warning credit indicator.

Thanks for reading.