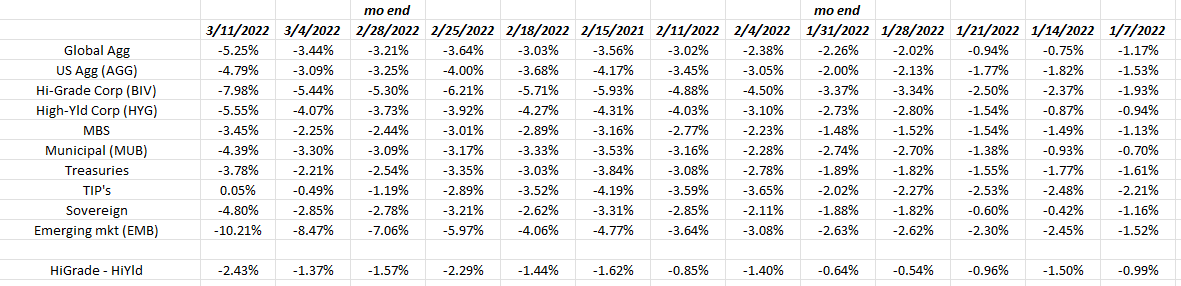

Bloomberg publishes YTD returns for the various bond market categories every day, and this blog tracks that data weekly. Only TIPS have a positive YTD return in 2022 as of March 11th, and just barely positive at that.

The Barclays Aggregate (AGG) is down about 5% YTD, which is the widely-recognized index for the US bond market although the 60% Treasury concentration in the AGG exerts a heavy influence on that return. I try and look at the AGG with the corporate high-grade bond market return and balance the two.

Corporate high-yield is outperforming the corporate high-grade index by 350 bp’s or so YTD, (-7.98% YTD vs, the -5.55% corporate high-yield YTD return) probably due to the duration of high-yield being half that of high-grade, i.e. 4 years versus 8 years.

Clients are long the SHYG as their corporate high-yield proxy, which has returned -3.63% YTD versus the HYG’s -6.31% YTD return.

It’s paid to have shortened the duration of your fixed-income and bond holdings coming into 2022.

(For disclosure purposes, client’s two largest fixed-income positions are the Blackrock Strategic Income Opportunity Fund and the JP Morgan Income Fund.)

Treasury yields:

One unusual aspect to the 2022 stock market selloff is that the “flight-to-safety” i.e. Treasury trade hasn’t happened.

Note the increase in the above yields across the Treasury yield curve since January 1, 2022.

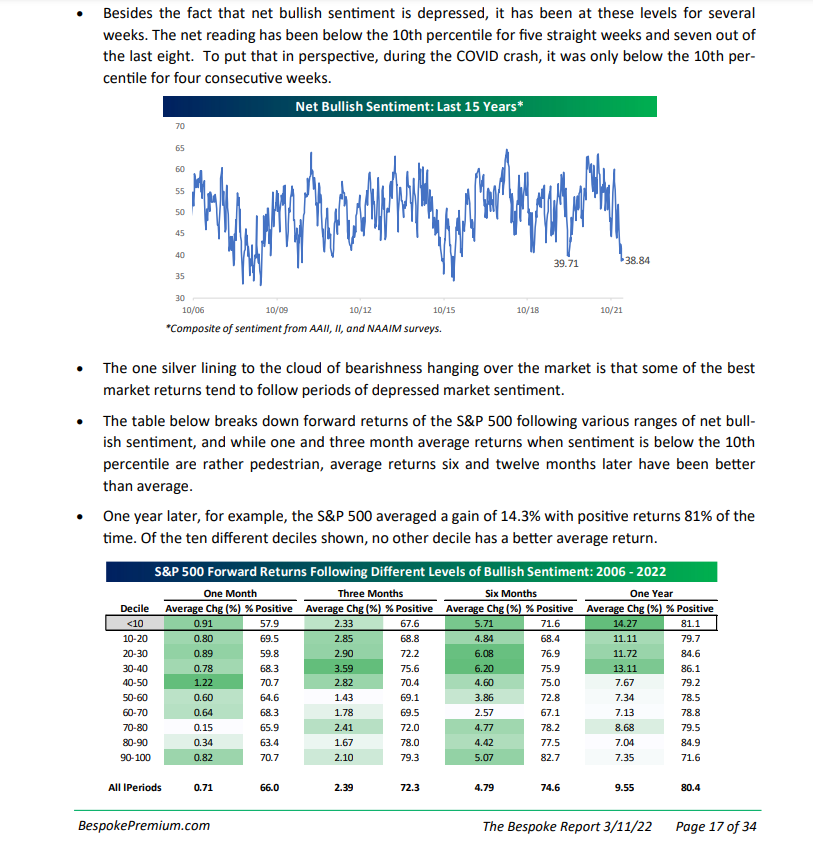

Stock market sentiment:

Source: Bespoke Investment Research (@bespokeinvest)

Bespoke felt so strongly about the above table that they published it again on Sunday, March 13th, 2022 after including it in the weekly Bespoke Report on Friday night, March 11th.

Bullish sentiment is very poor right now and the forward returns after periods of depressed sentiment are favorable, per the Bespoke table.

The only headline seen on Twitter that could possibly drive a formidable rally seen on Sunday morning was this one from FxMacro. What caught my attention is that they quoted a Ukrainian diplomat.

Watch US equity market futures Sunday night and take all this with substantial skepticism.

Summary / conclusion: Let’s say by some unexpected turn of events Russia does negotiate a peaceful settlement with Ukraine and ends up withdrawing from the country. With the end of Covid/Delta and now Omicron, think of how the US economy would likely respond if international events cease to be an issue. The last jobs report was all but ignored by the stock market as is decent SP 500 earnings data (see here) so investors would – at the very least – have to contend with an unfriendly Fed / FOMC and likely gradually-rising interest rates.

This is just one opinion, but even if Ukraine remains an issue for some time, a bigger deal for the US stock market in terms of igniting a rally would be a steady decline in the price of crude oil since right now, crude oil and gasoline prices are the face of inflation.

Again it’s just an opinion, but the psychological impact of crude oil and gasoline prices may be a bigger factor in the stock market sentiment data than Ukraine. (As a kid growing up in the 70’s, I vividly recall the OPEC oil crisis and what that did to gasoline prices. Back then gas was $0.30 a gallon and wound up rising to over $3 a gallon after OPEC repatriated all the crude oil reserves. It was nasty, and you had Watergate and the Vietnam War and – up until 1974 – Nixon’s “whip inflation now” domestic policies, which was nothing more than price controls and a total disaster.)

Again, if crude oil and gasoline roll over here, I do think it would help US stock market sentiment even if Ukraine lingers as an ongoing issue as it surely seems like it will.

Take all this as just on opinion and do your own thinking and homework.

Thanks for reading.