JP Morgan’s Investment Forum in Oak Brook, Illinois, this past week saw Dr. David Kelly kick it off with his always-entertaining and spirited look at the US economy and the capital markets. David’s key points:

- 1.) Inflation will come down and flatline in the 2nd half of 2023;

- 2.) The Fed will begin cutting the fed funds rate by mid-2023;

- 3.) The US economy will likely not fall off a cliff, like 2008, or like Covid in March, 2020, but instead the US economic progression will be analogous to a “slow slog” through a swamp;

- 4.) The SP 500 could see earnings fall 10% – 15% in 2023;

The 4th bullet point caught me off guard a little bit, since the SP 500’s forward 4-quarter estimate, has been deteriorating slowly since July 1 ’22, but has not dropped off a cliff so to speak.

Here’s the catch, though.

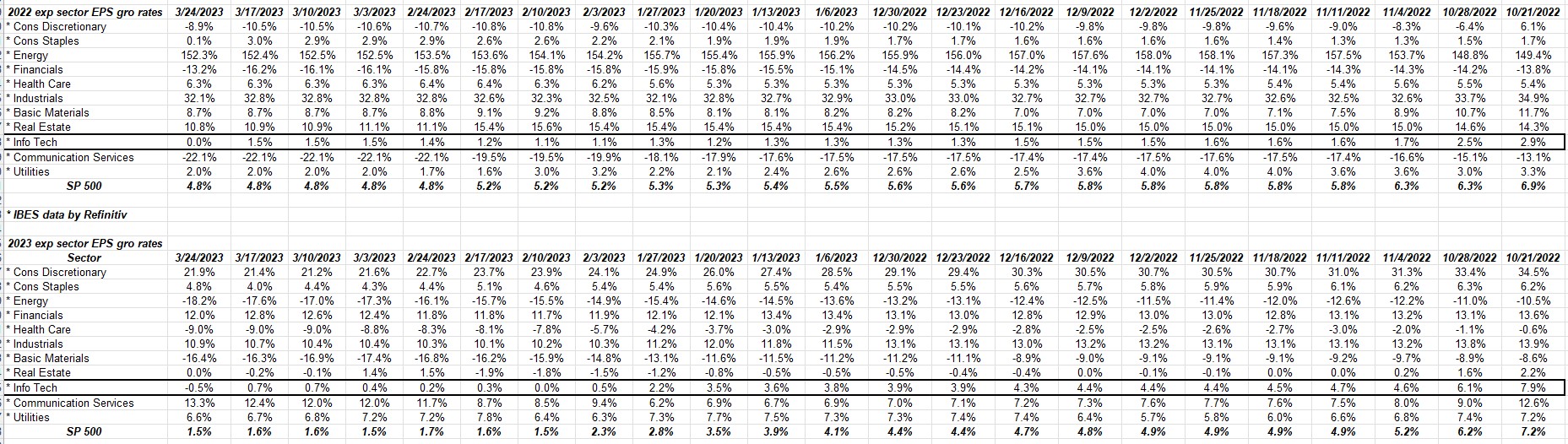

Technology earnings:

The above data is IBES data by Refinitiv’s tables from a section of the “This Week in Earnings” report published every Friday.

By transcribing the numbers onto the spreadsheet, it allows me to look at various time periods and also track the data rather than simply reading it from a report.

The black-bordered lines are the technology sector’s actual and expected earnings growth from/for 2022 and 2023. 2024 numbers will be published in the next week or two since the Q4 ’22 earnings season ends next week, with March 31.

Now, note 2023’s “expected” technology sector earnings growth versus the fact the Nasdaq 100 (QQQ) is up 16.93% YTD as of 3/24/23. Another fun fact is that the VanEck semiconductor ETF (SMH) is up 25.47% YTD.

Now consider that relative strength against the sector’s expected earnings growth.

One of the two is wrong, and not by a little.

Reread the title of this article again: something will have to give.

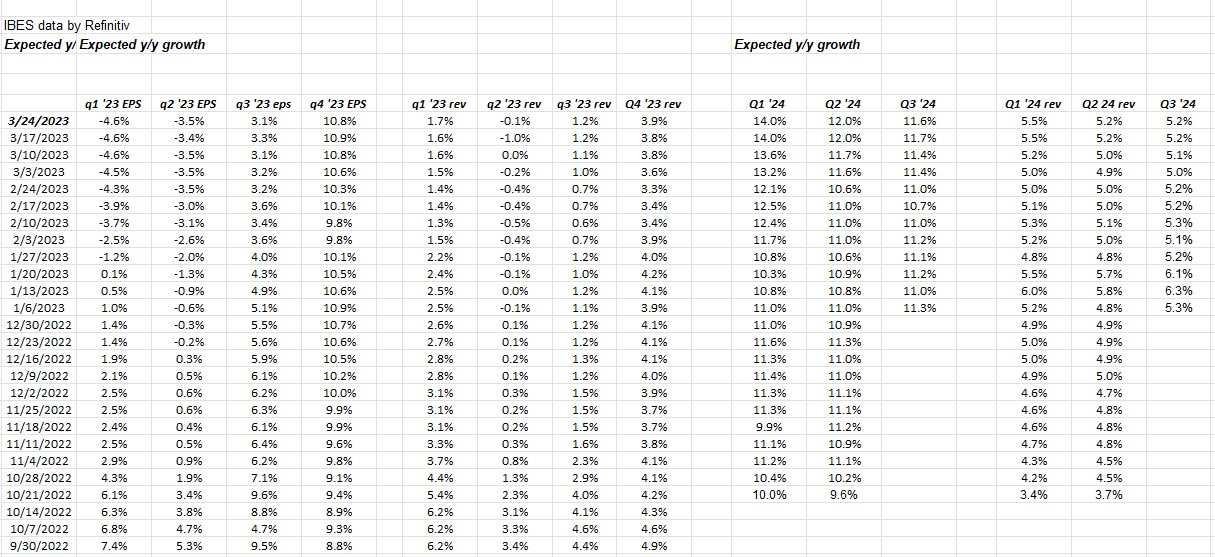

Looking at quarterly, bottom-up expected growth rates for the SP 500 for 2023:

This table is compiled from the IBES data by Refinitiv “Earnings Scorecard”. The first section shows that the first three quarters of 2023, are expected to be weaker at least through the 3rd quarter of ’23, but then look at that 4th quarter.

The 4th quarter of ’23 shows that revenue and EPS estimates chronologically have shown no negative downside revisions, even going back as far as September ’22.

That’s the kind of strength I like to look for in an uncertain market.

Don’t bet the farm on it, but it’s a positive sign in the light of what is a sea of negative earnings revisions the last 9 months.

Summary / conclusion: The unspoken elephant in the room that has been masked by the bank crisis, is the technology sector’s relative strength, while forward earnings look flat at best as of today.

2022’s final EPS of $220 – $222, would mean we’d see a $200 EPS for the SP 500 in calendar 2023 if David Kelly is right.

What’s interesting to me is that software was the first technology sub-sector that rolled over beginning in Q4 ’21, but now Salesforce and Adobe have both reported good quarters, although both stocks remain below their 200-week moving average. Companies like Meta (META) and even Amazon (AMZN) have seen the stock price respond positively to reductions in headcount and payroll, which is a very different response than we saw in 2001 – 2002.

This coming week we get Micron (MU), the DRAM and NAND producer, so we get an update on the semiconductor business, although Nvidia and AMD have bounced nicely, and are 19% – 20% of the market cap of the SMH, being 2 of the top three weights in the semi ETF.

While everyone’s focused on the bank crisis, the real market tell this year might be technology sector earnings, and it’s gone completely under the radar.

Either technology sector’s earnings will support ’23’s relative strength or the SP 500 may have a bigger problem than the banks. Remember, the tech sector’s market cap is still 25% of the SP 500’s capitalization.

No predictions are being made either. Q1 ’23 earnings season will support tech’s relative strength in ’23, or tell us who is swimming naked as Mr. Buffett would say.

More to follow tomorrow for blog readers.

Take everything you read here with substantial skepticism. Past performance is no guarantee of future results. This blog represents my own opinions, and they can change quickly and the information may not be updated in a timely fashion, if at all.

Thanks for reading.