Next week, Apple, Amazon, Meta and Alphabet report their June quarter earnings next week, and once again there is quite a bit of “high anxiety” and nervousness around the pending reports. Also, readers need to know that the FOMC statement is due out Wednesday, July 27th, and that at least 75 basis points is still planned for the fed funds rate hike, and then we get the first look at Q2 ’22 GDP on Thursday morning, July 28th.

To add another layer of complexity to the analysis, the action in the 10-year Treasury on Friday, July 22, is telling us a recession is getting closer and the infinite wisdom of the Fed is that they will be tightening the fed funds rate into a slowing economy.

That’s always fun.

The fact is I’m somewhat worried over the SP 500 earnings data trends by IBES data by Refinitiv. It’s been flat now for the first few weeks of the July ’22 earnings period, but only about 100 companies of the SP 500 have reported Q2 ’22 earnings. Historically, the typical pattern is to see positive EPS revisions by now.

Let’s look at all the data: (raw data courtesy of IBES data by Refinitiv):

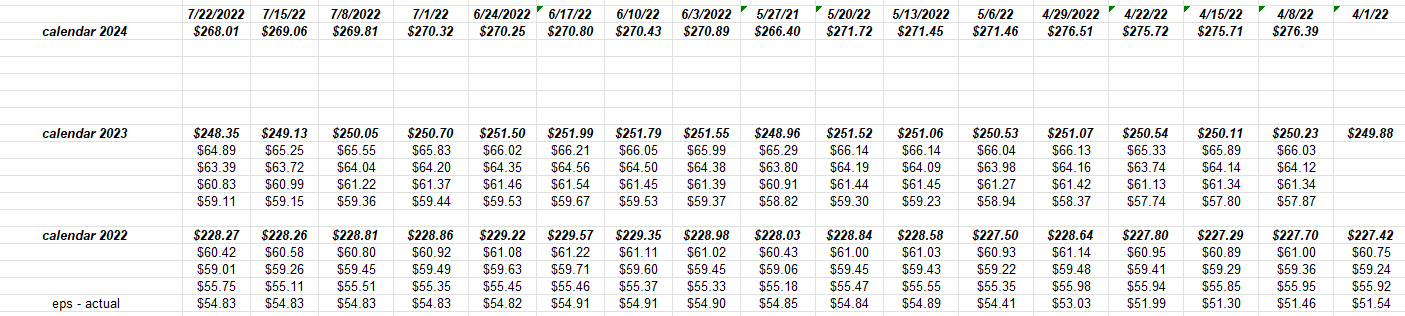

- The forward 4-quarter SP 500 EPS estimate was lower this week at $239.37, down from $239.98 last week, despite another full week of SP 500 earnings;

- The PE ratio rose to 16.5x from last week’s 16.1x;

- With the near-100 point rise in the SP 500 this week, (+2.55% on the week) the SP 500 earnings yield fell to 6.04% from last weeks 6.21% and is still down from the July 1, 6.31% print.

- The Q2 ’22 bottom-up quarterly estimate of $55.75 actually rose this week from last weeks $55.11;

The raw numbers week-by-week:

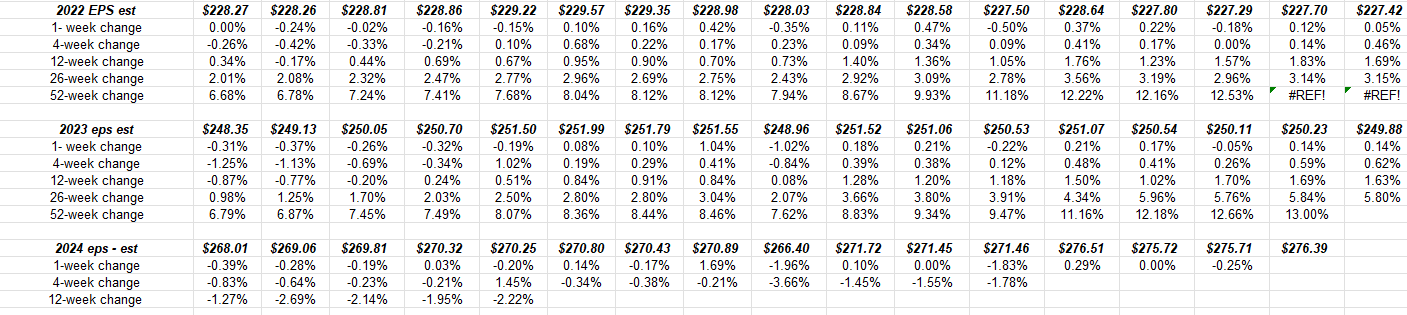

Rates-of-change:

It’s still a little early to worry about 2024, but with 2023 just 5 months away, 2023 SP 500 EPS estimate is down from a peak of $251.99 to $248.35 in the last 6 weeks.

There is no question that analysts are trimming numbers, but still modestly so far.

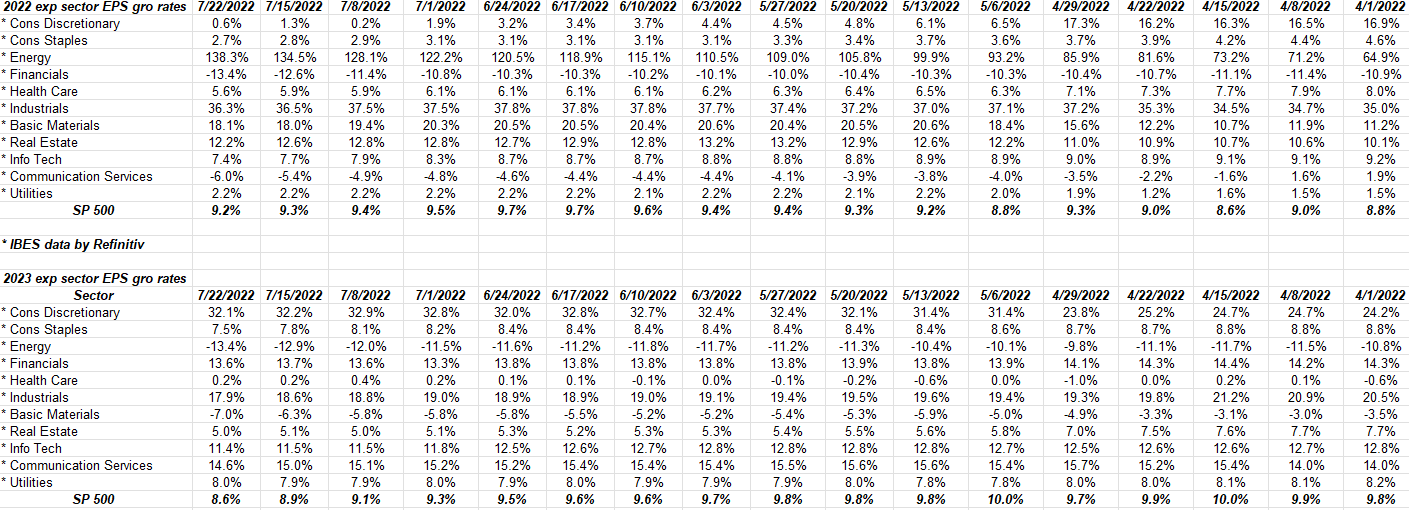

2022 and 2023 sector-by-sector EPS expected growth rates:

These tables are updates weekly from IBES data by Refinitiv.

Note how 2023’s SP 500 EPS expected growth rate is down 1% in the last 5 weeks. I’m more interested in the revision’s direction than the magnitude at this point. 1% over the last 5 weeks isn’t much BUT it should be trending up by now.

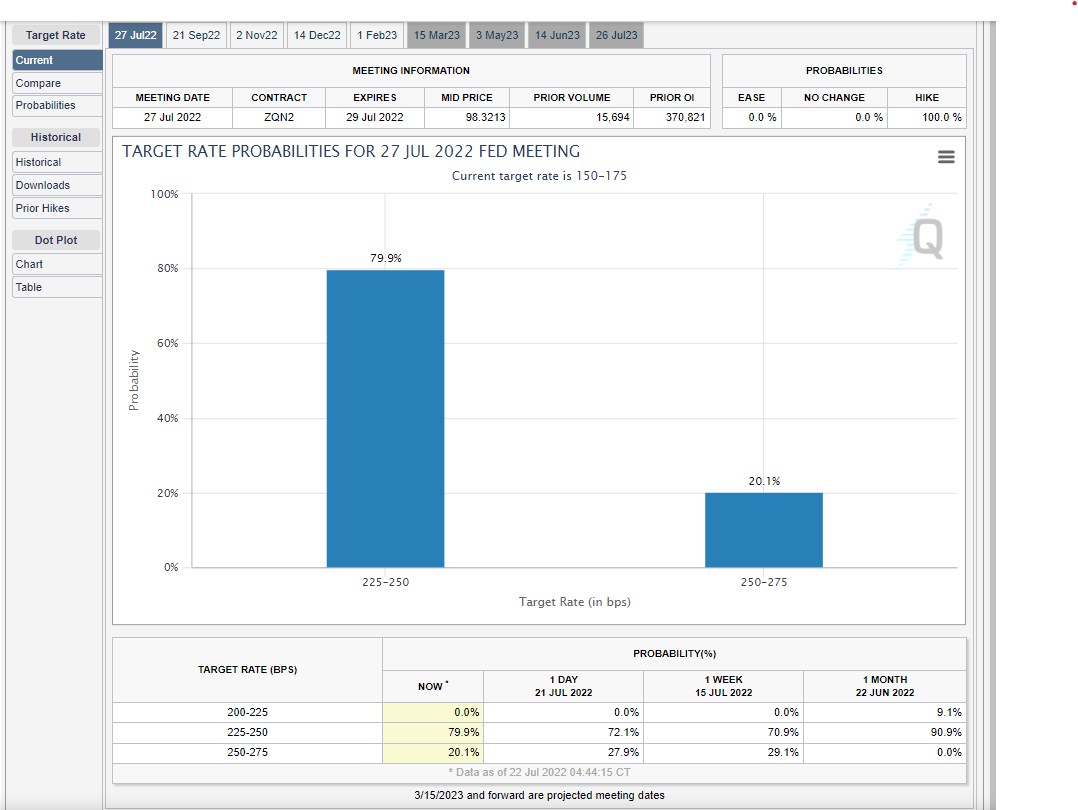

FOMC announcement: 7/27/22

This fed funds futures table from the CME website shows an 80% chance of 75 bp’s come Wednesday, and a 20% chance of a 100 bp move.

Don’t make it more complex than that.

The language and the Powell presser will tell us a lot more about the Fed’s and Powell’s body language around a potential recession.

Summary / conclusion: Coming into Q2 ’22 earnings season Bespoke noted that the level of bearishness around earnings expectations could be a positive, but sometimes the crowd does in fact get it right, so there’s a good reason to be nervous.

The 4 megacap companies reporting this week comprise 20% of the SP 500’s market cap as of July 22, ’22, and probably close to 13% – 14% of the benchmark’s earnings weight, so the coming reports this week are a big deal. I loved that Tesla put up a good report as a “high PE, high valuation” stock. The stock price just didn’t get rewarded as it has historically. With the Fed and inflation, it’s like running a marathon with a piano on your back for companies that are performing well, and hoping to see their stock price benefit.

This blog will have a look at the numbers for each tech company reporting next week, before the weekend is out.

Everybody’s nervous and the technicals for the benchmarks, like the SP 500 and the Nasdaq Composite, don’t look great.

Remember too, the comp’s for tech and financial sectors are very tough against Q2, 2021. That quarter saw some of the best y.y growth rates in years, last year, thanks to the earnings and revenue hits from Q2 ’20 and the pandemic. I’m going to attempt to give perspective on that, but blog posts aren’t supposed to be as long as “War & Peace”.

The rally in the 10-year Treasury and long-end of the yield curve along with credit spread improvement are quiet positives for the equity market. It always sounds more intelligent and intellectually appealing to talk about bad news, and what could go wrong.

More to come this weekend.

Thanks for reading.