SP 500 data:

- The forward 4-quarter estimate (FFQE) saw it’s quarterly bump this week, with the FFQE jumping to $230.26 from last week’s $224.01.

- With the flat market this week, and the increase in the FFQE, the SP 500’s PE fell from 20x to 19x;

- The SP 500 earnings yield jumped to 5.23% from last week’s 5.03%;

- The Q2 ’23 quarterly bottom-up EPS estimate is between $52.80 and $52.90.

In terms of interesting datapoints that can’t seem to be explained, last week’s (what was thought to be the final bottom-up EPS estimate for Q1 ’23) was $53.09, but this week that number had been revised higher to $54.83 or roughly a $1.74 higher revision, without an explanation. Have to check that with the IBES / Refinitiv staff. That’s a big revision – after the fact – and it also means the EPS “upside surprise” was higher than the reported +6.8% as of June 30 ’23.

The point is with that revision Q1 ’23 EPS looks even stronger than originally thought.

Financial sector:

Financials always lead off earnings season and Q2 ’23 will be no exception with the larger-cap financial names kicking off SP 500 earnings next week. On Friday, July 14th, 2023, BlackRock (BLK), CitiGroup (C), JP Morgan (JPM), State Street (STT), and Wells Fargo (WFC) all will report their Q2 ’23 financial results before the opening bell.

Bank of America (BAC), Charles Schwab (SCHW), Morgan Stanley (MS) as well as Goldman Sachs (GS) will follow early the next week of July 17th, reporting on Tuesday morning, July 18th, before the opening bell.

Thursday night, posted on this blog, was how well financial sector earnings have held up this year despite higher interest rates and the regional bank issues.

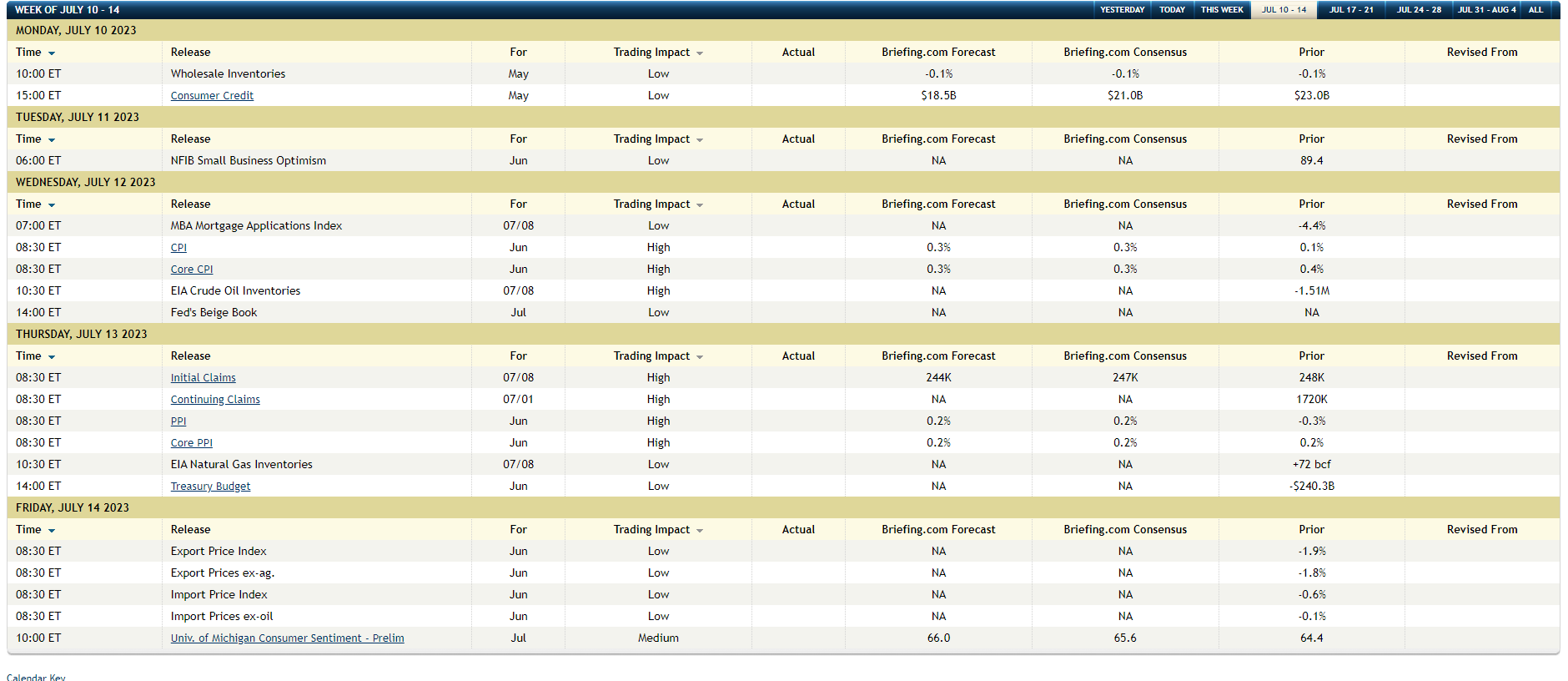

Economic Data:

No question, with this coming week’s economic data, CPI and in particular Core CPI will take center stage.

If overall CPI comes in at +0.3% or lower, it means that month-over-month gain in the CPI will fall below 3% t0 2.95%.

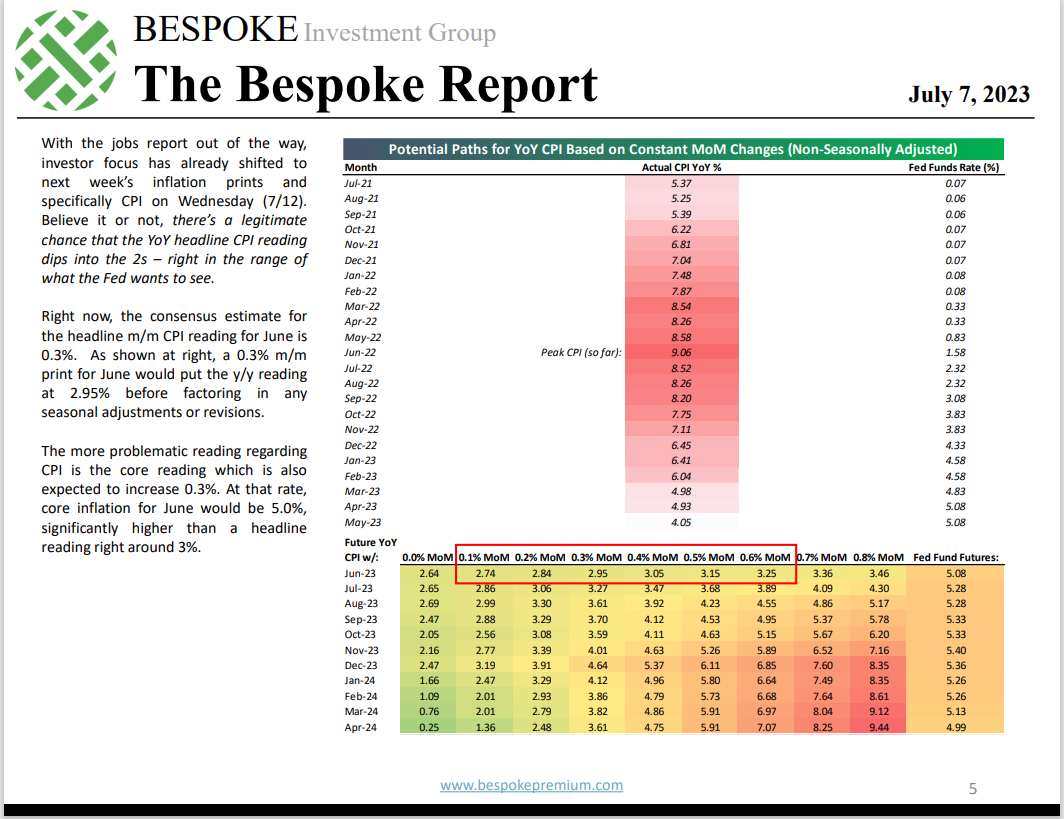

Bespoke puts out a great table on CPI data – have a look:

The aspect of the Bespoke CPI preview I like (and Bespoke has published this in the past) is that Bespoke calculates the CPI run rates at various levels of monthly change. (Yellow section at the bottom of the above page.)

Bespoke is calling Core CPI “more problematic” which likely means it’s going to be a little hotter than overall CPI, and remain more elevated.

Conclusion / summary: The original intent was to write more over the July 4th weekend, but it never happened. There is more color that can be added to the coming Q2 ’23 SP 500 earnings season, and hopefully it will be gotten to over the coming days.

Talking to a technician, the energy sector had a nice bounce on Friday, July 7th, accompanied by good volume in the larger-cap energy stocks, like Schlumberger (SLB), Exxon-Mobil (XOM), Conoco-Phillips (COP), etc. Energy faces very tough comp’s in terms of earnings and revenue growth from Q2 ’22, which gradually gets better as we move into the 2nd half of 2023 (again, comparing 2023 quarterly results, versus the same period in 2022).

The expected tech sector earnings and revenue growth hasn’t changed much since the beginning of the year, which is a tad worrisome, given how the YTD returns on mega-cap growth stocks in the first half of 2023.

More to come this weekend.

Take all of this as one person’s opinion. None of this is advice and past performance is no guarantee of future of results. Investing in the capital markets can result in loss of principal. All SP 500 EPS and revenue data is sourced from IBES data by Refinitiv. This data and the opinions therein may or may not be updated and if there is an update, it may not necessarily be in a timely fashion. Readers should gauge their own sensitivity to market volatility and adjust accordingly.

Thanks for reading.