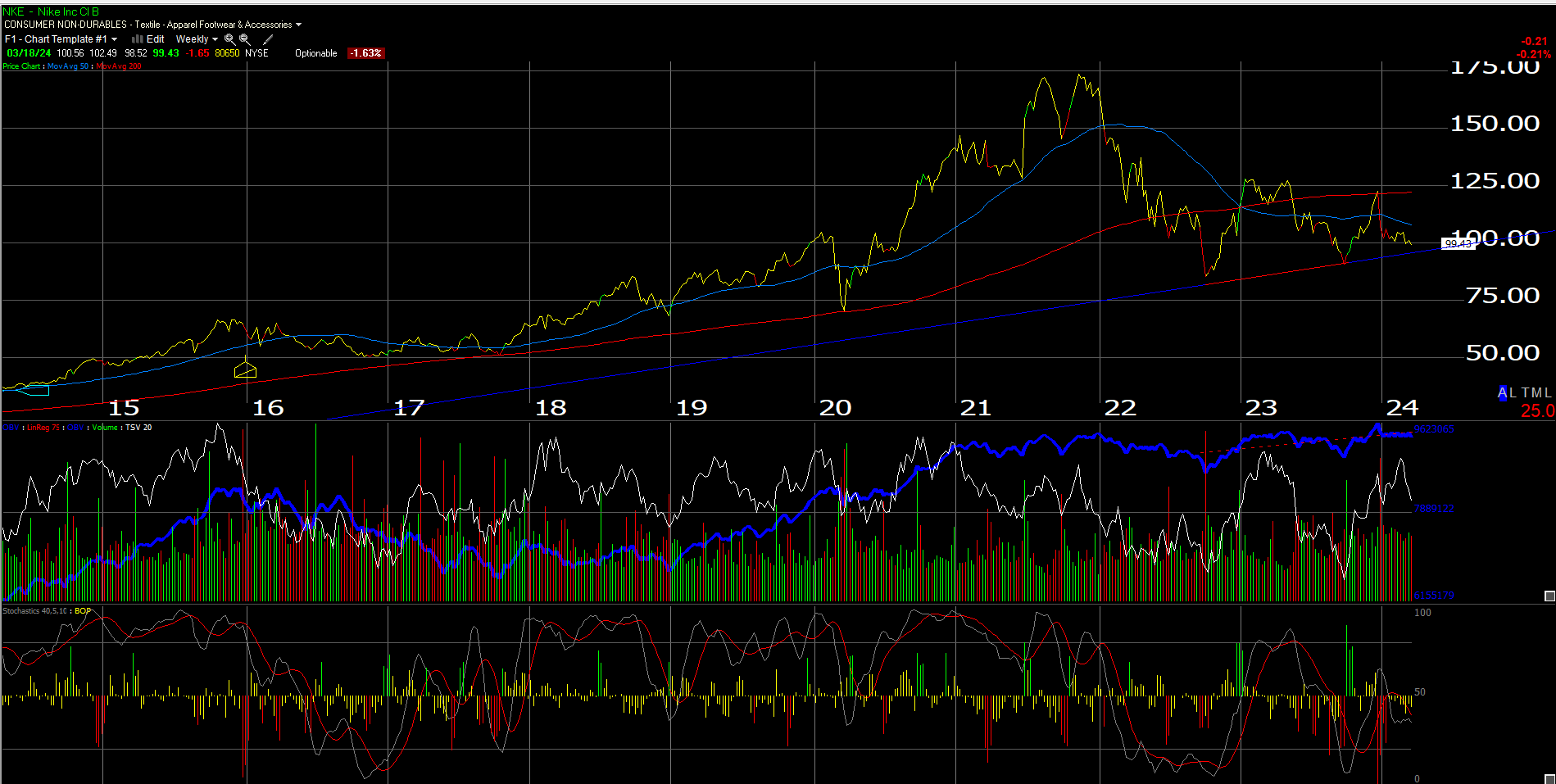

After hitting an all-time-high in November ’21 at $179.10, Nike has had a tough 2.5 years as the stock is still down almost 45% from that all-time-high.

Here’s a weekly chart for readers:

The problems are well known by now. Last quarter in fiscal Q2 ’24, Nike lowered revenue guidance from an expected +4% to just 1% annual growth. At one time, as of February ’22, the sell-side consensus was expecting 11% revenue growth for the shoe and apparel giant in fiscal ’24. Nike did announce $2 billion in expected cost savings over the next two fiscal years, and margins were much better in the November ’23 quarter as both gross and operating margins grew 170 bp’s yoy in the November ’23 quarter.

When Nike reports Thursday night, March 21st after the closing bell, street consensus is expecting:

Q’3 ’24 consensus estimates:

- Rev: $12.28 billion for -1% yoy rev growth;

- Op Inc: $1.3 billion for -7% yoy op inc growth;

- EPS: $0.74 for -6% EPS growth;

Q4 ’24 consensus estimates:

- Revenue: $13 billion for 2% yoy revenue growth;

- Op inc: $1.6 billion for 29% yoy operating income growth;

- EPS: $0.87 for yoy EPS growth of 32%;

What most readers may not realize is that Nike went through the same issues with inventory that plagued Amazon, Walmart, and so many other large retailers in ’22 and ’23.

Let’s take a look at Nike’s revenue-to-inventory growth for the last 16 quarters:

![]()

Source: valuation spreadsheet

If readers would click on the spreadsheet, you’ll see that prior to the pandemic Nike routinely grew revenue faster than inventory. That’s a sign of a healthy merchandiser. Then the pandemic hit, and while Nike survived the pandemic, (note the quarters from 2/22 through 2/23), the outsized inventory growth that occurred at Nike, resulted in free-cash-flow being significantly reduced for all 4 of those quarters (not shown). Like any retailer, when inventory gums up the balance sheet, cash-flow suffers.

It’s just in the last 3 quarters that Nike’s revenue growth has returned to normal, relative to it’s inventory growth.

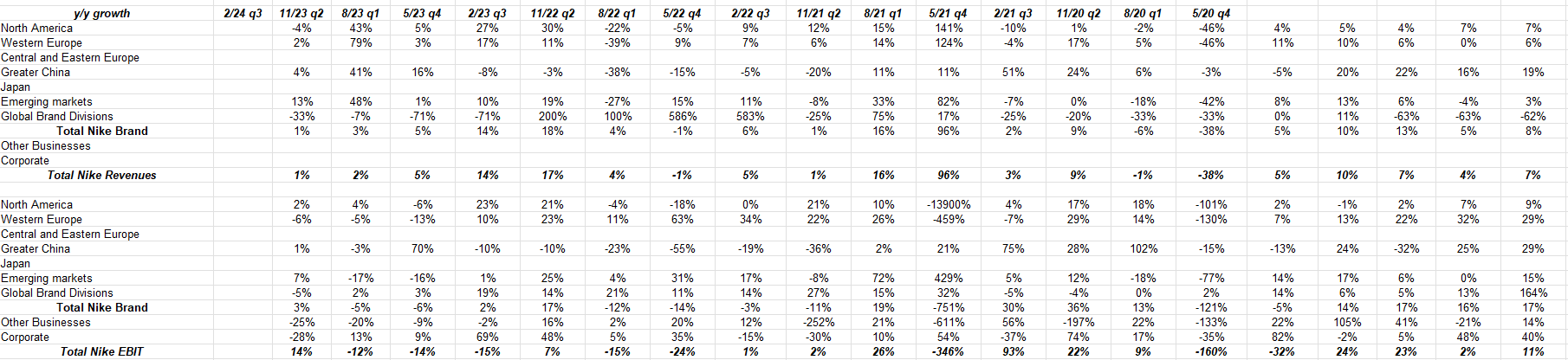

Regional analysis of Nike’s business:

Source: Nike earnings reports and internal valuation spreadsheet

North America is 40% – 45% of total Nike revenue, and roughly 80% of Nike EBIT (It’s puzzling why Nike continues to use EBIT and not operating income, but Nike also doesn’t report their cash-flow statement with quarterly results, which a considerable portion of the SP 500 now do with quarterly earnings results. Nike still requires you to wait for the 10-Q and 10-k to get cash-flow information.)

While the China segment gets a lot of press when Nike reports, since Morningstar considers China Nike’s most profitable segment, what fascinates me is that when China report positive yoy revenue growth, China’s EBIT is “levered” to that revenue, meaning, that China’s EBIT growth is typically more than that positive revenue growth, but when the yoy China revenue is negative, that levering works the opposite and the EBIT decline is worse than the revenue decline.

China is important to Nike.

Ed Yardeni recently put out a chart (can’t access) which shows how Nike, Starbucks, Apple and Tesla are feeling the “China syndrome” so to speak, which is the current trade and technology spat that China and the US are experiencing. (The China Syndrome was a 1979 movie.) There is no question China has the ability to influence the Chinese consumer, to a far greater degree than the US government over the US consumer, and that’s a risk to the stock.

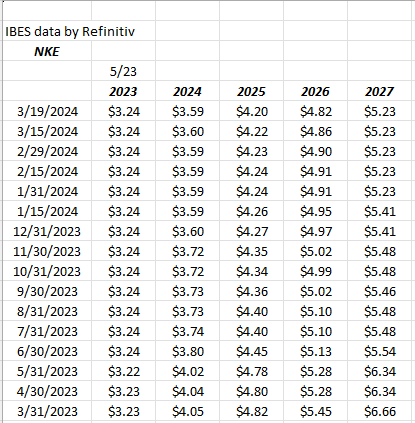

Nike EPS estimate trend:

NKE’s fiscal ’24 EPS estimate has declined 11% in the last year, while the fiscal ’25 EPS estimate has fallen 13%, and ’26 has fallen 12%.

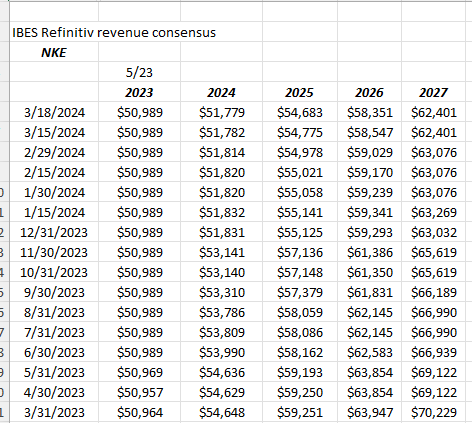

Nike Revenue Trend:

’24 rev est decline, 5%; ’25 rev est decline, 8%; ’26 rev est decline 9%

Valuation:

At roughly $100 per share, Nike is trading about 24x the next three years EPS, which is expected to “average” 14% – 15% over the next 3 years. at 2.5x revenue (12-month trailing or TTM) and 20x cash-flow (ex cash) and 24x free-cash, both TTM, Nike isn’t really cheap, but the valuation metrics are 50% of what the stock was trading for at it’s peak in November ’21.

This make perfects sense since Nike is down 45% from it’s all-time-high of $179 – $180.

One metric that jumped out on the valuation spreadsheet is that Nike is sporting a free-cash-flow yield of about 4%, the first time that metric has been hit since May, 2019. No question, Nike’s free-cash-flow has been improving, the TTM FCF as of the November ’23 quarter was $6.3 billion, and I believe that’s a record from TTM perspective.

Technically, the multi-year low for Nike was $82 and change in early October ’22. Any trade below that and you’d have to figure Nike is broken.

Morningstar assigns a fair value on Nike of $136, while the internal model values Nike between $85 and $100, but the model incorporates EPS estimates, which are still falling.

Summary / conclusion: The last time Nike went through a multi-year consolidation like this was the “brown-shoe” craze in the late 1990’s and after re-configuring Nike’s supply chain, the stock bottomed in the early 2000’s and never looked back. Is China a problem today ? Well, it’s certainly not a positive, even with the growth of the NBA in China.

Stock positives;

- Inventory has improved for 3 straight quarters, and revenue to inventory is now back to normal;

- Nike faces a very easy compare in Q4 ’24, which is the current quarter;

- The improvement in free-cash-flow is quite healthy and is consistent with the inventory improvement;

Stock negatives:

1.) EPS and revenue estimate trends are not good. Something has to stop that bleeding. Is it all China and Non-US – maybe not.

6 weeks ago, i went shopping for running shoes in the western burb’s of Chicago and wanted to buy a pair of Nike’s but wound up buying two pairs of Hoka’s instead. The sales folks at Dick’s told me there were no Nike’s in my size, (which is 9 – 9.5, so fairly normal) but what struck me was that they seemed to have little interest in selling me Nike. That left an impression. They didn’t offer an alternative Nike style or offer any kind of reasonable Nike substitute.

Anecdotal evidence is to be taken for what’s it’s worth, but you can’t help but wonder if the brand is losing a little of it’s luster, much like Apple has.

Clients are long the stock, but it’s still a 1% position. Technically, it could be building a longer base in this area between $80 – $100, but what’s more important is to see (at least) stable EPS and revenue estimates, and eventually improving estimates. If China’s a more serious problem, maybe management needs to address the issue specifically with investors.