There is a little of everything this week for readers.

First, be careful about using SP 500 EPS information as a timing tool. Jeff Miller and I used to talk about this frequently, and this past week I happened to catch Josh Brown on The Halftime Show (one of his CNBC appearances) and he made a good point (I thought) about using SP 500 earnings as a timing tool. Jeff Miller and Ed Yardeni used to show their “recession” graphs and overlay SP 500 earnings on the graph, and while there is a “coincident” relationship between economic downturns and the SP 500 EPS results, I’ve wondered how much “forecasting ability” the forward SP 500 estimates capture.

In my opinion the “forward 4-quarter” SP 500 EPS estimate is still one of the best indicators the Street has, but it’s hardly perfect.

As has been written on this blog before, the Q4, 2018 SP 500 correction of 20% coincided almost perfectly with the weekly decline or “rate-of-change” in the forward 4-quarter SP 500 EPS estimate. That’s one of the few times though. Despite the magnitude of the 2008 correction, the forward 4-quarter SP 500 estimate didn’t peak until July, 2008, after the market had topped in October, 2007 right at it’s March, 2000 high.

The other complicating factor is that off the March, 2009 low, for the first half of the 2010 – 2019 decade, the SP 500 forward estimate would weaken for a few months, and then strengthen again to new highs as the quarter gets reported. Without getting too technical, there is a particular earnings pattern that seems to repeat itself in good markets, but it requires a longer explanation than today’s post allows.

SP 500 data: (all data sourced from IBES data by Refinitiv’s This Week in Earnings and Earnings Scorecard. All spreadsheets and tables are my own.)

- The forward 4-quarter estimate this week is $227.46 vs last weeks $227.28. The maddening aspect about this is that with roll into the April ’22 quarter, the forward estimate should be somewhere between $230 – $233, or the typical “bump” as we move into the new quarter, BUT IBES data wont publish the quarterly bottom-up estimates for 2023 until the first full week of April (and they do this every year) so the forward estimate – which is now Q2 ’22 to Q1 ’23 – is missing the Q1 ’23 quarterly estimate. Hence, I’ll estimate it for readers and say that by next Friday, April 8, the forward estimate will PROBABLY read between $230 – $233, maybe even a little higher.

- The PE ratio is 19.99x, but if the $233 forward estimate was used, it would be about 19.5x

- The SP 500 earnings yield is 5% even, just like last week;

- If the $233 forward estimate were used the earnings yield would be 5.15%;

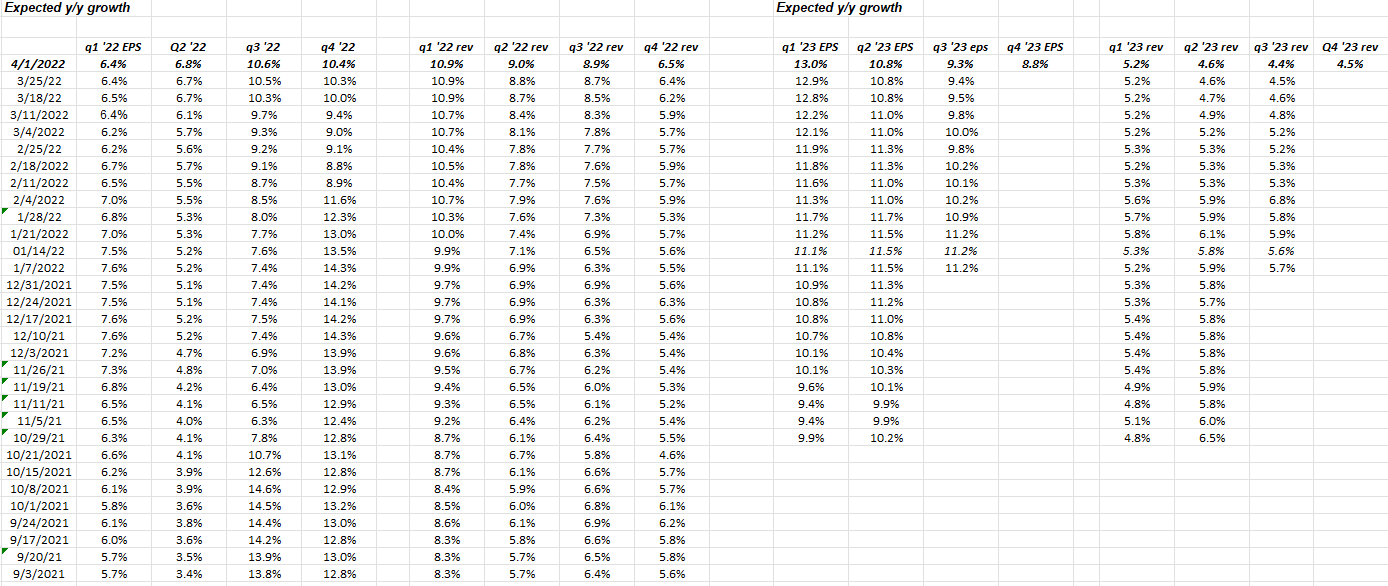

Expected SP 500 Quarterly Growth Rates for 2022 and 2023:

This is one of my favorite spreadsheets: note how 2022 expected revenue growth by quarter is seeing higher revisions since late in ’21, but EPS growth for the overall SP 500 is still not being taken higher. Analyst reluctance or red flag ? I’d be more worried if revenue were declining.

This is one of my favorite spreadsheets: note how 2022 expected revenue growth by quarter is seeing higher revisions since late in ’21, but EPS growth for the overall SP 500 is still not being taken higher. Analyst reluctance or red flag ? I’d be more worried if revenue were declining.

It’s one opinion but I do think Q1 ’22 earnings and revenue will be fine and we should see positive revisions to Q2 ’22.

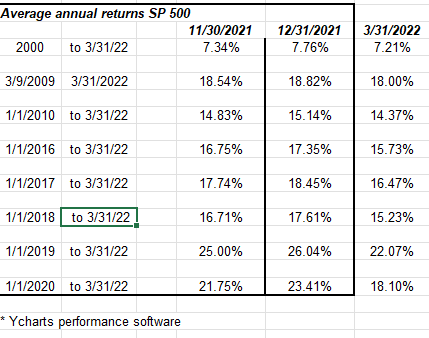

SP 500 average, annual return:

Just because it’s a small table, don’t underestimate it’s importance.

A flat year for the SP 500 would work wonders in terms of taking some of the froth from the 100% gain in the SP 500 from March, 2020, to March, 2022.

The summer of 2020 felt a little like 1999, early 2000, but then Tech peaked September 1, ’20, and there was a lot of damage done in the Russell 1000 growth names after March ’21. Gaming, online gambling, cannibis, SPAC’s, all had a tough time after late 2020. The indices actually held up fairly well in 2021.

SP 500 Top 10 Market Cap Weights (as of 3/31/22):

- Apple: 7% market cap weight, returned -.154% in Q1 ’22;

- Microsoft: 6% market cap weight, returned -8.19% in Q1 ’22;

- Amazon: 3.8% market cap weight, returned -2.23% in Q1 ’22;

- Tesla: 2.36% market cap weight, returned +1.97% in Q1 ’22;

- Alphabet: 4.5% market cap weight, returned -3.99% in Q1 ’22;

- Nvidia: 1.82% market cap weight, returned -7.21% in Q1 ’22;

- Berkshire (B): 1.7% market cap weight, returned +18% in Q1 ’22

- Facebook: 1.33% market cap weight, returned 33.89% in Q1 ’22;

- United Hlth: 1.25% market cap weight, returned +1.85% in Q1 ’22;

(Return data from Morningstar)

- The SP 500 returned -4.62% in Q1 ’22 and the QQQ’s returned -8.94% in Q1 ’22.

- Apple and Microsoft still comprise 13% of the SP 500’s total market cap as of 3/31/22.

- Only Tesla, Berkshire, and United Healthcare had a positive return in Q1 ’22.

Summary / conclusion: Tesla reported their Q1 ’22 deliveries either after the bell on Friday, April 1 or over the weekend, and the preliminary indication is that the 310, 000 deliveries were a “slight miss” from the 312,000 estimate although in this market, that may not matter. Tesla continues to deliver (so to speak) and the spike in gas prices the last 90 days had to help the fundamental story around owning the car, but supply chain issues still seem to be circulating around the edges of Tesla and the closing of one of their China plants thanks to a new Covid outbreak is supposedly a negative.

The only reason Tesla is mentioned is that it’s a major market cap weight (along with Amazon) in the consumer discretionary sector.

Housing and auto’s you’d think would have to start seeing some pullback from higher interest rates and higher gas prices. GM reported a y.y decline of 20% in auto sales mainly due to supply chain issues on Friday, April 1. GM finished the day down 1.75% to $42.96 but volume wasn’t even average.

SP 500 earnings start the week of April 11th, and – while there could be some earnings weakness (there always is), I still think the Fed, Jay Powell, and the prospects for 50 basis point tightening in May and quantitative tightening in May / June, will be a bigger market disruption than earnings. So far, the weekly earnings data and revisions look ok. Analysts typically update their models monthly so we’ve had two months of Ukraine, two months of much higher oil prices, 2 weeks of a higher fed funds rate and negative pre-announcements have been quiet. Some think starting tomorrow, April 4th, 2022, the negative news will start to rollout and we’ll hear SP 500 companies guiding lower on earnings, but even as retail bullish sentiment has risen sharply since early March, institutional investors are still quite tempered.

We’ll know more this week and next in terms of negative pre-announcements. We could see more negative pre-announcements than we have in the last 8 – 12 quarters, but watch how the stocks trade following the preannouncement.

I do think the 2nd quarter will be another rocky quarter, but not from SP 500 earnings issues, but likely from the monetary policy.

Take all this with substantial skepticism and a grain of salt. The worries for 2022 were the long outperformance of growth coming into the year, and “average, annual” return of the SP 500 as of 12/31/21. (See above table.) The SP 500 needs a year where it’s flat to +10% and the “megacap” outperformance subsides. This could all be wrong too, but the 100% gain in the SP 500 from late March ’20 to late March ’22 is too much, too fast.

Thanks for reading.