The name of the bond market game since Covid-19 hit, if it can be summarized in one sentence, is that “credit spread assets continue to make sense”.

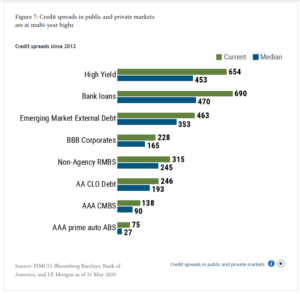

This graph from PIMCO was in their asset allocation outlook held for retail investors the last few weeks, and I think it did a good job highlighting the still-attractive credit spreads available in various asset classes, versus the longer-term median.

The spread data was as of May 31 per the graph, so I wish the data were a little more current for a July asset allocation outlook, but it is what it is.

(Clients are long the PIMCO high-yield bond fund in most balanced accounts.)

While some readers will think this is rather pedestrian in terms of credit market data, these funds are all owned by clients, and the following spreadsheet has been tracking “YTD returns” since the March ’20 lows for the various bond funds:

(Return data per Morningstar. Be sure and open the spreadsheet and expand it to see the weekly improvement in YTD returns of the major bond funds.)

The largest holding for clients has been the BlackRock “unconstrained” Strategic Income Opportunity Fund (BASIX) and that fund is now positive on the year.

The JP Morgan and Loomis Sayles Fund are evenly distributed amongst client accounts, and then comes PIMCO high-yield and within taxable accounts, John Miller’s Nuveen Municipal High-Yield.

Recently the BIV or Vanguard Investment-Grade Bond ETF (BIV) was added for a little duration, but it seems rather ridiculous to buy a 10-year Treasury bond today, even though the technicians like @GarySMorrow think the 10-year yield is headed lower.

Needless to say, clients are “tactically” overweight credit risk and credit spread through at least the end of the Q3 ’20 and I’ll probably wait to see what the Presidential election results look like on November 3, 2020, before reallocating again.

Clients are neutral to overweight corporate high-yield (a typical max weight is 12% – 15% of a bond allocation) but according to one high-yield manager the market is now “bifurcated” with troubled sectors like energy, retail and airlines, cruise lines, etc. trading over 10% current yields and then the high-quality end of the market trading near 5% – 6%. Clients high-yield exposure is primarily the PIMCO fund and the iShares HYG ETF.

The HYG topped out on June 5th at $85.03, (near-term high) and the SP 500’s short-term peak was on June 8th at 3,233.13.

A trade through 3,233 for the SP 500, likely means high-yield and the HYG will eventually follow.

Summary / conclusion: Liquidity is the “silent killer” in the corporate bond markets, but with the Fed’s 7 – 8 liquidity programs spread across corporate and municipal bond asset classes starting in early April, 2’0, the Fed and Jay Powell have stated they want to keep the corporate bond markets open for business so that corporations can continue to access the capital markets for refinancing, raising new funds, and rolling over debt.

Typically clients will see corporate high-yield credit bought under times of extreme stress like in early, 2009 and then again in the first quarter of 2016, when crude oil fell to $28 per barrel, and then sold within 6 – 9 months. Again, depending upon the Presidential election, the high yield weight will be evaluated during Q4 ’20.

In my own opinion, corporate credit risk is a higher-probability way to earn “alpha” in today’s market.

Take all these opinions with substantial skepticism. They are just one opinion, and I could very well be wrong too, but the Fed and Jay Powell have made it clear they want the corporate bond markets open and functioning.

Evaluate all these funds in light of your own financial profile and risk tolerance.

Thanks for reading.