Jeff Gundlach, the “new” media-appointed Bond King in the last year, (and Jeff has made some good calls) who runs his own bond firm, DoubleLine Capital, was on CNBC yesterday (11/11/16) and weighed in on all things political, economic and fixed-income.

Jeff’s “sell everything” call of late July ’16 certainly looks good for his interest-rate prediction even though his asset-class is shrinking underneath him, and he could be very wrong on equity returns over the next few years.

The point being that yesterday – during the CNBC interview – it seemed like Jeff Gundlach covered all the scenario’s: he thought interest rates were going to rise, with a 10-year yield of 2.32% being a critical level, but he also thought that the adjustment to higher interest rates, and higher Treasury yields was almost over. Jeff Miller, the Econ PhD who founded NewArc Capital in Naperville, Illinois, and the great “Dash of Insight” blogger, has long noted that bond guys tend to be the more prone to “a conservative view of risk”.

Jeff Gundlach thought rates were headed higher, but the move almost completed, and then I saw the online Barron’s headline this weekend that says Gundlach says Treasury yields are headed to 6%.

Up, down or sideways, Gundlach will be right.

It’s interesting that not one bond guy I’ve ever listened to has ever said that – after a 35 year rally in Treasuries – that the US bond markets and interest rates could see a decade like the US stocks and the SP 500 did from 2000 through 2009, in other words a long period of negative returns.

Why I worry:

1.) Fund flow data – while some might find its predictive use questionable, but the roughly $104 billion poured into taxable bond funds this year (per ICI as of the end of July ’16) versus the outflows from equity funds is telling. To me, this is a contrarian indicator, and the money that has flowed into bond funds versus stock funds this year, likely won’t end well. When all that money that has come in to Treasury and investment-grade and structured finance bond funds in the last 24 months finally all wants to reverse, that should be interesting.

2.) The President-elect Trump “stimulus” plan (and really, both candidates discussed it) that quickly gained traction Wednesday morning, November 9th, would hit the economy when it has a 4.9% unemployment rate and a weekly jobless claims that are scraping the lows of the 1970’s. Personally I never thought stimulus plans like building the federal Interstate highway system did much unless the economy was really flat on its back. Just driving around the construction mess that is Chicago-proper today thanks to all the federal dollars that have found its way into the city, I wonder how much of a specific project is labor vs materials ? Politicians squawk about these projects as “job creators” (yes, one guy digs, five guys watch) but I would think you’d buy concrete / asphalt companies and the engineering firms like Chicago Bridge (CBI) or Fluor (FLR) and that very little of the project is labor, and much more is material. My point is the “stimulus” seems more psychological than real, but it could hit at the exact point a number of other pro-growth initiatives do as well.

3.) Corporate tax code overhaul and reductions in personal tax rates could be very stimulative to the economy since you would have to think a some of a corporate tax rate reduction could be used for additional hiring, and a decline in individual income tax rates should be stimulative to consumer spending. It might be one saving grace for bricks-and-mortar retailers.

4.) The FOMC has been “jonesin” to raise rates again, as inflation starts to tick-up into the 1.8% area. Basically, if you think about the Treasury yield curve, and you believe in “real rates” of return on Treasuries, the 10-year Treasury has been under water in terms of “real return” for the last few years, and even the 30-year is just barely positive.

5.) Inflation: partially addressed in #4, if you assume a real return on a Treasury note, or bond, should be at least 2%, and add the inflation premium on top of it, the 10-year Treasury yield should be trading at roughly 4% and the 30-year closer to 5%. Hard to believe that inflation and really “inflation expectations” decline moving into 2017.

6.) Municipal bonds have traded at attractive yields the last 4 – 5 years, a lot of times with muni yields at 100% of Treasuries, but if Congress and the White House cut ordinary income, and capital gains tax rates, particularly for high net worth investors, the relative demand for muni’s would decline. Lower tax rates equals less demand for tax-exempt income. That will send muni yields higher perhaps to attract additional demand. The point is muni’s might get hit harder than taxable debt in the next year.

7.) The TLT fell 7% this week, it’s largest weekly decline ever. Like equity returns in the 1990’s you would have to think individual investors aren’t prepared for the kind of losses they could see in their bond funds. IEF per Charlie Bilello, a technician whose work shows up frequently on Twitter said the IEF (7-year Treasury ETF) fell 3% last week, its 2nd largest weekly decline ever.

8.) Faster economic growth: in Q3, 2003, US GDP grew a whopping 8% and that was all pent-up demand post the tech bubble, 9/11, and the anxiety around the start of the Gulf War in March, ’03. You could make the case the US economy has been running only luke-warm for the last 8 years, post the Financial Crisis. If it gets revved up, it wont slow for a while.

Conclusion: A lessening of Dodd-Frank restrictions would turn the banks loose for the first time in 8 years, and get bank management’s more optimistic about generating revenue growth and generating ROE, at the same time we could see reasonable corporate tax reform and a lowering of individual income tax and capital gains tax rates, at a time where the economy is already generating a 4.9% unemployment rate, and the only relief valve would be the Treasury and corporate high grade bond markets, and you would think with a nervous FOMC if all this came together at once, the Treasury market would blow like a long-dormant volcano.

That $104 billion in taxable bond inflows in just 2016 would be under water for a LONG, LONG time.

2013 was a tough year for Treasuries as the yield on the 10-year Treasury rose from 2% to 3%. In the Spring of 1987 – March ’87 to be exact – I thought the 30-year Treasury fell 10 points in just one month alone.

Barclay’s AGG returns:

- 1-week: -1.37%

- 1-month: -1.58%

- 3-month: -2.20%

- YTD: +3.60%

Source: Morningstar, as of 11/11/16

The 10-year Treasury yield has already risen from 1.40% post-Brexit to 2.12% as of Friday, November 11, 2016.

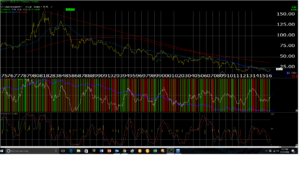

Here is a chart of the 10-year Treasury yield (CBOE contract TNX) going all the way back to pre-1980.

It does look like a bottom in yield has been forming the last 4 – 5 years.

For clients in balanced and bond accounts, mostly cash, some “strategic income” funds, and a 10% weighting in the TBF ETF (inverse Treasury ETF) have been the primary positions since the ’09 lows. At times clients have owned taxable high-yield, muni high yield, muni closed-end funds, and some other vehicles. To the detriment of performance, no investment-grade bond funds have been held for 2 years.

Here is a blog post from August 27th, ’16, when White Sox Park (previously called US Cellular Field or “The Cell” ) was renamed for a mortgage firm here in Chicago.

There is a potential for all the above stimulus to hit all at once, i.e. tax-reform, construction stimulus, faster economic growth, and it won’t be pretty in bond-land.

Thanks for reading.