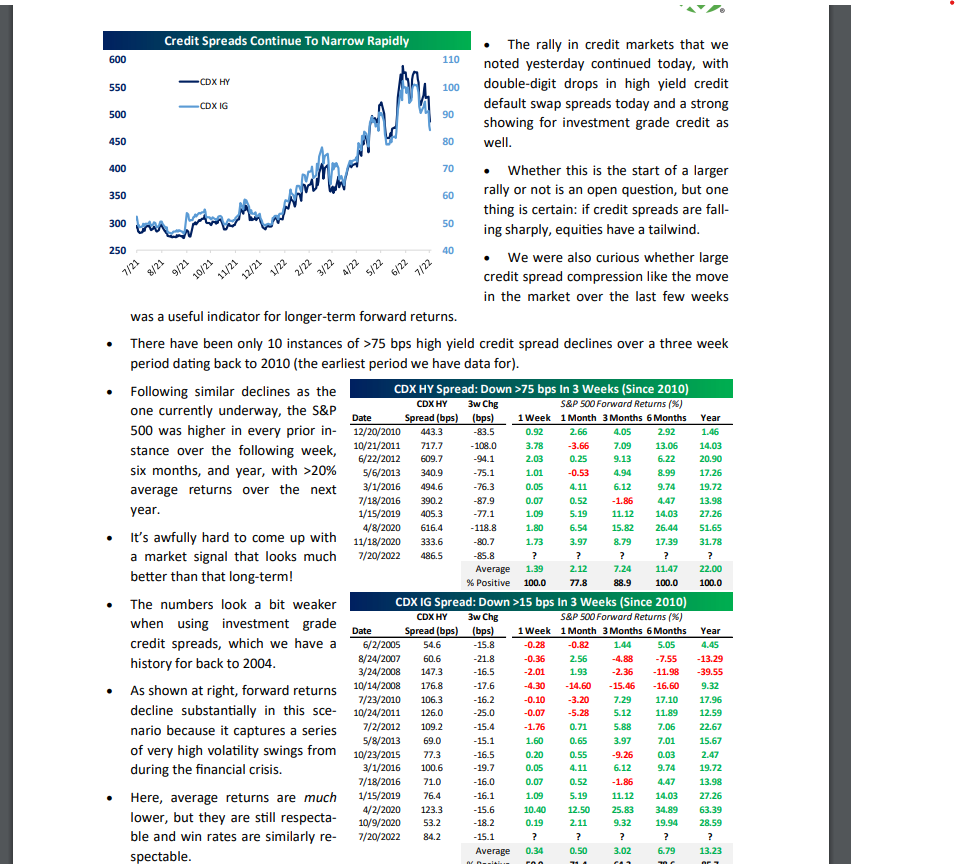

Bespoke, with their always-relevant research, put out (in my opinion) a very timely update on the improvement in high yield credit spreads today (Wednesday, July 20th, 2022) which have fallen 75 bp’s in the last 3 weeks.

The middle table above shows the SP 500 forward returns after such a rapid improvement in credit spreads.

As Bespoke concludes, and I’d agree, those are pretty impressive returns.

On another note, and thanks to great work by Refinitiv, during earnings season Refinitiv sends out an “Earnings Scorecard” each morning reflecting the previous day’s earnings, and from the “forward 4-quarter” estimate can be calculated.

Doing the quick math, here is how the “forward 4-quarter” estimate has changed since late last week:

- 7/15/22: $239.98

- 7/18/22: $239.93

- 7/19/22: $239.93

- 7/20/22: $239.88

This blog could have waited until Thursday morning’s update, but there may be another blog post coming Thursday night.

The point is after this week’s earnings reports, the “forward 4-quarter” estimate is lower by one thin dime since last Friday’s update.

Not seeing real downward pressure yet, next week is the big week, with mega-cap tech reporting their June quarters.

Summary / conclusion: Having lunch two weeks ago with a bond portfolio manager who has managed institutional bond money since the early 1990’s (and for whom I was an analyst for several years), he asked me when I’d get interested in high-yield credit again, and my response was I would need to see some possibility of the FOMC reducing interest rates. The PM then spent a few minutes explaining how high-yield was attractive right then and there and here’s why, and he turned out to be exactly right.

Most retail investors don’t understand the importance of credit spreads to the equity market in general and equity market valuations in particular, but we could be seeing a significant green light for further upside for stocks. Credit matters, as I discovered quite painfully in 2007 and 2008, when credit spreads continued to widen and I kept thinking (somewhat foolishly) “spreads will snap back”.

High-yield credit was down about 13% YTD as of June 30 ’22, according to index data.

After the lunch, clients saw an allocation to PIMCO’s High Yield Fund (PHDAX), which was down a little over 14% YTD as of June 30, and down 11% as of last night’s close.

This blog’s post from Monday, July 18th, 2022, on the market sentiment being as bad as 2008, plus improving credit spreads is a powerful combination.

Take all this with a healthy skepticism though. The FOMC is going to boost the fed funds rate another 75 bp’s next week at least, and possibly 100 bp’s but I would then expect Powell to acknowledge that much of the commodity price outlook has changed since June 17th, 2022, and – given jobless claims increasing – there looks to be some softening overall in the labor market. It would make sense for Jay Powell to acknowledge some of the changes on the inflation front after the Wednesday, July 27th announcement but that doesn’t mean it will happen.

Hope readers found this helpful.

Thanks for reading.