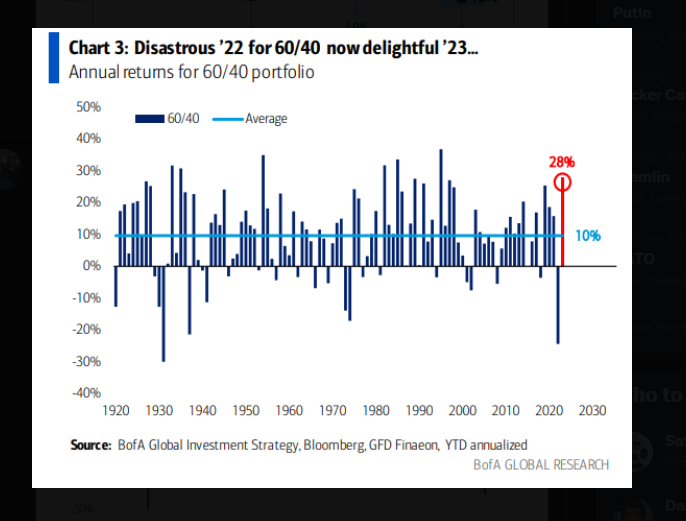

The 60% / 40% balanced portfolio as of June 23, 2023:

- SP 500: +14.14% YTD return

- Barclay’s AGG: +2.58% YTD return

- 60% / 40% balanced YTD return: +9.52%

- (Morningstar return data)

Sourcing a chart from Twitter’s @MikeZaccardi (Twitter) and Bank of America’s research shows that 2023’s YTD balanced portfolio return is right in line with the historical average of 10%.

Still, it all from the equity market. Bonds are contributing very little to 2023’s +9.5% YTD return.

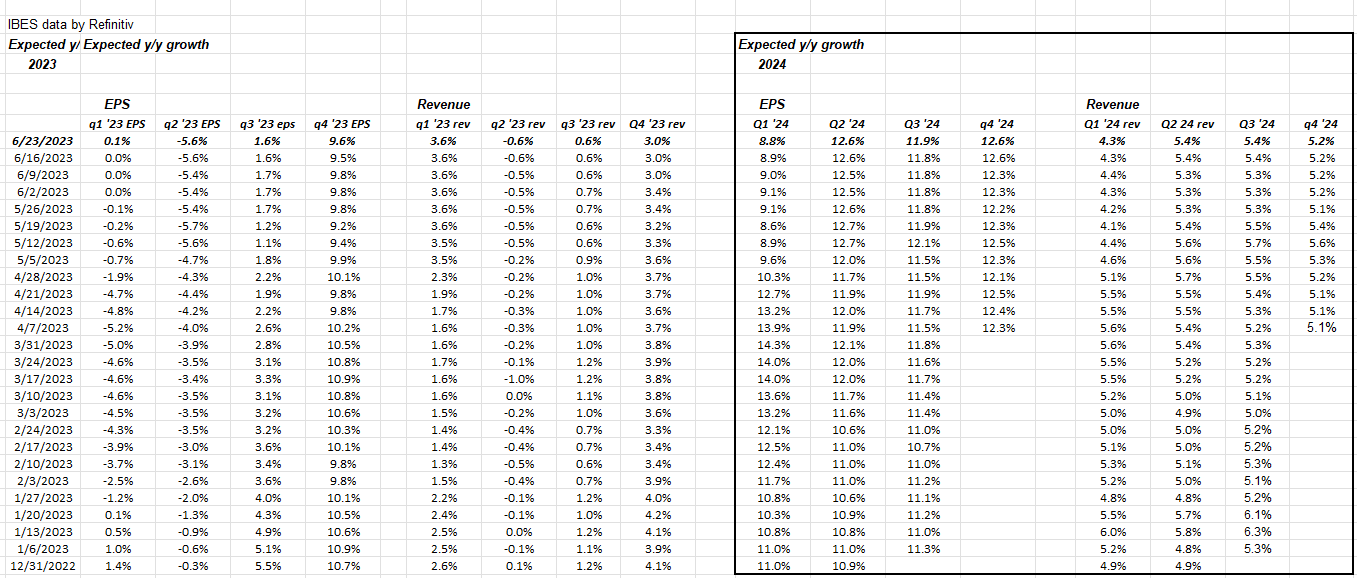

2024 SP 500 EPS:

Is it too early to look at 2024 SP 500 EPS estimates ? Well, yes and no. There are 6 months remaining in 2023, thus if you believe the stock market is a discounting mechanism, that discounts into the future by a 6 – 9 month window, then you are paying attention to 2024 EPS and revenue estimates, and the fascinating thing about the 2024 estimate trends, is that Q2 – Q4 ’24 are showing no degradation or negative revisions off the starting expected growth rates, which is unusual for the forward estimates.

That’s worth watching. Also Q4 ’23’s EPS growth rate is showing remarkable stability, even though Q4 ’23 expected revenue growth is degrading a little.

Readers can laugh and make jokes, the pattern is what is important, not necessarily the absolute growth rates, although that does matter.

This post from January ’23 notes the same pattern, highlighted almost 6 months ago.

This bodes well for “expected, future, returns” for the SP 500, buy maybe not for lower Treasury yields. Stronger earnings, and higher stock prices, will keep the FOMC focused on the inflation data.

SP 500 data:

- The forward 4-quarter estimate to $224.33 from last week’s $225.06.

- The PE ratio on the SP 500 this week is 19.4x

- The SP 500 earnings yield rose a little this week, to 5.16%, from last week’s 5.10%;

Walgreens (WBA), Micron Technology (MU), and Nike (NKE), report this coming week. This blog will likely have earnings previews out for Walgreens and Nike over on www.seekingalpha.com, and possibly Micron if there is time.

Summary / conclusion: The May ’23 PCE and Core PCE data is scheduled to be released before the market opens on Friday, June 30 ’23, and that is closely watched data by Jay Powell and the FOMC.

Even the Markit manufacturing and services PMI data released Friday’s June 23, is that the manufacturing data continues to show that the US manufacturing sector is now in decline, while “services” continues to show decent growth.

![]()

This data – cut-and-pasted from Briefing.com’s economic calendar shows the forecasts for PCE and Core PCE data for May, to be released this coming Friday morning, June 30. Note the prior numbers and the expectations: readers can see while overall PCE will or is expected to decline markedly, core PCE is being more stubborn.

Durable goods and GDP are also out this coming week, but the PCE data is still the most important (in my opinion).

Take all of this as one person’s opinion. All EPS and revenue growth expectations are sourced from IBES data from Refinitiv. Past performance is no indication of future results. None of this is advice, and this data may or may not be updated, and if updated, may not be done in a timely fashion. Capital market can change quickly for both the good and bad: readers should gauge their own appetite or risk for market volatility.

Thanks for reading.