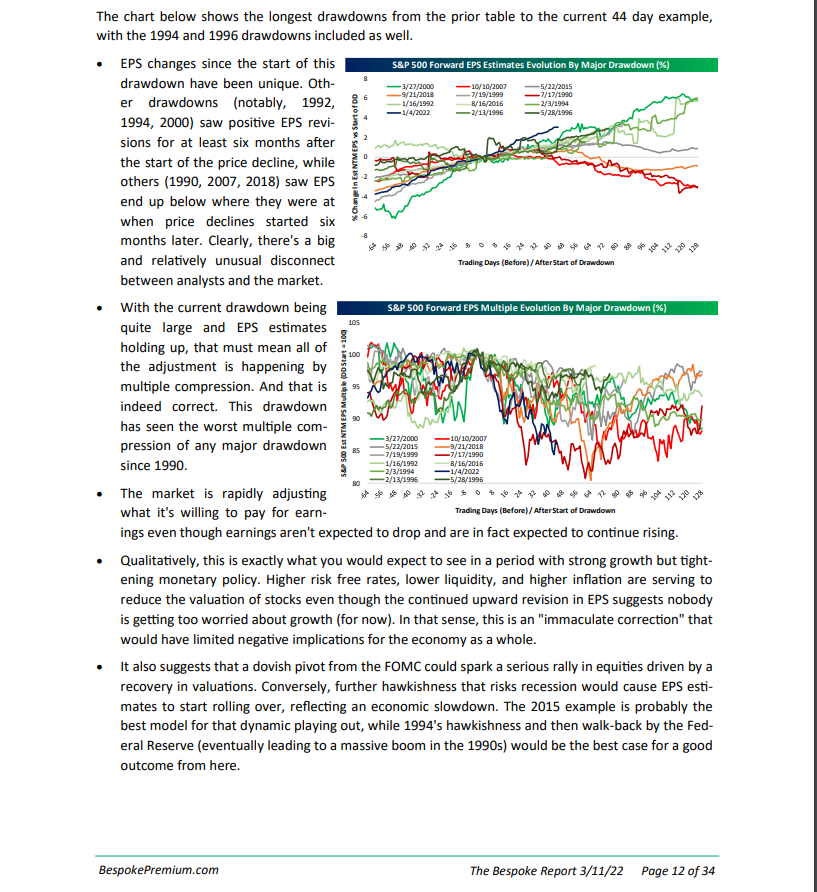

Long-time readers know that Bespoke’s research is one of my top picks for “value-added” work, and this weekend’s Bespoke Report was no exception.

From page 12 of this weekend’s Bespoke Report published Friday, March 11, 2022:

Read the 3rd sentence of the 2nd bullet point from page 12. ( Page 11 and 12 could be cut-and-pasted here but readers should reach out to Paul Hickey at paulhickey@bespokeinvest.com or justin@bespokeinvest.com to get the Report. Bespoke is very good research at a reasonable price. )

In fact the SP 500 earnings revisions this week were mostly positive and continue higher:

- The forward 4-quarter estimate rose to $226.46 from last weeks from last weeks $225.60 and 12/31/21 forward estimate of $216.14;

- The PE after the 2.44% decline in the SP 500 this week is 18.5x

- The SP 500 “earnings yield” jumped to 5.39% this week, expected given the benchmark drop, from 5.21% last week;

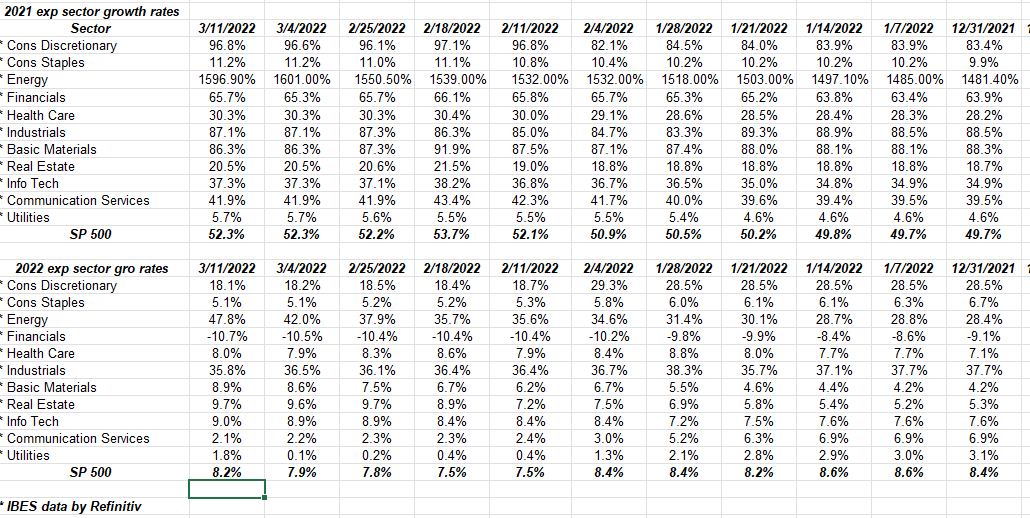

- Maybe even more interesting: check “expected” SP 500 EPS growth rates for 2022:

Consumer Discretionary (AMZN and TSLA) and Communication Services (FB) have seen sharp downward revisions while Energy, Basic Materials and Real Estate have seen steady positive revisions higher in their expected EPS growth rates for full-year 2022.

The point: despite the drop this in week in the SP 500, actual EPS revisions were positive and mostly higher.

Again, the caveat being that given how badly “consensus” missed with their post-pandemic earnings estimates, readers should be cautious about the same thing happening to the downside starting with Q1 ’22 earnings in about a month. (This blog listed the upside surprises or EPS beat rates for the SP 500 last week.)

Summary / conclusion: Whatever the market’s problems, they are not “earnings related” yet. All this means to readers with with a longer time horizon is that the market is giving you an opportunity to buy quality businesses at lower valuations.

That’s a good thing.

The question is how bad does the downside get on the SP 500 ?

Reading some technicians, a 1/3rd retrace of the SP 500 rally from the pandemic lows in late March ’20 to the early ’22 SP 500 highs, gets us to the 3,800 area for the SP 500 or roughly 10% lower from Friday’s close.

There are so many headwinds and cross-currents today: last week, Chinese stocks traded in the US got thoroughly whacked presumably on the SEC’s potential enforcement of the HFCAA (Holding Foreign Companies Accountable Act), and then US stocks that have a significant Chinese presence started to take gas when it became apparent that China could retaliate is the SEC (as is their right) started inspecting their financial audits for the last 3 years. (Here’s the CNN article on the action last week.)

The KWEB (KraneShares Chinese Internet ETF) fell 49.99% in calendar 2021 and is down another 38% YTD in 2022 as of Friday, March 11th.

Ukraine has set off a whole range of decision trees given China’s public support of Russia and Putin and what it all eventually means.

And then to top it all off, you have the Fed in the background, soon to be in the foreground this week with a 25 bp fed funds rate increase, and Wall Street figuring out what it all means, which probably translates to “reduce stock exposure”.

What’s happening in the US bond market deserves a separate post.

SP 500 EPS revisions and trends are still healthy: and as Bespoke noted, with this year being the “worst multiple compression” since 1990, something must give soon.

Take everything here with a grain of salt and substantial skepticism. Events can change quickly in the capital markets and become far worse than you suspect or become much better far faster than you’d expect.

Thanks for reading.