If you look at the YTD return for the Financial ETF (XLF) as of June 30 ’23, the -0.50% return might seem like a fair trade given the rising interest rates, inverted yield curve, and Silicon Valley Bank (SIVB) debacle this year.

However looking at expected financial sector EPS growth, the numbers don’t look nearly as grim as some of the price action. Here’s a brief look at what’s expected from the sector, as well as some historical numbers:

- Q1 ’24: +5.2% expected EPS growth;

- Q4 ’23: +11.4% expected EPS growth;

- Q3 ’23: +14.5% expected EPS growth;

- Q2 ’23: +8.4% expected EPS growth, +7.1% expected revenue growth;

- Q1 ’23: +7.7% actual EPS growth, +10.8% actual revenue growth;

- Q4 ’22: +8.9% actual EPS growth, +6.6% actual revenue growth;

- Q3 ’22: -16.4% EPS decline, +7.8% actual revenue growth;

- Q2 ’22: -19.3% EPS decline, -1.6% revenue decline;

- Q1 ’22: -17.1% EPS decline, +2.2% revenue decline;

- Q4 ’21: +9.9% EPS growth, -4% revenue decline;

- Q3 ’21: +34.9% EPS growth, +4% revenue growth;

- Q2 ’21: +158% EPS growth, +6% revenue growth;

- Q1 ’21: +138% EPS growth, +33% revenue growth (thanks to very weak comp’s vs Q1 ’20)

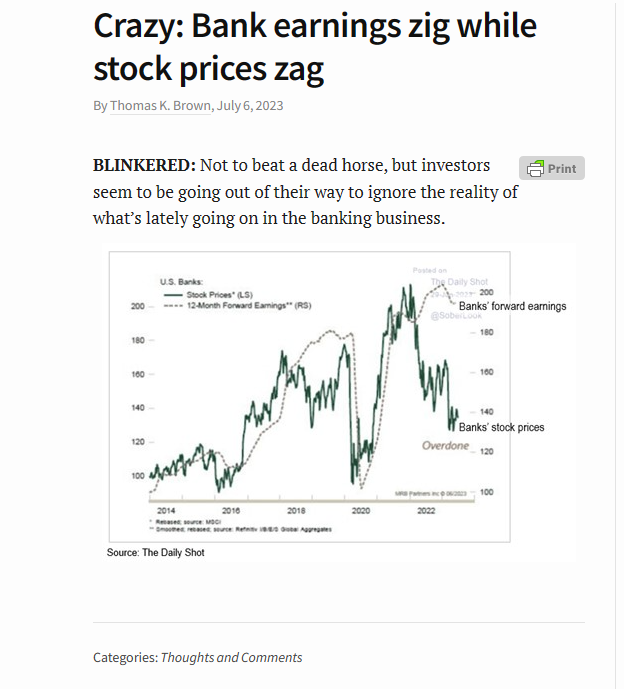

Summary / conclusion: With this weekend’s blog post, it was pointed out how the financial sector EPS and revenue growth looked pretty healthy, despite the stock price action, and then Tom Brown, over on Bankstocks.com, came out with this blog post on Thursday, July 6th, 2023 noting the graphical difference between the bank stocks and bank earnings:

Tom is a great analyst. I remember during the 1990’s bank merger craze he went after Hugh McColl at Nationsbank pretty aggressively, on his acquisitions led by goodwill and other suspect metrics, thinking Hugh substantially over-paid for Nationsbank’s empire building. I can’t recall if Tom was employed at an investment bank at that time, but you had to admire his grit and independence to criticize what seemed at the time to be enormously popular deals.

What’s been an enormous influence on financial sector earnings was Covid and the pandemic and the ZIRP (zero interest rate policy) policy of 2020 to 2021, and now the financial sector is adjusting to this.

For the financial sector net interest income was higher than expected in the last few quarters, (a positive) while the still-solid economy is not yet adding to loan loss reserves, (another positive) but the fact is until investors get some visibility into a normally-sloped yield curve, rather than this brazilian jiu jitsu, rear-naked choke being applied to financials thanks to the inverted yield curve, the sector may not rally smartly. In addition to the capital-market sensitive banks, like JP Morgan (JPM), Goldman, (GS), Citigroup (C), and others, the sharp rise in interest rates has curtailed bond issuance, and while the IPO market is slowly re-opening, it’s been slow for 18 months now.

The financial sector actually faces very easy comp’s in Q2 and Q3 of ’23 (looking at last year’s EPS and revenue growth).

Financial sector earnings actually look better than tech sector earnings.

Think about that.

Take all this as one person’s opinion. Past performance is no guarantee of future results, and all SP 500 EPS and revenue data is sourced from IBES data by Refinitiv. None of this should be construed as advice. This information may or may not be updated, and if it is updated, it may not be updated in a timely fashion. Investing can involve the loss of principal. Each reader should gauge their own appetite for market volatility, and act accordingly.

Thanks for reading.