At 4% of the SP 500 market cap and 10% of the Nasdaq QQQ’s, not to mention the 20% EPS weight (per IBES by Refinitiv), Apple is not a small part of the US stock market.

The fact is, Apple is huge, and is now in the midst of a transition from a Technology hardware company to a Services business.

Apple was sold from many client accounts last Spring ’18, in the $160’s range. The stock is 25% higher since that sale, which took Apple from a top 10 position in client accounts down to near 30th in the position rankings, but with the news out of the conference call Thursday night about stopping disclosure of Apple’s product by unit, I remain comfortable with the decision.

The earnings preview of Apple posted to this blog last week showed upward revisions to numbers, but that changed with the comments after the conference call last Thursday.

Looking at the numbers this weekend, Apple’s fiscal 2019, 2020, and 2021 revenue numbers were revised higher, while the EPS estimates for the same years were kept the same or revised lower for fiscal 2019 and 2020. Fiscal 2021 did see a higher EPS number following earnings.

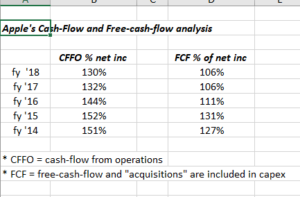

That means Apple could see ever-further margin pressure until the Services business grows substantially from 16% of revenue (as of 9/30/18).

Per a research note out of Jefferies, Apple will start disclosing their services gross margin with the December ’18 earnings release, which is expected to be quite higher than hardware gross margin.

Here is my biggest worry about Apple and this pressure could get worse:

Here is why investors are starting to see some of the quality of earnings diminish for Apple:

Here is a note from May 6th from this blog where a yellow flag was raised over this key ratio, but the stock is up another 15% since then.

Summary / conclusion: Like IBM in the 1960’s and 1970’s and then Microsoft and Intel in the 1980’s and 1990’s, the premier leadership stock for this bull market, and really the last 20 years, is starting to wear a bit at the edges.

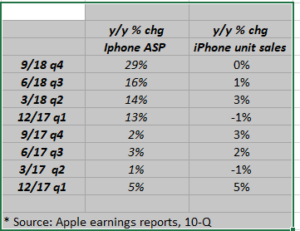

“Average selling price” (ASP) increases have driven almost the entire revenue increase for Apple as iPhone unit growth has flagged the last 4 – 8 quarters.

The iPhone is still 60% of Apple’s total revenue and 76% of total units as of the September ’18 quarter. (Refer to the second spreadsheet again.)

My biggest fear for Apple isn’t that it drops 50% in the next two years but rather it just treads water or remains range bound for years, just moving to-and-fro as the Tech giant transitions into Services.

And according to Morningstar, the Services business is not without it’s own risk. If read properly, Morningstar’s latest analysis of Apple’s quarter cites Amazon’s Alexa and that new genre of voice-enabled, home devices as a formidable threat to Apple. (Long Amazon.)

For me personally the Health Care business and Apple’s potential with the Apple Watch could be a HUGE opportunity for Apple if medical professionals, hospitals and such could figure out a way to safely trust and access the Apple Watch data that could monitor a user’s vitals. That’s an entirely new vertical for Apple with substantial margins and think about what it would mean for consumer health insurance bills.

The immediate future for Apple now is how fast the growth rate of emerging Services offsets the legacy of the Hardware business. Every major Tech company goes through this.

I’d love to repurchase Apple for clients but I’d like to watch how this whole Services transition evolves and occurs, but for clients, I’d prefer to watch from the sidelines.

Thanks for reading.