The SP 500 earnings lessons from the pandemic taught us that sell-side consensus for SP 500 earnings (actual vs estimates) grossly underestimated the actual results we saw during the earnings periods from June ’20 through December ’21. The “Upside Surprise” percentages for SP 500 EPS estimates were unusually large. Here’s the history by quarter both pre-pandemic and now post-pandemic from Refinitiv’s Earnings Scorecard report published every Friday:

- Q4 ’21: +5.2%

- Q3 ’21: +10.2%

- Q2 ’21: +15.7%

- Q1 ’21: +22.3%

- Q4 ’20: +15.7%

- Q3 ’20: 19.6%

- Q2 ’20: +22.9%

- Q1 ’20: +2.6%

- Q4 ’19: +4.6%

As readers can see, the upside surprise or earnings beat rate for the SP 500 soared during the post-pandemic liquidity boom, and is now in the process of returning to the long-run average of 2% to 5%. Jeff Miller and I used to talk about this frequently and I greatly miss those discussions.

The point for readers today is that SP 500 forward EPS estimates are still seeing “normal” upward revisions, but with Ukraine now exacerbating the post-pandemic distortions to the US economy, we won’t really know what Q1 ’21 SP 500 EPS and revenue estimates will look like until we see the actual results.

Still like reading the Weather Channel app before you step out the door every day, the SP 500 estimate data is still one of the best tools available to get a consensus on the forward numbers. Here’s a look at what we are tracking currently using IBES data by Refinitiv:

- The forward 4-quarter estimate fell slightly this past week to $225.60 from last week’s $225.70;

- The PE ratio on the forward estimate is 19x

- The SP 500 earnings yield is now 5.21% vs last week’s 5.15%;

- As the SP 500 PE compresses, as it is now, starting 2022 near 21x – 22x, the SP 500 earnings yield will rise, assuming no change in forward estimates as we are seeing today.

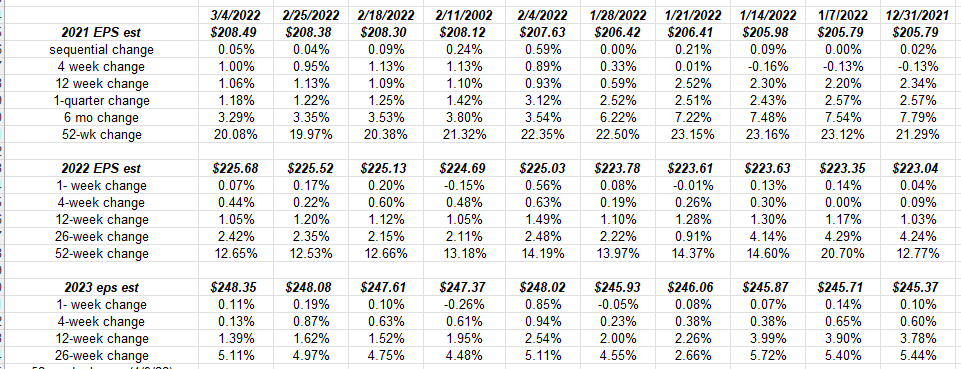

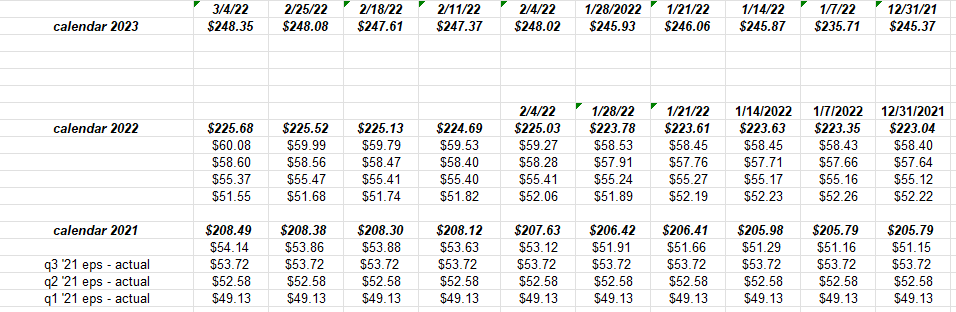

Here’s the latest SP 500 EPS annual estimates along with the respective “rate-of-change” for various time periods. There is gradual slowing of rates of change for SP 50 estimates, which was widely anticipated with the fed funds rate hikes and gradual withdrawal of excess liquidity from the US economy.

The above spreadsheet is a derivative of this weekly data:

While Refinitiv has yet to provide quarterly bottom-up SP 500 estimates for 2023, readers can see the progression in the quarterly SP 500 for 2021 through 2022.

I thought 2021’s Q3 and Q4 would show a print of better than $55 per share ( back in Sept – Oct ’21) but Q3 ’21 fell short, and with 3 – 4 weeks left in the quarter, Q4 ’21 will struggle to print $55 for the quarterly SP 500 “actual” print. It’s going to be close.

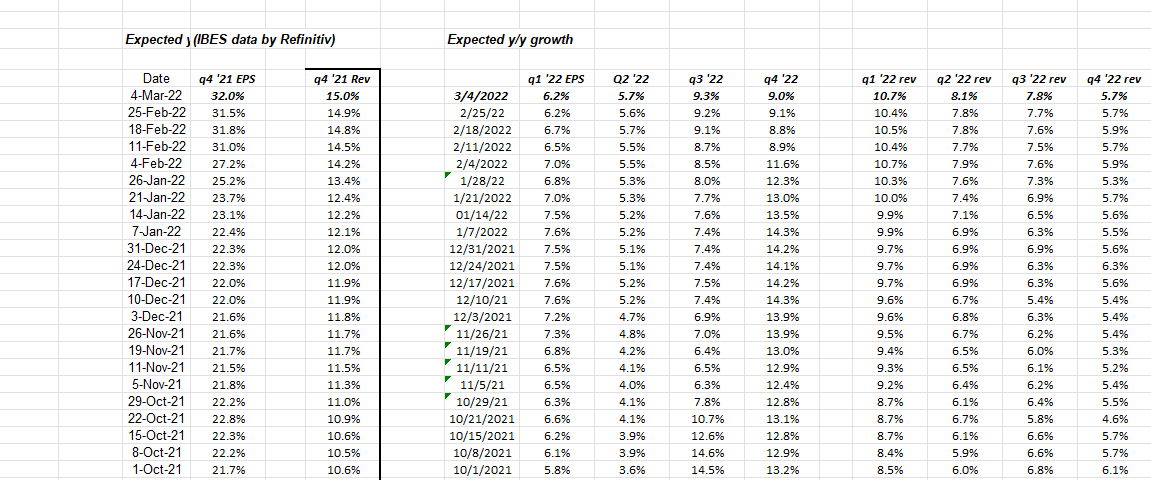

This is one of the favorite tables from our work with Refinitiv data. It shows the progression since Oct ’21 of the expected SP SP 500 EPS and revenue growth rates for the next 4 quarters.

Note how SP 500 revenue growth will peak near 10.7% in Q1 ’21 and will fall to 5.7% by Q4 ’21 in a rather linear fashion.

Take this data for what it is: a consensus estimate. As we learned during the pandemic, reality can turn out quite differently.

Summary / conclusion: While the title of today’s SP 500 earnings update is a “return to normal in 2022” actual results can differ greatly from estimates. Keep that in mind as readers do their “portfolio construction”. The other key metric from this week’s data is that the SP 500 earnings yield jumped to 5.21% and is still rising but not dramatically since the SP 500’s Top 10 positions are still holding up the SP 500.

Even though last week felt ugly and was a tough tape, the SP 500 fell only 1.25% on the week.

No question this is a very tough tape to trade.

Again, as a reminder, take all this data with skepticism. Thanks can change quickly for the capital markets. It’s surprising to me that commodities soared this week, while Treasuries rallied. It’s the “flight-to-safety” trade in Treasuries now dominating the inflation trade.

Ukraine has complicated everything in terms of portfolio construction and portfolio rebalancing.

Thanks for reading.