This summer, the CFA Society of Chicago, in one of their well-attended Vault Series presentations, featured Ted Reilly, the founder of Chicago Media Angels, the Chicago start-up that fills the gap between the artistic moviemaker and investment capital.

For some strange reason, the Chicago CFA Society asked me to interview Ted after the presentation for the podcast, which provided an opportunity to brush up on the sector and try to sound intelligent.

In fact within a day or two of the interview, Netflix (NFLX) had reported their Q2 ’18 earnings, and the stock showed its first crack as it traded down from $419 to $335 between mid and late July ’18.

The reason for the drop in the stock was that Q2 ’18 showed fewer subscriber additions than the Street consensus, which for a growth stock trading at 150x ’18 earnings per share, just proves it doesn’t take much for the air to come out of the tires quickly.

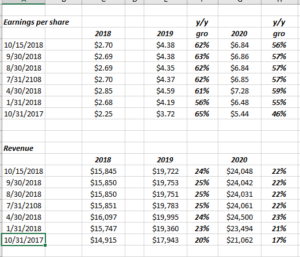

But here is a funny thing: the Street consensus estimates for EPS and revenue haven’t decayed much since:

Source: Reactive IBES consensus estimates as of 10/15/18

Readers can quickly see that after the July ’18 earnings report, the increases in EPS and revenue growth for Netflix quickly slowed and the upward revisions have stalled.

That being said, we have yet to see meaningful negative revisions. Consensus Street estimates still call for 60% EPS and mid-20% revenue growth for 2019.

Let’s see if that holds up after the 3rd quarter earnings report.

Fundamentally what is worrisome about Netflix outside of the nosebleed valuation ?

Well, the fact that Netflix hasn’t had a positive year of cash-flow since 2014, and even before 2015, cash-flow-from operations (CFFO) was just mildly positive. I’d list the numbers / metrics but the 2017 annual report lists the prior 3 years so take a minute to look at the cash-flow statement, and it is telling.

It’s clear that NFLX has ramped up the capex on primarily original or internal content, meaning they are creating and producing their own shows, rather than buying content from say, a firm like Chicago Media Angels, who wraps their business model around the ideas of a small movie-maker.

Summary / Conclusion: Netflix started the year near $200 per share, and by the July earnings report, had already doubled in price, so the recent consolidation was badly needed. The risk is that FANG / momentum and growth go out-of-favor and even if Netflix executes and subscriber growth emerges once again, the stock languishes because growth is out of style. The additional risk to the stock is that the Board is diluting shareholders by issuing common stock, and I can’t blame them given the price and valuation, but id rather not see the dilution than see it. (From June ’16 to June ’18, fully diluted shares outstanding rose from 438 to 451 million.)

A small amount of Netflix has been bought for appropriate clients, but the position is immaterial in terms of its weight.

It’s a better risk / reward to build positions in these higher P.E growth stocks when growth and momentum are out of favor, and growth and momentum investing have been on a 2-year tear since the last major correction for the SP 500 in Q1 ’16.

Disruptor companies like a Netflix may never get truly “cheap”. Now Reed Hastings will likely not implode like an Elon Musk, but streaming has attracted a lot of attention, and the competition is getting intense: AT&T’s Time Warner acquisition means HBO will be given a lot of cash and investment to compete with Netflix in that space.

- Q3 ’18 consensus: $0.68 in eps on $3.99 bl in revenue

- Q4 ’18 consensus: $0.51 in eps on $4.2 bl in revenue

- 2019 consensus: $4.38 on $19.72 billion in revenue

Let’s see how Q4 ’18 and 2019 Street consensus change with after the results and conference call Tuesday night.

Thanks for reading.