As was suggested in last weeks SP 500 earnings update, the bump in the forward estimate would come in between $230 – $233 and in fact it’s a little stronger than expected at $234.18.

To throw out some dry-as-dirt stats on the IBES data from Refinitiv:

- The final, actual, 2021 SP 500 EPS number was $208.11, an increase for calendar 2021 of 49% for the year;

- For Q4 ’21, actual SP 500 EPS grew 32% on a 15% y.y increase in Q4 ’21 revenue, versus Q3 ’21’s, 42.6% EPS growth on 17% revenue growth;

- With this week’s update, Refinitiv added a 2024 SP 500 EPS estimate of $276.39;

- Current SP 500 EPS estimates for 2022, 2023 and 2024 per the IBES data by Refinitiv are:

- 2022: $227.70

- 2023: $250.23

- 2024: $276.39

- The “average” expected, SP 500 EPS growth rate for 2022 – 2024 as the numbers stand today, is 10%, a return-to-normal growth pattern after the pandemic driven 2020 and 2021 results;

Here’s a rundown of the regular weekly data:

- The forward 4-quarter estimate jumped to $234.18 from last week’s $227.46 or a $6 jump, which is somewhat higher-than-expected, but still within a reasonable range;

- The PE on the forward estimate is 19.17;

- Interesting that the SP 500 “earnings yield” jumped to 5.22%, which is at the higher end of the last few years range;

JP Morgan (JPM) earnings preview ($392 bl mkt cap, ranked 12th in SP 500 by mkt cap wt): according to Briefing.com, JP Morgan reports before the opening bell on Wednesday, April 13th, 2022. Analyst consensus is expecting $2.69 in EPS on $30.97 billion in revenue for “expected” y.y growth of -40% and -4 respectively. While JP Morgan hasn’t seen negative y.y growth on EPS and revenue since Q1 ’20 or the start of the pandemic, the tough compare with Q1 ’21 is not helping either as JPM grew EPS and revenue 470% and 14% in last year’s first quarter, printing $4.20 in EPS on $32.2 billion in revenue. The $4.50 in EPS in Q1 ’21, may have been JPM’s highest quarterly EPS print ever. (My spreadsheet only goes back to 2008.)

For full-year 2022, JPM (or rather Street consensus) is expecting 2% revenue growth and a decline in EPS of -22% for the calendar year.

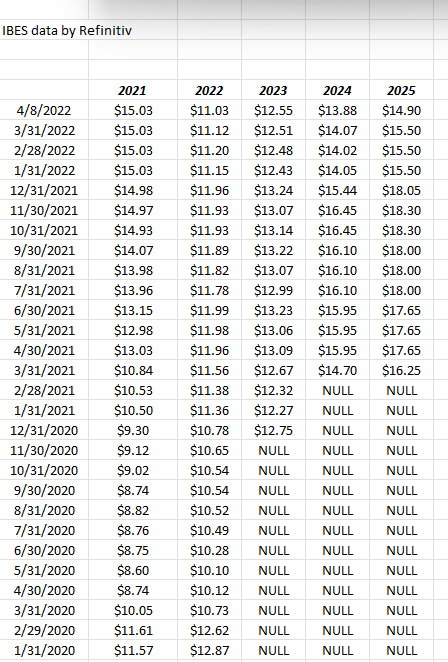

JPM EPS estimate revisions:

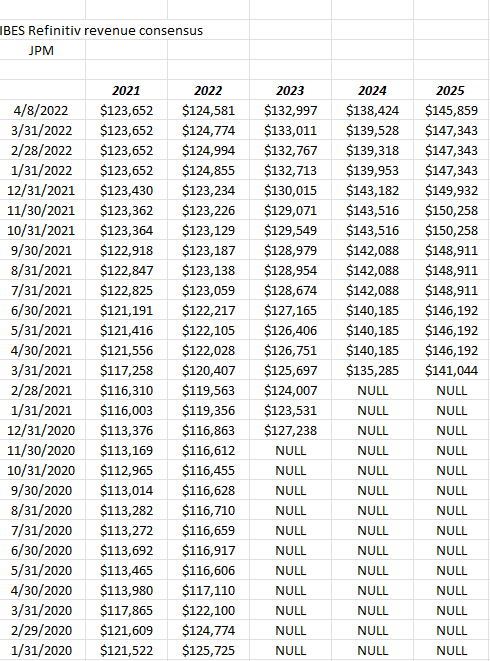

JPM revenue revisions:

The interesting aspect to the forward EPS revisions is that the Street consensus doesn’t expect JPM to exceed it’s 2021 actual EPS of $15.34 for another 4 – 5 years. That’s probably too conservative but it should tell readers that with 2022 likely being a tougher market, with fewer IPO’s, and less debt issuance, JPM’s capital markets group will likely lag 2021 results and with higher interest rates, housing and the consumer could slow later in the 2022.

As of Friday, 4/8/22, JPM is down 14.5% YTD, versus the SP 500’s -5.46%.

Jamie Dimon has talked about the $1 billion in Russian exposure for JPM and it will likely be an issue for Q1 ’22. Morningstar has a “fair value” rating on JPM of $152 per share, so the stock is currently trading at a 12% discount to that fair value estimate for the bank, which may not be enough to pull in newer investors that want a higher margin of safety for their stocks. Over the years I’ve become a bigger fan of Morningstar’s research and I do believe Morningstar’s fair value estimates also have their own “margin of safety” incorporated into the estimate.

JPM faces another tough set of comparisons in Q2 ’22 but over the next 90 days longer-term investors should get an opportunity to own JPM at a decent valuation. A positively sloped yield curve will help the banks and financial sector, but for JPM I think the slowdown in capital markets is a bigger issue and will return more to the type of capital market activity we saw in the middle of the 2010 to 2019 decade.

At $133 per share JPM is sporting a 2.9% – 3% dividend yield with low expectations built into 2022 EPS.

——————–

Goldman Sachs (GS) earnings preview: ($108 bl mkt cap )

Goldman is JPM on leverage and although the GS business is trying to penetrate the consumer and ultimately the commercial markets for lending, borrowing and serving the client, Goldman is still the premier investment banker on Wall Street their earnings and revenue volatility reflects that.

Goldman is expected to report Thursday, April 14th, 2022 before the opening bell with the Street (IBES and Briefing.com) expecting anywhere from $8.82 to $8.99 in EPS on expected revenue of $11.8 to $12 billion in revenue for “expected” y.y declines of 52% and -33% respectively.

Again Q1 and Q2 ’22 are expected to be horrid compares for the banking giant since GS earned $18 and $15 respectively in the first two quarters of 2021.

Full-year expectation for 2022 for GS are currently expecting an 18% decline in revenue and a 33% drop in EPS again which shouldn’t be surprising given the incredible surge in capital market activity from 2021 and 2021.

Looking at Goldman’s EPS history over the last 15 years, the bank giant earned between $10 and $20 in EPS for most of the decade from 2010 to 2019, but with the pandemic Goldman’s EPS surged to $60 (actually $59.36) per share in 2021. Just ball-parking and spit-balling for readers, if we split the difference, Goldman’s “normalized EPS” will probably fall somewhere between $35 and $40 per share, which means at $325, Goldman is probably pretty reasonably valued on PE basis (8x – 9x EPS) but readers have to factor the Fed and tightening monetary policy into consideration in 2022.

Summary / conclusion: If the 10-year Treasury continues to rise, the yield curve steepens and monetary conditions continue to tighten as the Fed is chatting about readers are likely better off with traditional old-fashioned banks and spread lenders and avoiding those financials with significant exposure to capital market activity but it really depends on how high the 10-year Treasury yield rises and what it does to IPO’s, bond refunding and issuance, mergers and acquisitions and the rest.

Goldman is cheap here but given that EPS and revenue volatility if it does slip under $300, readers likely need at least a 1-year time horizon to own the banking giant. JPM’s traditional corporate and consumer business will likely slow, but the delta (rate of change) is much lower than capital market activity thus JPM’s “normalized EPS” is likely much more stable than Goldman’s.

I do believe overall SP 500 earnings will be pretty healthy for Q1 ’22 and even Q2 ’22 but comparing versus last year will look horrid.

Readers might get a chance to own financials broadly at decent valuations at some point in Q2 ’22 with a longer horizon.

My own opinion is really all about the Fed, what happens with the 10-year Treasury yield and the yield curve shape and how ugly quantitative tightening will get.

These are all opinions on this blog and take all of it with substantial skepticism. Capital market conditions change rapidly.

Thanks for reading. More to come this week on financial sector EPS.