The ghost of Jerome Powell’s mid-December ’22 post-FOMC presser continued to linger this week, as the 10-year Treasury yield jumped from 3.48% as of 12/16/22 to today’s (12/23/22) 3.75% closing yield. That’s a 27 basis point increase on the week and is one reason that stocks struggled, despite what turned out to be positive stock reactions from FedEx (FDX), Nike (NKE) and even Micron’s (MU) earnings reports.

The 3.75% 10-year Treasury yield close for this week, is the highest since the week of November 18th’s weekly close of 3.82%.

Looking back at the 1980’s and 1990’s “real” returns on Treasuries are typically 2% or 200 bp’s, so if Jerome Powell and the FOMC want to return the inflation rate to 2% permanently, that means a 3.50% Treasury yield is still too rich and the “equilibrium” 10-year Treasury yield is closer to 4%.

SP 500 data:

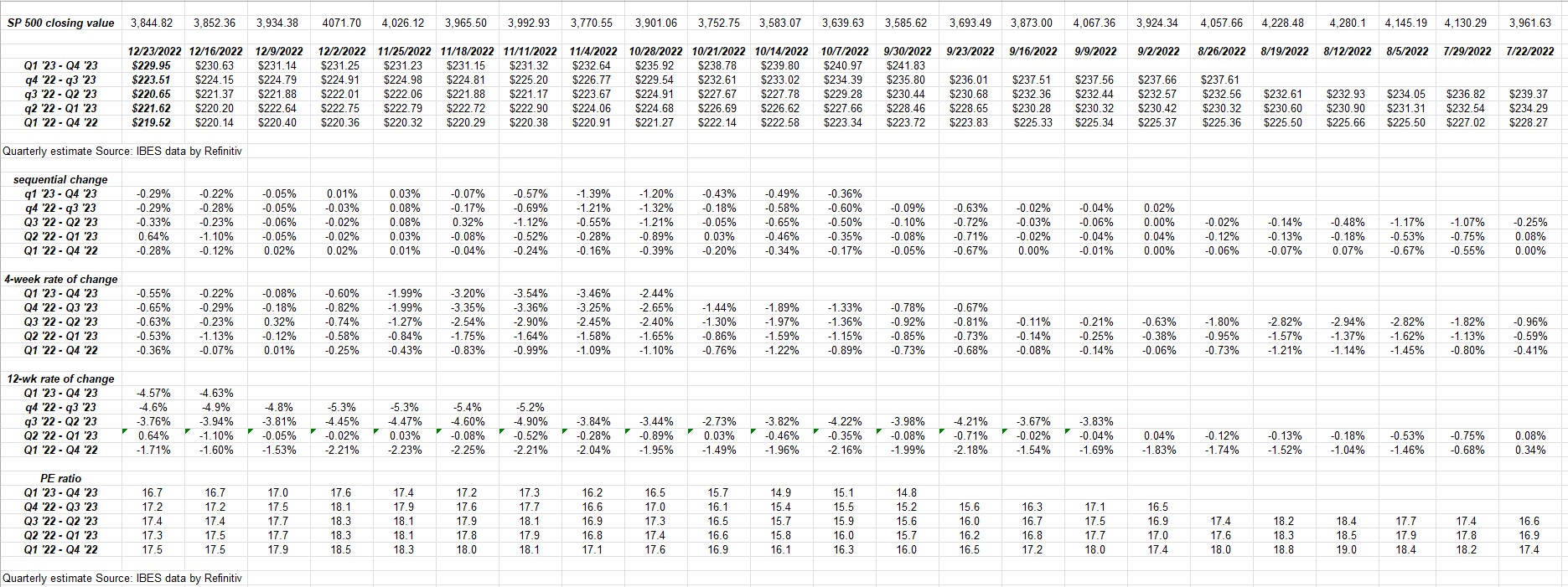

- The forward 4-quarter estimate (FFQE) ended this week at $223.31 versus last week’s $224.15 for a sequential decline of 37 bp’s;

- The PE ratio to end the week is 17.2x vs last week’s 17.2x;

- The SP 500 earnings yield this week 5.81% vs last week’s 5.82% and versus June 30th’s 6%;

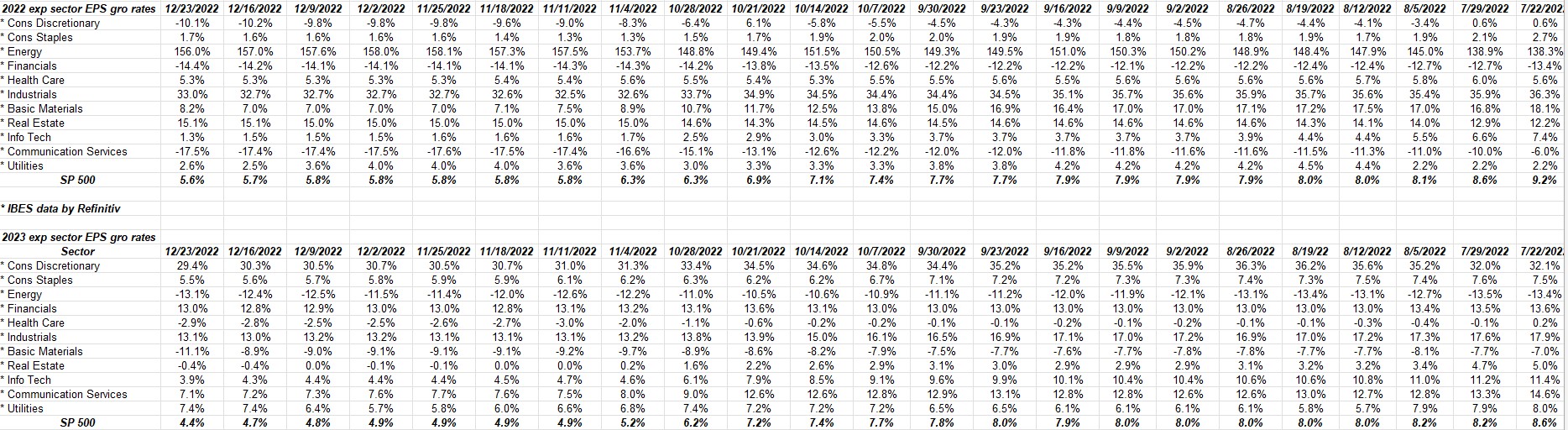

- Looking at calendar year 2022 and 2023 SP 500 EPS estimates, the expected EPS growth rates for both years have now been cut in half from 10% this summer to 5% currently. (Click on the following spreadsheet to show what this looks chronologically);

Looking at 2022 and 2023 SP 500 sector growth rates:

Using the IBES data by Refinitiv tables, readers can see how the expected sector growth rates have changed since this summer.

2023’s expected growth rates, will be adjusted again when Q4 ’22 earnings are reported and companies give full-year calendar year guidance for 2023.

Sectors expected to show better EPS growth in 2023 vs 2022:

- Consumer Discretionary (biggest sector weights are Tesla and Amazon, which have had a tough year in 2022);

- Consumer Staples

- Financials

- Technology (a small increase in growth is expected in 2023, given current estimated growth rates)

- Communication Services

- Utilities

These sectors comprise 65% of the current SP 500 market cap.

What’s interesting is that the Industrial sector, which we told readers one year ago that the current growth rate projections showed that Industrials would have the highest growth of any sector in 2022 (and in fact that was the case, with the exception of Energy) is still expected to growth 13% in 2023, still well above the 2023 SP 500’s expected EPS growth of 4.4%.

But Industrials are expected to slow from 2022’s 33% growth rate to 2023’s 13%.

SP 500 Forward EPS Curve and “rates-of-change”:

The sequential and 4-week rates of change for the SP 500 forward EPS have slowed considerably, but the 12-week rate-of-change is still seeing sharp negative revisions.

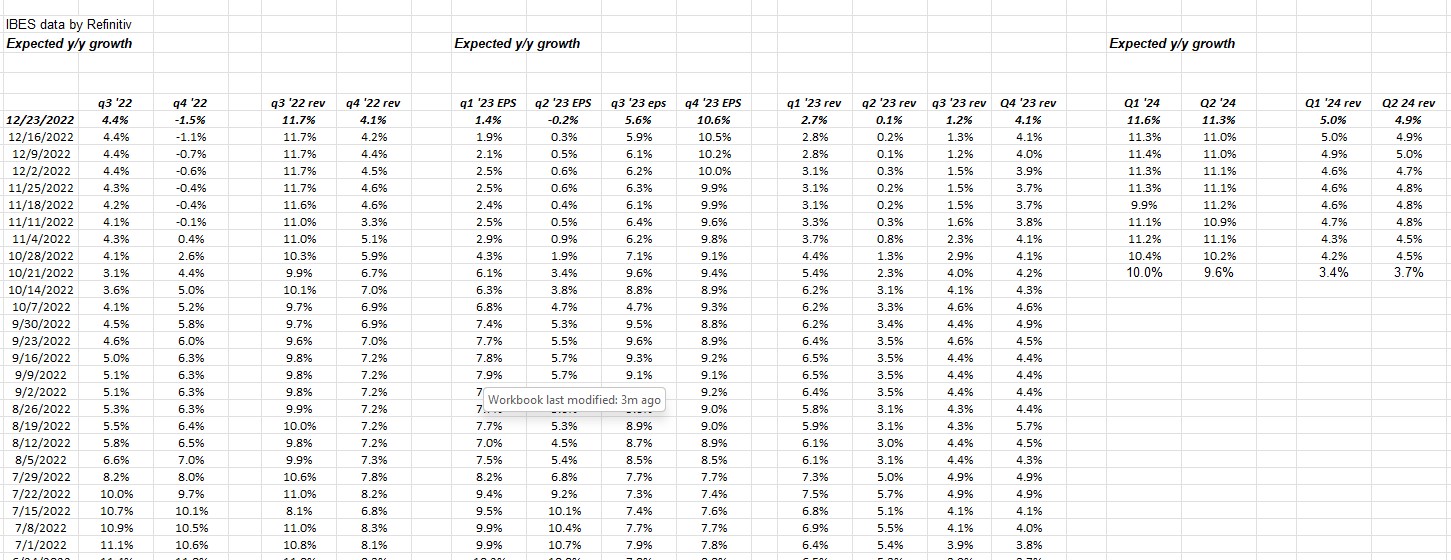

Here’s a pattern worth noting: SP 500 EPS expected to bottom in 2nd half 2023:

Expand this spreadsheet table and note the trends in Q1 ’23 and Q2 ’23 EPS and then note the trends in Q3’23 and Q4’23 in SP 500 EPS.

It’s clear that Q3 ’23 EPS has seen its decelerating growth rates start to slow, and more importantly, the Q4 ’23 expected EPS growth rate has been gradually increasing.

You’re not hearing that in the financial news media.

I’ll be more convinced when 2023 full-year guidance continues the same pattern as Q4 ’22 earnings get reported.

Summary / conclusion: This blog post “buried the lede” with the last bullet point, which has been mentioned in the SP 500 earnings update the last weeks, but it’s getting clearer from SP 500 earnings patterns and weekly revisions, that the gradual erosion or slowing in the SP 500 forward EPS is expected to slow or reverse sometime in the middle of 2023. In fact Q4 ’23 expected, SP 500 EPS growth rate revisions have been positive (ie. higher expected growth rates) since October 1 ’22.

That’s how the data looks now – we’ll see what the revisions look like when Q4 ’22 earnings results are reported and 2023 guidance is given by corporate managements.

The big jump in the 10-year Treasury yield this week took that yield up to 3.75%. Anything below 3.50% and the SP 500 starts trading very well, anything above 4% and the opposite is likely to occur.

Take all opinions here with a substantial dose of skepticism, and evaluate in light of your own risk / reward. Past performance is no guarantee of future results. All the earnings data is sourced from IBES data by Refinitiv, but the spreadsheet work is solely the work of this blogger. Capital markets change quickly, both positively and negatively.

It’s a long holiday weekend with much year-end writing to be done. Expect more blog posts over the weekend.

Thanks for reading.