This blog’s primary source of earnings data is IBES data by Refinitiv, and to remind readers the Apple and Amazon earnings releases from Thursday night and the earnings releases from Exxon Mobil (XOM) and Chevron (CVX) from Friday morning, are not in the following data. It’s expected that the updates early next week from Refinitiv will give us a good read on that data, which should be a positive influence on SP 500 EPS and revenue revisions, at least for Q3 ’22. Remember, there is a difference between “market-cap weight” and “earnings weight” within the SP 500. A company like Tesla (TSLA) has a big market-cap influence on the SP 500, but not really an earnings influence. Apple has both, but Exxon (XOM) and Chevron (CVX) have a much bigger earnings weight influence than a market-cap influence today since energy is just 5% of the SP 500 by market cap, although Chevron and Exxon have been moving up the market-cap continuum. (Here’s a September 30th update on SP 500 market-cap weight vs SP 500 earnings weight list.)

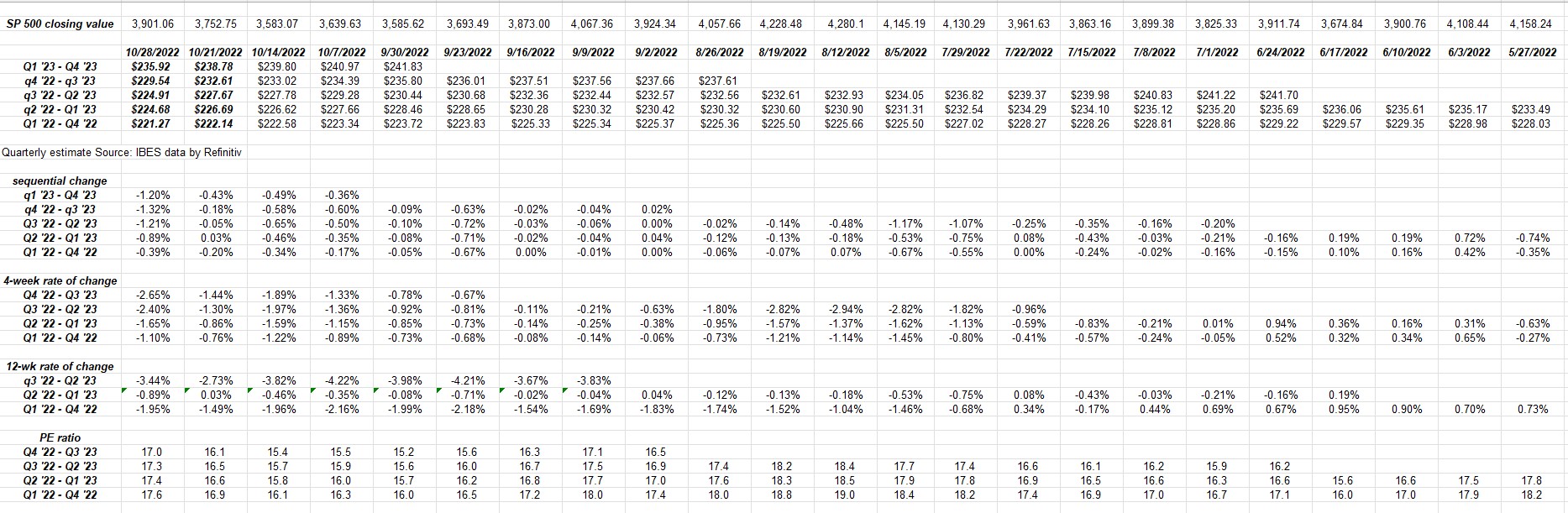

SP 500 data:

- The forward 4-quarter estimate (FFQE) fell to $229.54 from last week’s $232.61 or a sequential decline of -1.32% which is the largest sequential decline since early August ’22.

- After the nearly 4% SP 500 rally this week, the PE ratio rose to 17x versus 16.1x last week;

- The SP 500 earnings yield fell to 5.88% from 6.20% last week;

- Keeping an eye on the Q3 ’22 bottom-up estimate, it slipped to $54.78, below the $55 level which is where it should be, but with Apple’s and Exxon and Chevron’s report last week, the new bottom-up estimate should improve in the early part of Halloween week;

Rate-of-change:

This data around rate-of-change of forward estimates is not comforting. Let’s see if Apple, Chevron, and Exxon-Mobil change this trajectory next week.

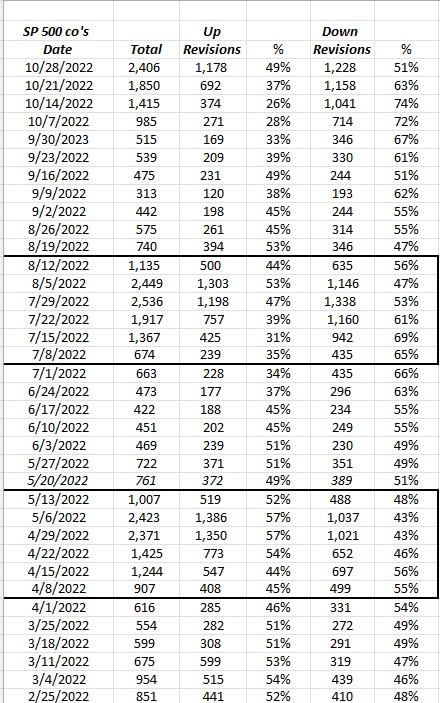

SP 500 Earnings Revision data:

The following data won’t be updated until Friday, November 4, 2022 but readers can see the trend in “positive revisions” in the last 3 quarters.

Again, there might actually be a “greater than 50% positive revision” print on 11/4/22 data, thanks to Apple, Exxon and Microsoft. (Here was a post published on September 17th, 2022 on this blog looking at the trend in revisions. We’ll find out this coming week if the trend has begun to reverse.)

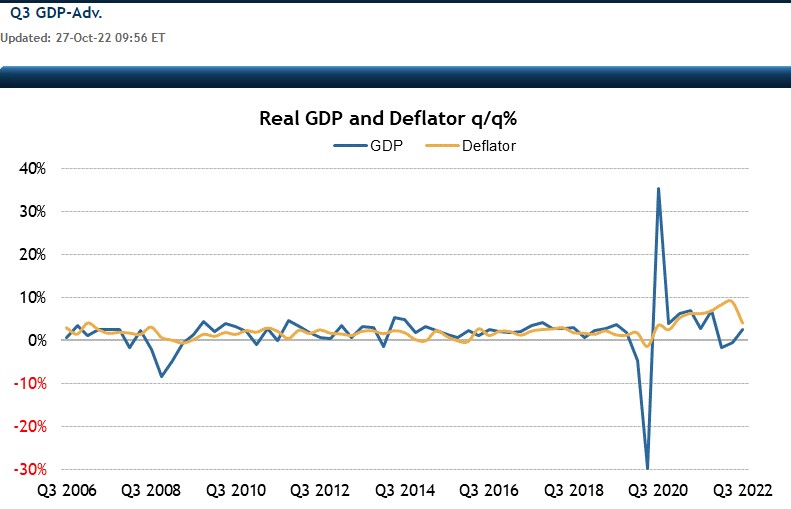

Summary / conclusion: While the Q3 ’22 GDP data looked good on the surface, reading Brian Wesbury’s commentary over at FirstTrust, once again exports were a big influence. In Q1 ’22, when the GDP was a lousy print, imports soared (which detracts from GDP growth) so Q3 ’22 is just a reversal of that effect and exports pushed the number stronger than it should have been. Wesbury added in his Thursday morning commentary that when he looks at “core GDP”, which Brian defines as “personal consumption + homebuilding + business investment” so actual Q3 ’22 GDP growth was just +0.1%, by the revised methodology.

For readers, the other aspect to economic data you have to keep in mind, is that when October ’22 payrolls are reported on November 4 ’22, or this coming Friday, the GDP data will be 5 weeks old.

All I really care about is inflation data and while the PCE data in Thursday’s GDP report wasn’t great, it wasn’t too bad either. According to Briefing.com data, the “advance chain deflator” which is reported with GDP came was expected at +5.3% and came in at +4.1%.

This chart from Briefing.com shows the deflator beginning to roll over (yellow line), but the market may want to see the Core CPI data first:

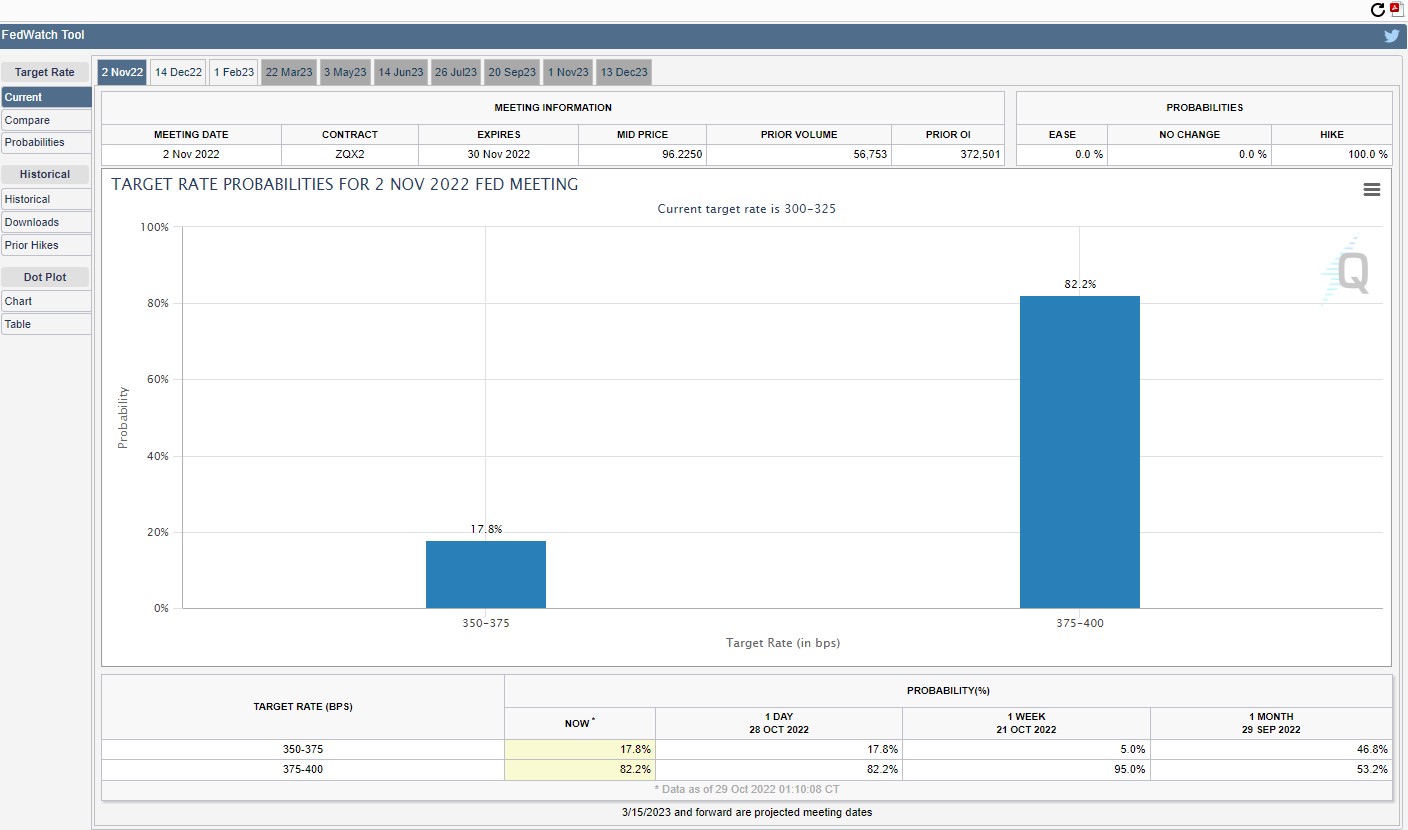

The Fed meeting Tuesday and Wednesday this coming week will almost certainly leave us with a new fed funds range of 3.75 to 4.00%. The current fed funds range of 3% to 3.25% has a midpoint of 3.125% thus after Wednesday’s release, expect fed funds to trade around 3.875%.

Blackrock (supposedly) put out a note this week to PM’s and clients saying to expect a softening in the Powell rhetoric around continued tightening. We’ll see – the Core CPI and overall CPI data isn’t scheduled for release until Thursday, November 10th, 2022.

There is a number of positives around the SP 500 and the various stock market indices in October: the November to April period is seasonally strong, at least technically anyway, the SP 500 really didn’t make a new low below the June ’22, 3,636 level for any period of time, high yield credit is holding up very well, in fact corporate high-yield (i.e. junk bonds) have also not made new lows below the June ’22 spoke lows, and the dollar is off it’s 22-year highs.

Some think Powell will lay waste to the market again on Wednesday afternoon, November 2, 2022, as he did in late August ’22 with his Jackson Hole speech, but I’m more interested in the market reaction to a “Fed Chair boot on the neck” of the market, than the speech itself.

There is an 82% chance the Fed raises the fed funds rate to 3.875% on Wednesday, November 2 ’22.

Technically, there are a number of reasons to be positive on forward equity prices. 2022 has felt so much like 1994, and Treasury Secretary’s Yellen’s comments about her worries over Treasury market liquidity were a bit of a wake-up call, similar to Greenspan’s comments in late 1998 over the relationship between Treasuries and the corporate credit market.

Fundamentally, I do not like how SP 500 earnings are rolling over. SP 500 CEO’s seem very cowed, with very few reluctant to make optimistic comments about 2023.

Scott Minerd the Guggenheim CIO was on CNBC in late September, and I thought he said the SP 500 has never bottomed before the Fed has stopped raising rates, but in 1994, the SP 500 bottomed in early December ’94, although Greenspan continued to raise rates into January, ’95. Back in ’94, 75 bp’s was a HUGE fed funds hike, while this year it’s commonplace. And it’s been more painful for the bond market in 2022 since the Fed was starting from zero fed funds, so as a percentage of the existing rate, these 2022 fed funds hikes are sizable. Back in 1993 and 1994, the Fed was moving off the 3% fed funds level up to 5.5%.

The SP 500’s expected forward returns still seem all about inflation and which way it way it heads. Watch the market reaction to Fed Chair Powell’s comments on Wednesday, November 2nd.

Take everything written today with a substantial grain of salt and healthy skepticism. These are opinions and only opinions and no recommendation to buy, sell or hold, anything. Past performance is no guarantee of future results and any opinions expressed here may or may not be updated in a timely fashion. Markets can change very quickly, both positively and negatively.

Thanks for reading.