FedEx (FDX) reports their fiscal Q3 ’24 tonight, March 21 ’24 after the closing bell.

Analyst consensus:

- Revenue: $22 bl or -1% expected yoy revenue growth

- Operating Inc: $1.285 or 10% yoy operating income growth

- EPS: $3.49 or 2% yoy operating income growth

Expected Q4 ’23 analyst consensus:

- Revenue: $22.4 billion for expected revenue growth of 2%

- Operating Income growth: $1.9 billion or 8% yoy expected growth

- EPS: $5.45 or 10% expected yoy growth

If tonight’s actual revenue is $22 billion, FedEx will have reported 7 consecutive quarters of negative y/y growth. EPS growth has been relatively robust the last 2 quarters despite negative revenue growth, printing, 32% in fiscal q1 ’24 and 25% in fiscal q2 ’24.

Last quarter, FDX saw some Express issues with a change in strategy by USPS, which apparently cost FDX Express some revenue. The intersting aspect to last quarter was that revenue fell 2% yoy, while FDX operating income rose 17%, and EPS rose 25%. That’s exactly the kind of operating leverage FedEx needs, but I think it’s more that FDX is still coming out of the post-Covid environment rather than implementing the “FedEx One” consolidation announced in early April ’23.

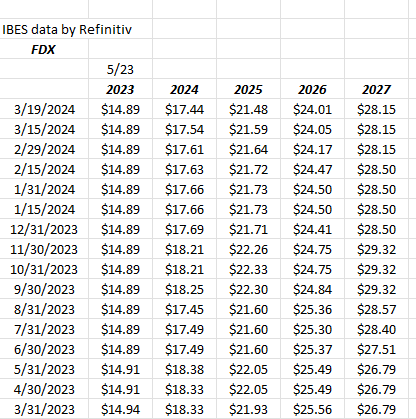

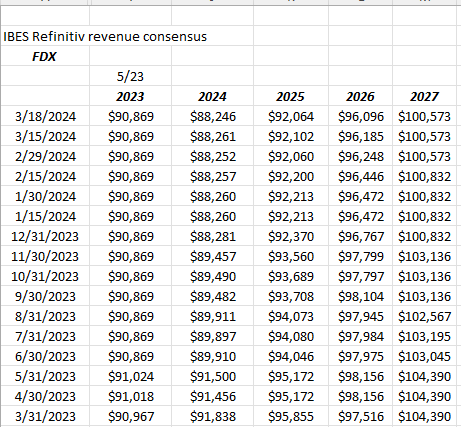

FDX EPS and revenue estimate trends:

The fiscal ’24 EPS estimate has fallen 5% in the last 12 months, while the fiscal ’25 EPS estimate has fallen just 2%.

The fiscal ’24 revenue estimate has fallen 4% in the last year, while ’25’s revenue estimate is also lower by 4%.

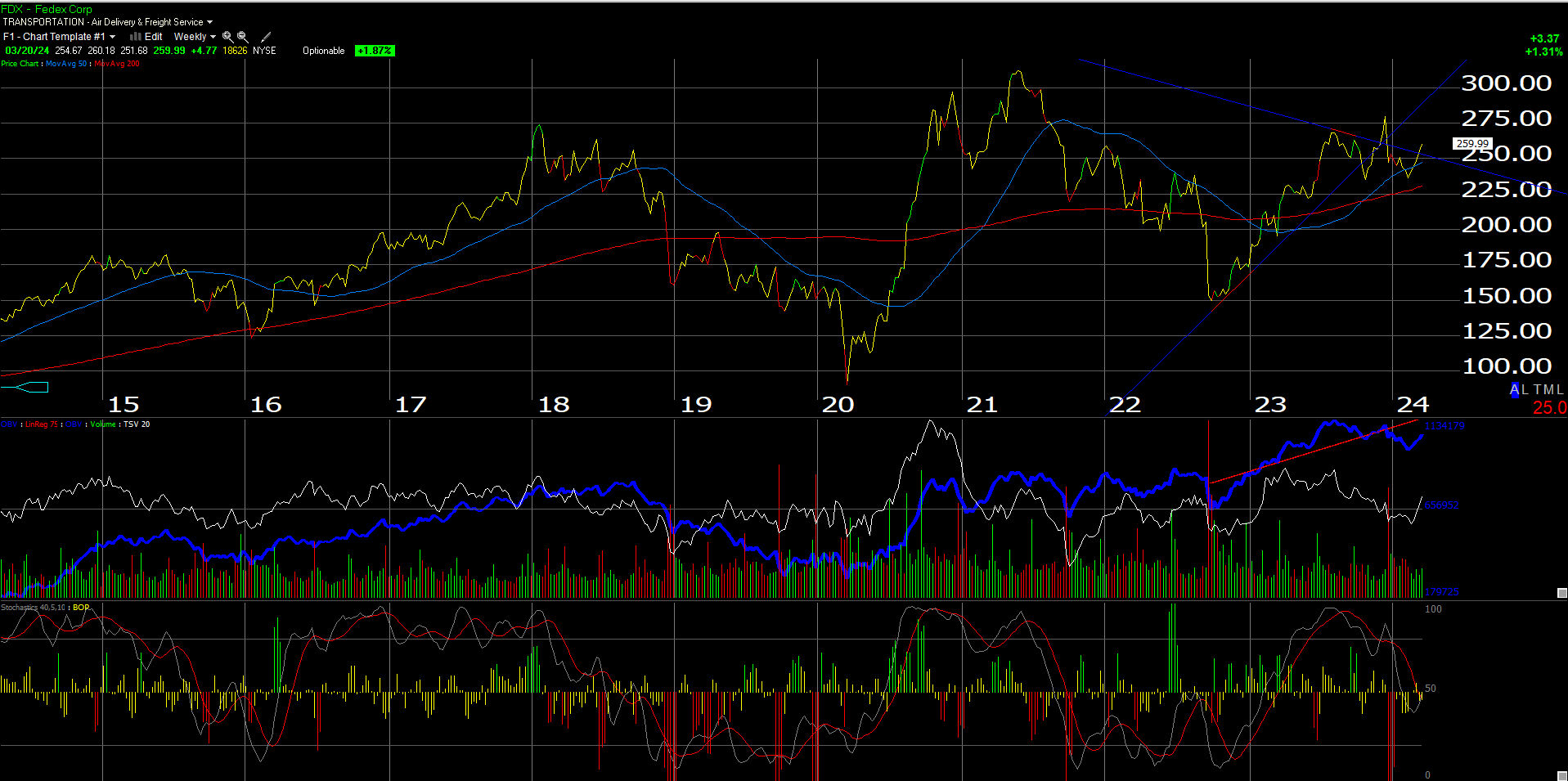

The chart:

FDX recently moved back above it’s 50 and 200-day moving averages, which is technically a plus.

I’d still like the stock trade above the all-time-high of $317 from June ’21. That all-time-high was driven by the “stay-at-home” frenzy around the pandemic and the need for quick delivery of consumer goods.

Valuation: FDX is still cheap on a GARP basis, trading at an average PE of 12x for an expected average, 3-year growth of 17%. Expected EPS growth in ’24 and ’25 as of today – per the consensus estimates – 16%, 23% and 12% respectively.

Still, the most compelling valuation historically is price-to-sales, or price-to-revenue. Historically FedEx stock has peaked with a 1x price to sales and 10% operating margin and we’re still short of those metrics at 0.75x price-to-sales and an operating margin last quarter of 6.3%.

Summary / conclusion:

From a bigger picture perspective, I believe it was McKinsey that has put out a study in the last few months, that talked about the biggest sector beneficiaries of AI “productivity” improvement, and those sectors were:

- Travel

- Retail

- Airfreight and logistics

FedEx falls in the third category and Raj Subramaniam has been out ahead of downsizing or rationalizing the FedEx expense structure since early April ’23, when Raj announced the “FedEx One” initiative, which is expected to drive FedEx’s operating margin to the 10% area. (Here is the December ’23 earnings preview for FDX and here in June ’23 for fiscal May ’23’s quarter.

After May ’24’s fiscal Q4, FedEx is going to consolidate their quarterly reporting to show “one” FedEx segment, which contains Express, Ground, and Freight.

That’s probably not a bad idea, but while Raj is targeting a 10% operating margin, I suspect investors will expect 10% to be the floor going.

As this blog has written about repeatedly over the years, (Most of the earnings previews are over on Seeking Alpha), if not on this blog, FedEx’s achilles heel has been “Express” which while comprising 45% to 55% of FEDX’s revenue, could never “lever” their operating income growth. It’s clear that with the retirement of Fred Smith, Raj may have the ability to “rationalize” the Express cost structure and improve segment returns.

Despite Amazon seemingly moving into FDX’s Ground business, Ground has been a stellar performer for FDX with the exception of the occasional quarter. Ground – comprising 35% – 39% of FDX revenue, has been able to “lever” Ground revenue and produce much higher operating income growth for a given level of Ground revenue growth.

Despite the business buzzwords, basically Raj Subramaniam and the FedEx management team have to continue to shrink the cost structure and drive revenue growth, which will ultimately help the operating margin, but that’s easier said than done. Will AI be a help on this ? Probably but investors are dependent on management to tell us how.

In a decent global economy it does worry me a little that FedEx revenue estimates have been seeing lower revisions.

Ultimately, the real tell for FDX will be what happens to the operating margin.

Clients have a long position in FDX that comprises roughly 2% of total assets.