May ’23 still has 2 days remaining but here’s the basis point change in Treasuries (as of Friday, May 26) since 4/30/23:

- 3-month: 24 bp increase

- 1-year: 45 bp increase

- 2-year: 50 bp increase

- 5-year: 41 bp increase

- 10-year: 36 bp increase

- 30-year: 29 bp increase

Looks like we are seeing a nice rally in the 10-year on Tuesday morning, post Memorial Day weekend, so there was some “debt ceiling” worries built into yields, but judging by the fed funds futures referenced this weekend here, you have to think the greater worry about the US consumer strength and inflation not disinflating fast enough, are bigger worries.

Let’s see where Treasury yields end the week.

Here’s a data point tracked every week, that readers might enjoy: the traditional 60% / 40% portfolio has definitely felt a drag from the bond side of the equation:

60% / 40% YTD return by week:

- 5/26: 6.79% (SP 500 +10.25%, Barclay’s Agg, +1.60%)

- 5/19: 6.79% (SP 500, +9.89% AGG, +2.13%)

- 5/12: 6.22% (SP 500, +8.04%, AGG, +3.49%)

- 5/5: 6.49% (SP 500 +8.31%, AGG, +3.76%)

- 4/28: 7.04% (SP 500, +9.18%, AGG, +3.82%)

- 4/21: 6.12%, (SP 500 +8.2%, AGG, 3.00%)

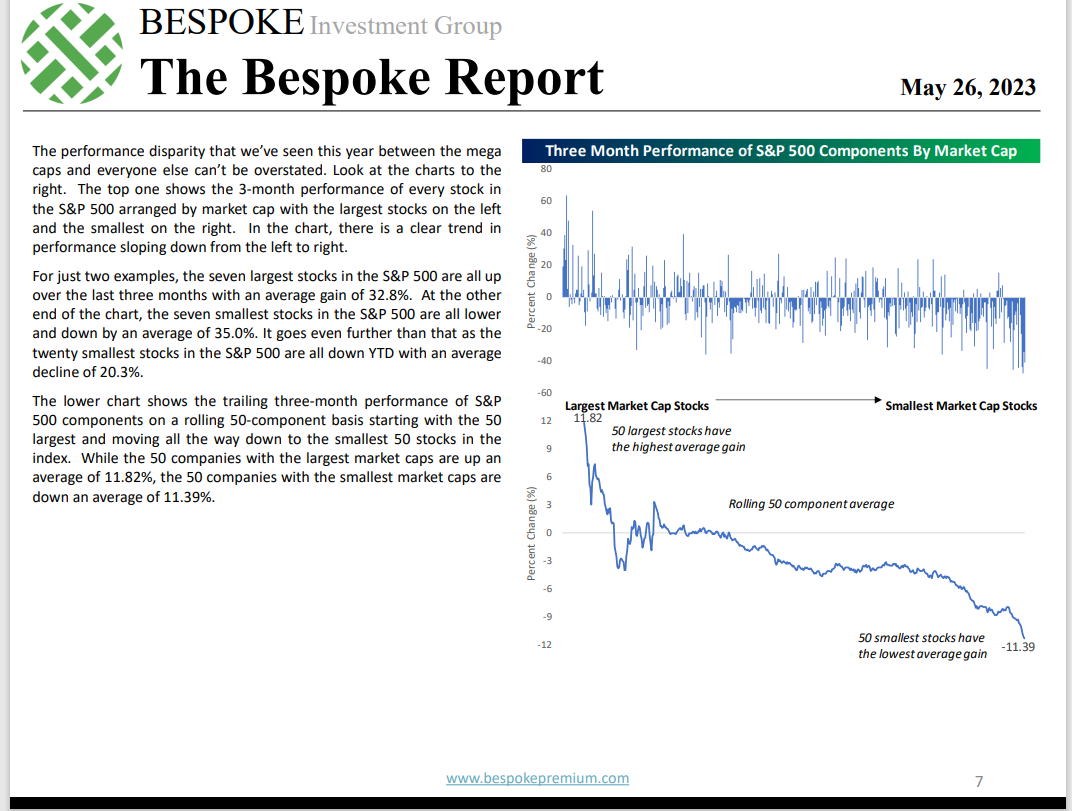

Technology and the narrow SP 500 leadership in 2023:

Rather than re-write history, Bespoke covered the topic perfectly this weekend. Here’s their two charts:

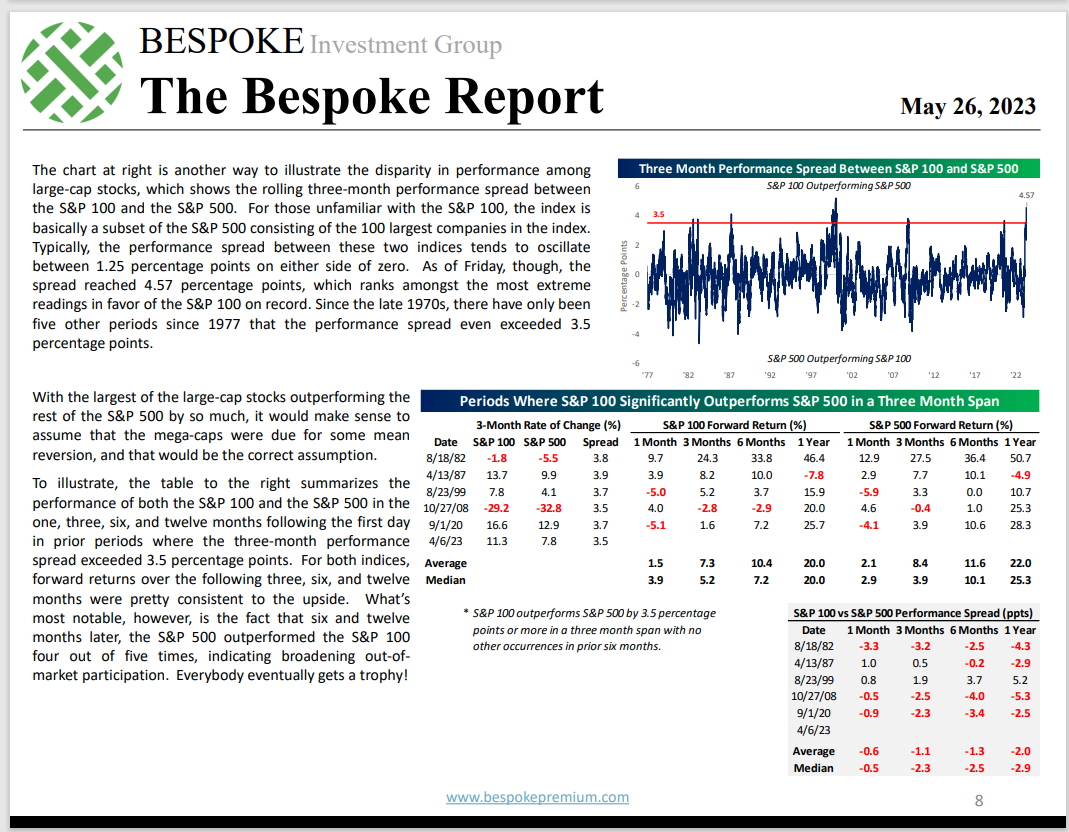

The first Bespoke page cut-and-pasted from this weekend’s Bespoke Report shows the performance of the largest 30 stocks in the SP 500, versus the smallest 30 stocks, (wow, what a disparity) and the 2nd page shows why readers may NOT want to necessarily bet on “mean reversion” anytime soon.

All the crap published from Wall Street and that shows up in the financial media week after week, I’m amazed that Bespoke doesn’t get more coverage for their research. They certainly deserve it.

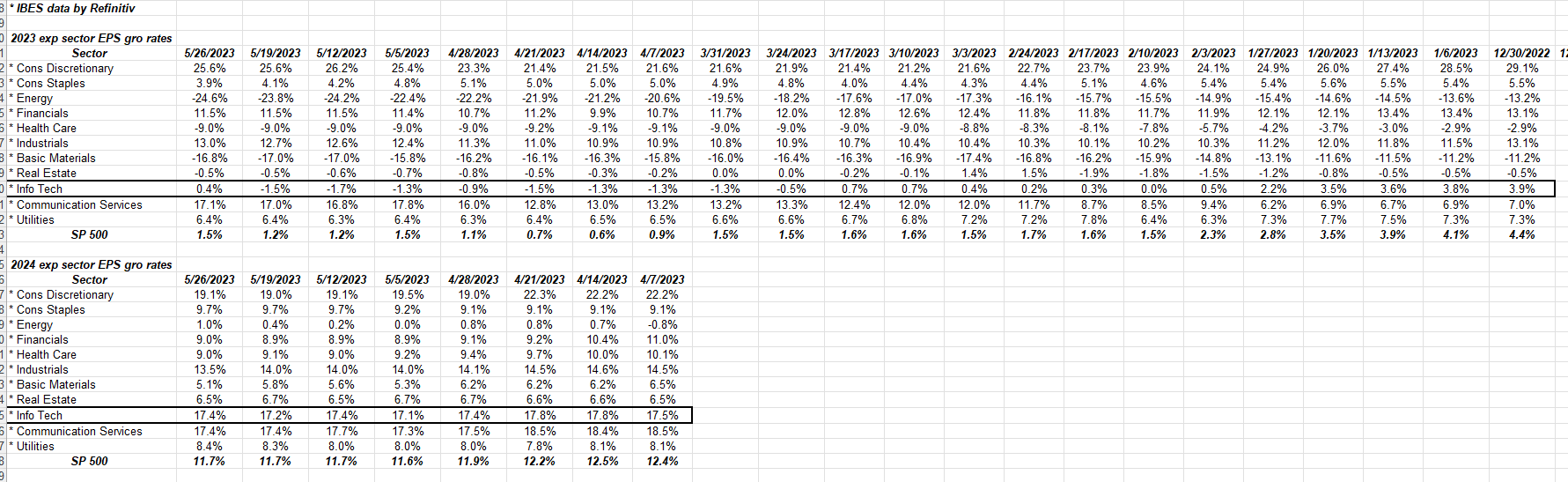

However here’s this blogs caveat around “tech leadership” at this point in 2023:

Click on the above spreadsheet and note how Tech sector EPS growth has changed in 2023. Expected tech sector EPS growth remains pretty punk for 2023, even after Nvidia’s earnings last week. However note 2024’s expected growth. How far in the future does the stock market really discount?

Click on the above spreadsheet and note how Tech sector EPS growth has changed in 2023. Expected tech sector EPS growth remains pretty punk for 2023, even after Nvidia’s earnings last week. However note 2024’s expected growth. How far in the future does the stock market really discount?

Really, I expected to see a bump in expected tech sector EPS growth in 2023 after Nvidia’s whopping upside guidance.

Typically technology as a sector does better when semiconductors are a leadership group, and semi’s are leading once again in 2023. The SMH is up 45% YTD as of Friday, May 26th. Of course, Nvidia is the largest weight in the SMH ETF at 17.7% of the market cap of the SMH.

This blog post was written on March 25th noting the same dynamic and still tech moves forward.

Eight weeks later, little has changed.

Summary / conclusion: It’s one opinion, but if Treasury yields cooperate, you can make a case for more upside for the SP 500, even with a decent return YTD already. Some are comparing the current market with the late 1990’s, which a case can be made for, while others are making a case for a repeat of 1995, where technology exploded with the Netscape IPO and the beginning of the dot.com boom (AI being the new thing in 2023).

The other aspect in 2022, it was clear high PE growth stocks would NOT take higher rates well, and the Nasdaq corrected 30% in 2022. Even with little help from interest rates in 2023 (normally a “PE compressing” event) and no earnings growth expected, technology, and in particular mega-cap top 10 of the SP 500 continue to outperform.

None of this is advice and take it all with a substantial grain of salt. All earnings data is sourced from IBES data by Refinitiv, and earnings and revenue estimates can change daily. Past performance is no guarantee of future results, and investing can involve loss of principal. Take all market opinions with substantial skepticism. Capital markets change quickly, both positively and negatively.

As always, thanks for reading.