Bespoke published a chart on Bespoke last week noting that this is the 4th drawdown in the stock in the “iPhone era”.

To highlight the last two longer pullbacks for readers:

- Sept, 2012: the stock peaked at $100.75 in September, 2012 and fell all the way to $55 – $56 by July, 2013. Total peak-to-trough correction was 44%. Apple’s fiscal year ends September every year, thus in fiscal ’13 EPS fell 10% while revenue rose 9%.

- April, 2015: Apple’s stock peaked at $133 – $134 in April, 2015, and subsequently traded down to $89 – $90 by May, 2016. Total peak-to-trough correction was 33%. In fiscal 2016, revenue fell 8% while EPS fell 9%.

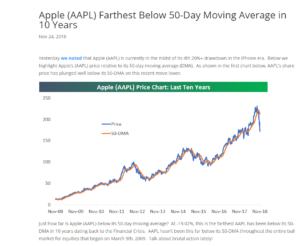

Sept ’18: According to Bespoke, Apple’s is currently in its steepest correction of the iPhone era, and in fact is now the furthest below its 50-day moving average at any point since the March, 2009, bull market. So far, since Apple’s peak at $230 – $231 in the first week of October, the stock is down 24% – 25% with Apple trading today at $174.

So what’s the point ?

Running trendlines on the chart off the 2009 and then 2013 lows, as well as noting the 200-month moving average at $140, my own thinking is ultimate support for the stock would be between $120 – $140, so I wouldn’t be surprised at a 43% – 44% correction.

That might seem shocking but Apple’s fiscal 2019 EPS estimate has already fallen from early November’s post-release print of $13.61 to $13.46. Apple’s revenue estimate has fallen from a consensus $281.6 bl for fiscal 2019 to $279.4 billion. Those declines are just in the last 27 days since Apple reported their fiscal 4th quarter on November 1 ’18.

Remember though, EPS growth was “negative” year-over-year for the last two substantial stock corrections in 2012 and 2015. Coming out of early November ’18 conference call, Street consensus was looking for 15% EPS growth for fiscal 2019.

Summary / conclusion: The only real question worth asking at this point is whether “Services” growth can offset hardware decline, but ultimately the two are tied at the hip I would think. The only reason for the blog post today was that I think Apple is in for a rough year and it has had these periodically over the last few years. However companies don’t stop disclosing key product information for trivial reasons. Starbucks stopped disclosing comp’s in 2007 and investors soon found out why. WalMart stopped disclosing comp’s and we found out why. Granted the Starbucks collapse or decline was exacerbated by the 2007 and 2008 bear market, but here is the key point for readers: companies don’t stop disclosing data that would make the company and its growth prospects look good.

Id look to repurchase Apple near $140, which could mean Apple has a 3% dividend yield or close to it. That is the point of the 200-week moving average. (For clients with big gains in taxable accounts, the stock was kept.)

$140 would be about a 40% correction, not unheard of in terms of its severity given the last two Apple corrections.

Take this all with a grain of salt, too. Apple may never get to $140 or even close to it. An accelerated share repurchase (ASR) might help if the December quarter is as bad as the estimates reflect. Also tariffs and what ultimately comes out of the trade talks matter too. This is somewhat of a back-of-the-envelope combination of fundamentals and technicals. It could be very wrong.

The stock is oversold on the daily chart and probably headed for a decent bounce.

And the stock may not be owned at $140 even if it gets there, and depending on what is happening around it. Apple has been THE stock to own off the 2003 bear market lows and then again off the March ’09 lows. One single stock typically does not lead consecutive bull markets.

Readers will be kept abreast of the trends in EPS and revenue estimate revisions – it has been a good tell for Apple.

Earlier articles on Apple are here, here and here.

The first article linked was the early tell for Apple, and Seeking Alpha didn’t even pick up the post. Sometimes cash-flow can give a false tell but as the third article linked shows, Apple has been fraying at the edges for a bit. It’s not necessarily horrendous, it just means cash-flow is declining versus net income. More of a “quality of earnings” issue.

Thanks for reading.